Archive for the ‘Seattle’ Category

Need a job?

I pulled up behind another car at a stop light yesterday and couldn’t help but notice a license plate surround for the local construction laborers union, plus a labor bumper sticker in the back window. This attracted my attention because the vehicle in question was a late-model Cadillac Escalade.

Admittedly this may have been an outlier, but all across the U.S. there is a huge demand for entry level construction trainees. Here in Seattle (a high-wage, high cost-of-living area) entry level “no experience, no education” wages are in the high-teens per hour, rising rapidly to $50k per year with a modicum of experience. Take some winter months to go get trained in plumbing, electrical, or HVAC and the annual income gets into the high 5 to low 6 figures pretty quickly. (The average plumber in Seattle makes $95,000 per year, according to Salarylist.com.) Some sources put this number somewhat lower, but you get the point.

Ironically, these jobs are going begging, and the reasons are varied. Many young people are scared off from a job that evidently requires a lot of outdoor work and physical stamina. Yet, as one young woman in a carpenter training program noted, “If you work hard and you put in your effort, they’ll take you over somebody else who is muscle…” Baby boomers seem to think that if their children don’t go to college, they’ve failed as parents, and so the percentage of construction workers under age 24 has declined in 48 states since the peak of the housing boom.

Wall Street Journal has a great article this morning called “Young people don’t want construction jobs. That’s a problem for the housing market.” It is indeed. It is one reason why home construction per household in America is at its lowest level in 60 years of keeping records, according to the article. The reasons include lack of vocational programs in high schools, although many of these are coming back. The Home Builders Institute, affiliated with the National Association of Homebuilders, has as many as 6,000 young people in their training pipeline at any given time.

I’m not suggesting — nor is the WSJ, that flooding young people into construction jobs will change the housing affordability metric overnight. The homebuilding industry is still replete with problems such as a trade war with our principle material suppliers, a lack of housing infrastructure, and short-term financing issues. Nonetheless, young people might want to be reminded that a surprisingly large number of CEOs in the construction field got started with a hammer in their hands.

Share this:

And yet more on housing

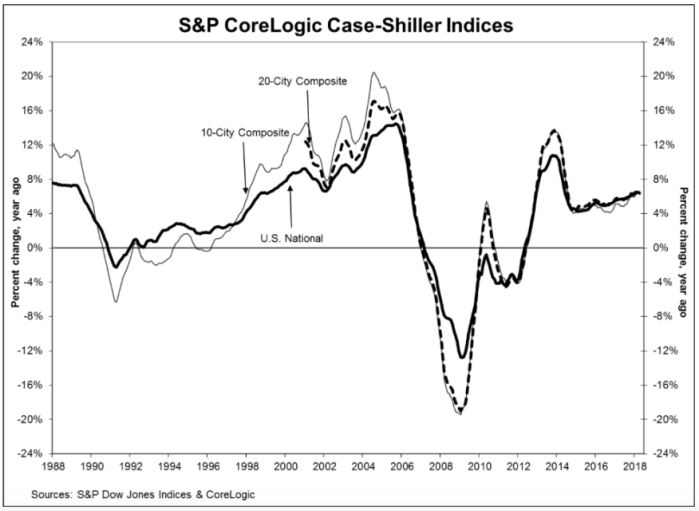

Twice burned, you know? I think we should all be a bit gun-shy about rapidly increasing house prices. Are we looking for a bubble or a peak?

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, reported a 6.4% annual gain in April, slightly down from an annualized rate of 6.5% in March. While they produce a few other indices, all of them basically report the same thing. Oh, by the way, my home city of Seattle leads the pack with an annualized rate north of 13%.

Glancing at the graphic, below, the slope of the current pricing graph looks suspiciously like what we saw during the bubble run-up. As I’ve noted here previously, house prices increasing at a rate higher than 2 points over inflation is emblematic of a bubble. That would suggest a nationwide rate somewhere around 4% – 5% right now. You do the math.

Share this:

WordPress v. Facebook

Loyal readers will note that I’m frequently on Facebook and less frequently here. You may have also noted (or not….) the very different tone of my two sets of writings. My pure FB posts are generally either my (fairly strident) political views or mental meanderings about family, travel, restaurants, and bars. In other words, normal stuff. My blog posts lean to business, finance, and the economy, with a bent toward real estate. By construct, the “voice” on this blog is different than the “voice” on FB.

Here’s where life gets interesting. I had the honor last week to speak to a small audience at a luncheon at Seattle’s historic Rainier Club about the economy. It’s quite impossible now-a-days to separate “economy” from “politics”, much as I might like to. Calvin Coolidge, I believe, said that the “business of America is business”, and the current government in D.C. has adopted that mantra. Sadly, the current government in D.C. appears to know quite little about mainstream business. they know a bit about a few things, and almost nothing about most things. That said, they’ve sold a bill-of-goods to many mainstream business folks. I saw a truck heading into Seattle today with InfoWars and “Arrest Hillary” bumper stickers. The driver was a bearded young man who appeared to be a hard working fellow. He’s been sold on the notion that the government in D.C. is on his side now, and they’re going to make everything a lot better. I’m waiting to see that. I haven’t seen anything yet out of D.C. that suggests this government is representing anyone other than Russian bankers and the Koch brothers.

At my Rainier Club talk, a questioner — clearly a Trump supporter — commented that the benefit of the new administration was that they were dismantling onerous regulations which affect small business. I reminded the questioner that I’m Chair of the Board of a business headquartered in Seattle, and that nearly all of our regulations are imposed by the City of Seattle and the State of Washington. I further reminded him that these regulations make Seattle the sort of place where creative people wanted to live, and since my bread and butter is hiring creative people, I’m happy to put up with these regulations in order to hire creative folks. I noted that Amazon, Starbucks, Nordstrom, Weyerhaeuser, Expeditors International, Expedia, Alaska Air, Microsoft, Boeing, Costco, the Russell Group, Symetra, F5 Networks, Paccar (who make Peterbilt and Kenworth trucks) and a host of other global companies were also willing to put up with these Washington State regulations in order to be able to tap into the brain trust that wants to live here. Intriguingly, the most “regulated” cities and states in the nation tend to be homes to the most forward-thinking and growing businesses. Indeed, New York and California have over 20% of the Fortune 500 headquarters, and the states which are generally the least regulated have no Fortune 500 or even Fortune 1000 companies (Montana, Maine, South Dakota, Wyoming, West Virginia, New Mexico, and Alaska). You go figure….

Share this:

12th Fed District issues 3q report

Greenfield is a global firm (albeit mostly in the U.S.), and even though we’re headquartered in Seattle, we try to focus our attention broadly rather than locally. That said, the 12th Federal Reserve District just released First Glance 12L (3Q15) which takes an early cut at the data from the nine western states. It’s very telling data — the “left coast” as I like to call it tends to suffer worse when times are bad and boom better when times are good. Thus, there are some interesting facts and figures to be gleaned from this well-written report.

Naturally, the report is focused on the health of the member banks in the region, but the macro-econ factors driving that health are of much broader importance. Nationally, unemployment stood at 5.1% at the end of the 3rd quarter. Western states tended to be a bit worse off, with 3 states (Idaho, Utah, and Hawaii) recording lower unemployment rates and the rest showing higher numbers, ranging from Washington’s 5.2% up to Nevada’s 6.7%. California, always the thousand pound gorilla in the room, came in at 5.9%.

However, job growth in the western states is well above the national average — 3% annually for the region versus 2% for the U.S. as a whole. However, the west is digging out of a deeper hole — while job growth nationally hit a trough of -4.9% at the peak of the recession, it bottomed out at -6.7% in the west. Generally, job growth in the west over the past 20 years had held steady at about one percentage point above the national trend during “boom” years.

Housing starts in the west are well below the pre-recession peaks. As of September, 2015, the seasonally adjusted annual rate (SAAR) of housing starts stood at 161,000, with 107,000 of that in 2+ family units. This compares with a peak of 449,000 SAAR in the 2005-2006 period, at a time when 2+ unit housing only made up 85,000 of the starts. Arguably, the market in the west is still absorbing the huge shadow inventory built up during the boom days.

Commercial vacancy rates in the west have been drifting down for the past few years in the office, industrial, and retail sectors. Apartments, however, seem to have plateaued around 4.3% at the end of the 3rd quarter, and are forecast to rise a bit to 4.7% a year from now. I might posit that historically, profit-maximizing apartment vacancy rates have been found to be somewhat higher than these numbers, so apartment managers and owners may have some lee-way to continue building.

The 5 western maritime states are very export-driven, and the strength of the U.S. dollar (up about 18% against major currencies since 2014) has been rough news for those markets. While western state exports rebounded nicely from the trough of the recession (up about 17% from 2009 to 2010), export growth has flat-lined since 2012. Regionally, exports declined about 2.5% since last year, with positive growth reported in only four states (Arizona, Hawaii, Nevada, and Utah). Bellweather California saw exports decline 3.6%. Note that in Washington, my semi-home state, exports make up 21.2% of the gross state product. (We export things like big trucks, big airplanes, software, and agricultural products.) Hence, this is critically important stuff.

The remainder of the report focuses on the health of the regions banks. I’ll leave that up to the reader if you care to download your own copy. Short answer, though, is that the region has seen loan growth accelerate even while the nation as a whole has flattened. Further, the regions banks tend to be a bit more efficient in terms of expenses and staff, both compared to the nation as a whole and compared to the “boom days” pre-recession. Both small and large commercial borrowers generally reported tightening credit standards at the end of the 3rd quarter, which is a change from previous reports. However, consumer borrowers (residential mortgage, credit cards, and auto loans) generally reported easier standards. The bulk of loan growth for small banks (under $10B) came from non-farm non-residential, while for large banks the biggest growth sector was in consumer lending. The percentage non-performing assets (the “Texas Ratio”) in the region, which peaked at 38.9% in 2009, is now down to 5.4%, although still higher than in the 2004-2007 period. By comparison, the national peak hit in 2010 at 19%, and is now standing at 7%, also higher than pre-recession levels.

Share this:

The Center for Wooden Boats

My attentiveness to this little blog of mine has waned the past few months. I’ve been terrifically busy, which is of course a “good thing” as Martha Stewart says.

That having been said, despite my “busy-ness”, I recently accepted a seat on the Board of Trustees of the Center for Wooden Boats. The CWB has been at the southern tip of Seattle’s Lake Union for many years, serving as an educational resource about our maritime heritage. Those of you familiar with the current re-development of that portion of Seattle will instantly recognize that the CWB is wonderfully located. Our next-door-neighbor is the old Naval Reserve facility, which has been converted to house the Museum of History and Industry. Together, these two fantastic resources now anchor a huge park/public space in the hottest part of town. To match the demand, CWB is now in the final stages of a multi-million-dollar capital campaign to fund a new education and meeting center.

CWB really has the potential to be a resource of national and even international recognition and quality. While many museums and galleries around the world are facing tough times, CWB continues to enjoy tremendous support. Naturally, the upsurge in attendance and attention have strained these resources, and part of my task as a new board member — coming from a finance/business perspective — will be to aid in the stewardship of this valuable center.

More later, but if any of you have any interest in how to engage or support the CWB, please let me know.

Share this:

A few thoughts about the stock market

As the Dow Jones Industrial Average creeps ever so slowly toward 13,000, I’m reminded of the words of William Shakespeare, from the famed “Seven Ages of Man” soliloquy in the comedy, As You Like It:

…and then the whining school-boy, with his satchel and shining morning face, creeping like snail, unwillingly to school…

Now of course this blog is primarily focused on real estate and the various economic forces that affect it. However, since so much of real estate is securitized, particularly in the U.S., and so many of the players in the real estate market are publicly traded companies, an occasional glance at the ticker-tape is in order.

With that in mind, I have a small idea. It’s not a huge one, but just a little observation, if you will, about why the market is creeping so slowly, even though so many pundits claim that it’s underpriced right now. (I neither agree nor disagree with that sentiment — I’m in a wait and see mode.)

However….. I serve on the board of a small Trust which is VERY conservative. Our sole manager also manages a lot of high-tech money (remember — Microsoft is headquartered here… duh…). We have a lot of liquidity, and even our bond investments have a very short average duration.

As one money manager put it to me, “Our clients aren’t interested in MAKING money in the stock market. They just don’t want to LOSE any more money in the stock market.”

Thus, there MAY BE some upside potential to this market. However, it may take a long time to realize it, because so many money managers got singed in the flames of the market burn-out a few years ago.

Share this:

Conerly’s Businomics Newsletter

I’ve mentioned before that one of my favorite economic writers, particularly for the Pacific Northwest, is Dr. Bill Conerly out of Lake Oswego, Oregon. Even though Greenfield’s practice is national, we have to maintain a bit of a Northwest focus to our work. Dr. Conerly helps us with the underlying economics driving the economy of this salmon habitat in which I live.

Dr. Conerly’s “charts” are wonderfully informal and informative at the same time. In the ‘old days’ he would simply hand-write his thoughts on the charts then fax them to his subscribers (remember “faxing”?). Today, of course, it’s all digitized and stored on his web site, with an emailed link. Nonetheless, the succinct hand-written notes are still there, and the brevity is welcomed. (I could learn from that.)

Rather than reproduce the charts here, I’ll simply give you a link (here) and you can go view them yourself. If you’d like to contact Dr. Conerly — he’s a great speaker and consultant on economic issues — then the e-mail address is bill@conerlyconsulting.com. A quick synopsis may whet your appetite:

- Business equipment orders are still not back to the pre-2008 peak.

- Consumer sentiment is up, but not back to 2007 levels

- A January, 2012, Wall Street Journal survey pegged the risk of recession at 19%

- Private non-residential construction has “turned the corner”, but is still significantly lower than 2007-2009 levels.

- Unemployment: great headlines, but we’re a very long way from feeling good.

- Mortgage rates are at all-time lows, but only if you have great credit.

- Stock market: lots of up-side if Europe manages to muddle through

- Oregon and Washington bankruptcy filings on the way down, but still over double the 2007 rates

- Boeing orders may be tapering off, but still significantly exceed deliveries — no need to cut output

- Wheat prices (an important economic component in our area) are downturning, due to the global slowdown.

Well, folks, that’s about it — great reading from a great analyst.

Share this:

Global and Local Data

Two important economic research pieces hit our desks this week — the RICS Global Commercial Property Survey, and the Dr. Bill Conerly’s Businomics Newsletter. The former, as its name implies, has a very global reach (the U.S. included), and gives a great basis for comparison of how the U.S. commercial real estate economy is doing relative to other economies. Naturally, this begs the question, “Are there OTHER economies?” From an investment perspective, all “economies” are integrated, and while each occupies a different place on the risk/reward graph, they are all viewed through the same lens by the equity and debt markets. Dr. Conerly’s work focuses narrowly on the Pacific Northwest, and gives us a great snapshot on how our local economy is doing. It’s a “must-do” resource piece for any work we do in our backyard.

RICS, of course, stands for Royal Institution of Chartered Surveyors. First charted by Queen Victoria in 1881, it is now the world’s oldest and largest property-focused organization, with 100,000 professional members and 50,000 students in 140 countries. Greenfield has been pleased to be affiliated with RICS here in the U.S. for quite a few years.

The headlines speak for themselves:

from RICS Global Commericial Real Estate Survey 1Q2011

For your own copy of the report, or one of the regional reports, visit the RICS web site by clicking <here>

Dr. Bill Conerly, based out of the Portland, Oregon, area, is a great friend of ours here at Greenfield and one of the region’s top consulting economists. His newsletter presents key national economic trends (along with his pithy comments) and then focuses on how these play out in the Pacific Northwest. He calls national GDP growth since the start of the recovery “disappointing”, and notes that while consumers seem to be rebounding and business equipment capital spending is growing moderately, construction spending is still “weak”. Housing starts are still troubling (for more on this, see some of my prior blogs on the housing market) and despite gas prices, inflation still seems to be under control (actually near the lowest levels in the past 5 years.) The spread of junk-bond yields over treasuries hit a peak of nearly 2000 basis points in 1009, and is back down to between 500 and 1000, but still above the roughly 300 basis point level of 2007. Dr. Conerly suggests there is still some worry about risk, although I would posit that 700 or so basis points is probably a healthy level. Finally, on a national view, Dr. Conerly is looking for “decent but not dramatic gains” in the stock market.

On the local front, Dr. Conerly notes that both Oregon and Washington bankruptcy filings have turned downward from their peak levels last year, although both are still well above levels pre-2009. Through the recession, both states have seen substantial net in-migration (Oregon at about half of Washington’s level), although Oregon’s in-migration had trended slightly downward and Washington’s slightly upward.

For more information on Dr. Bill Conerly or copies of his charts, visit him here.

Share this:

Greenfield Named a “Best Place to Work”

A little bragging opportunity — and we’ll be sending out reams of press releases on this — but I thought I’d give you guys an early peek. Seattle Metropolitan magazine just released it’s list of the 20 best places to work in the Seattle market. You’ll recognize some of the names on the list — Zillow.com and Expedia.com. We’re terrifically pleased that Greenfield is #9 on the list of best places to work in Seattle.

Seattle is a great place to run a business — extremely bright people are attracted to live here, and as a result, a firm like Greenfield can pick and choose the brightest minds who want to get into real estate analysis. While we have two great university-based real estate programs in the state, we’re able to attract new hires from the top programs all over the world — indeed, one of our most recent hires had just finished his masters degree in real estate in the U.K.

Conversely, to keep and maintain such a creative staff, we have to offer an exciting and intellectually invigorating place to work. When we’re in a fairly small city, and competing against some of the most creative and exciting firms in the world (e.g. — Microsoft, Costco, Starbucks, the Russell Group, Weyerhaeuser, Amazon, Expedia, Boeing, Paccar, Nordstrom, etc.), we have to constantly strive to be the best.

Thanks for the chance to brag a bit. This is a REALLY big deal, and I’ll be bragging more and more about this in the coming weeks.

Share this:

Mueller’s Market Cycle Monitor

Dr. Glenn Mueller’s Market Cycle Monitor just hit my desk from the folks at Dividend Capital. To access it, or some of their other great stuff, just click here.

I’ve written about Dr. Mueller’s work before — while his model isn’t able to forecast really major moves (like the “fall off the wagon” move of 2008/2009), his Market Cycle synopsis does a great job of assessing how various property types and submarkets are moving through the normal stabilized cycle of business. In short (and I’m sure he’d do a better job of explaining this than I could), at any given point in time, a market or submarket is in one of four investment states: Recovery, Expansion, Hypersupply, and Recession. The way market participants react to one situation drives the market forward to the next situation. For example, in the recovery phase, no new properties are coming on-line. Natural expansion of the market drives up occupancy, and with it rents. The subsequent shortage of space leads to expansion. Too much expansion leads to hyper-supply, in which too much property is competing for too-few tenants. This leads to recession. (In a very macro sense, that’s more-or-less what happened in 08/09, with the added problem that too many banks were trying to loan too much money and thus not properly pricing risk.)

The nuances of his model and report are too numerous to synopsize here. In short, he finds that on a national basis, every property type (e.g. — apartments, industrial, suburban offices) are in various stages of recovery, with the health facilities and senior housing being the closest to breaking out to expansion. Intriguingly, both limited-service and full-service hotels are following in close order.

He also tracks most of the top geographic markets in the country, and all of these are either deep in recession or in the earliest stages of recovery. No markets are close to break-out into expansion. The worst two markets (and “worst” is just relative here) are Honolulu and Sacramento, while the best (again, relative) are Austin, Charlotte, Dallas-Fort Worth, Nashville, Richmond, Riverside, Salt Lake, and San Jose. My home city of Seattle is ranked — along with a dozen others — deep in the heart of recession.