Archive for the ‘Affordable Housing’ Category

Need a job?

I pulled up behind another car at a stop light yesterday and couldn’t help but notice a license plate surround for the local construction laborers union, plus a labor bumper sticker in the back window. This attracted my attention because the vehicle in question was a late-model Cadillac Escalade.

Admittedly this may have been an outlier, but all across the U.S. there is a huge demand for entry level construction trainees. Here in Seattle (a high-wage, high cost-of-living area) entry level “no experience, no education” wages are in the high-teens per hour, rising rapidly to $50k per year with a modicum of experience. Take some winter months to go get trained in plumbing, electrical, or HVAC and the annual income gets into the high 5 to low 6 figures pretty quickly. (The average plumber in Seattle makes $95,000 per year, according to Salarylist.com.) Some sources put this number somewhat lower, but you get the point.

Ironically, these jobs are going begging, and the reasons are varied. Many young people are scared off from a job that evidently requires a lot of outdoor work and physical stamina. Yet, as one young woman in a carpenter training program noted, “If you work hard and you put in your effort, they’ll take you over somebody else who is muscle…” Baby boomers seem to think that if their children don’t go to college, they’ve failed as parents, and so the percentage of construction workers under age 24 has declined in 48 states since the peak of the housing boom.

Wall Street Journal has a great article this morning called “Young people don’t want construction jobs. That’s a problem for the housing market.” It is indeed. It is one reason why home construction per household in America is at its lowest level in 60 years of keeping records, according to the article. The reasons include lack of vocational programs in high schools, although many of these are coming back. The Home Builders Institute, affiliated with the National Association of Homebuilders, has as many as 6,000 young people in their training pipeline at any given time.

I’m not suggesting — nor is the WSJ, that flooding young people into construction jobs will change the housing affordability metric overnight. The homebuilding industry is still replete with problems such as a trade war with our principle material suppliers, a lack of housing infrastructure, and short-term financing issues. Nonetheless, young people might want to be reminded that a surprisingly large number of CEOs in the construction field got started with a hammer in their hands.

Share this:

Home prices up, sales down

Reuter’s reported this morning that sales of existing homes are down and prices are up. Economists had forecasted an increase year-over-year of 0.6%, according to National Association of Realtors statistics, which would have been a pretty good jump. In fact, sales actually fell by 2.2% from June, 2017 to June, 2018.

Sales rose in the northeast and Midwest, but fell in the west and south. Existing home sales make up about 90% of the market (the other 10% from new homes). As we’ve reported before, rising costs and lack of infrastructure are driving up new home prices and driving down new home availability. This means that demand drives up prices, and ultimately drives down volume. (This was the part of the supply/demand equilibrium lecture that drove so very many college freshmen to major in something other than economics.) Annual wage growth has been stuck below 3% for some time now, and median house prices are now up 5.2% from last year, to a record high of $276,900. According to NAR, this is the 76th consecutive month with year-to-year price gains.

Supply at the lower end of the market — starter homes and rental homes — dropped by 18% from last year. This is problematic since first-time buyers accounted for 31% of all transactions in June. However, economists estimate that in a healthy market, first-time buyers would account for a 40% market share. All in all, these are not the signs of a healthy housing market.

Share this:

Inflation outpacing wages. Fed expectations?

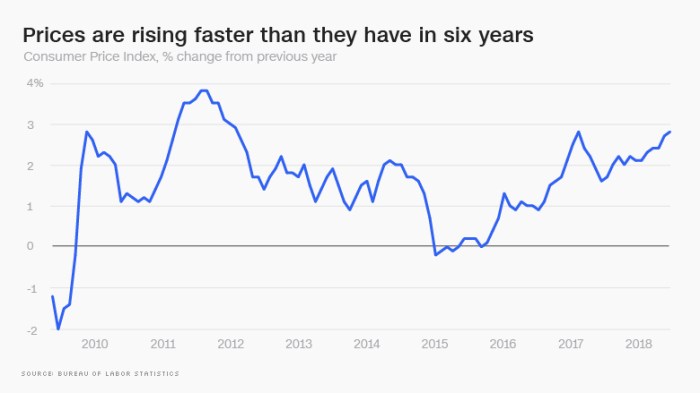

Those of us who lived through the 1970’s may think that 3% or 4% inflation is childsplay, but the FED doesn’t necessarily look at it that way. Indeed, they’re an “inflation conservative” bunch, and don’t take too kindly to the CPI heading northward.

An article this morning in CNN Money offers two painful scenarios. First, inflation is nudging up, in no small part from housing costs and health care costs. Add to that the impending impact of the coming Trade War, and the news isn’t very good.

Graphic courtesy money.cnn.com

Second – and we’ve been predicting this – consumer prices are rising higher than wages. The difference isn’t very big at the median, only 0.2 percentage points, but given the disparate increases in incomes in America of late, and the disparate consumptions patterns, this means that the burdens of cost inflation are being disproportionately felt by working families.

More to come….

Share this:

Commercial property prices

First, a happy 4th of July to all of our U.S. readers! I’ve spent the day catching up on reading, writing, and napping. I hope you’ve all done the same.

Part of my reading was a recent piece by Calvin Schnure for the members at NAREIT titled Commercial Property Prices Continue Steady Gains. It’s an interesting read, and factually correct. However, Mr. Schnure and I might arrive at somewhat different conclusions. Case in point is illustrated by the graphic below, taken from his article:

Now, if you are running a REIT and want to convince potential investors that the world is rosy, then this is a very pretty graphic. On the other hand, if you are a real estate analyst (ahem…. please hold your applause) you have to wonder what the heck is going on here. I’m particularly concerned with multi-family, which has increased in value on the order of about 60% since the previous peak (December, 2007) but is up by something close to 160% since the trough of 8 years ago. Yeah. That’s a huge run-up. Couple that with the observations (anecdotal, at present) that multi-family vacancies are on the rise nationwide, and particularly, surprisingly, in formerly hot markets like Seattle (just to name names).

I’m not preaching a long-term or even intermediate term demise for multi-family. Far from it, in the long term, these are still worth considering. However, in the short-term, these annualized gains may not be sustainable.

By the way, there’s a lot more in the NAREIT article, and it’s worth reading in its entirety.

Watch this space. We’ll keep you posted.

Share this:

And yet more on housing

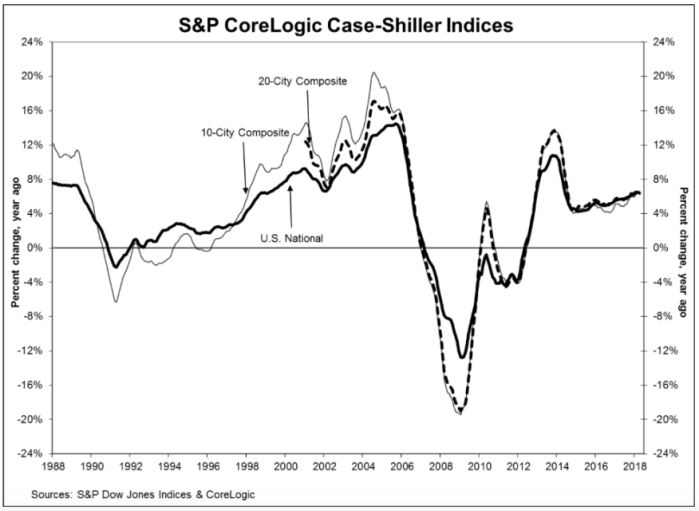

Twice burned, you know? I think we should all be a bit gun-shy about rapidly increasing house prices. Are we looking for a bubble or a peak?

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, reported a 6.4% annual gain in April, slightly down from an annualized rate of 6.5% in March. While they produce a few other indices, all of them basically report the same thing. Oh, by the way, my home city of Seattle leads the pack with an annualized rate north of 13%.

Glancing at the graphic, below, the slope of the current pricing graph looks suspiciously like what we saw during the bubble run-up. As I’ve noted here previously, house prices increasing at a rate higher than 2 points over inflation is emblematic of a bubble. That would suggest a nationwide rate somewhere around 4% – 5% right now. You do the math.

Share this:

Deconstructing house prices

I stumbled on a very interesting graphic on the inter-web the other day. I can’t provide the citation just yet — it was posted anonymously on a data visualization web site. Nonetheless, I’ve done a bit of research to semi-validate these numbers, and even if they’re off a bit, it’s a very useful graphic.

First, it tells us that since 2002, the median price of a new home in America has approximately doubled, from $175,000 to about $350,000 (depending on exactly which metrics you use, this is about right). That’s an inflation rate of about 100%, more or less, in 15 years (end of 2002 to end of 2017). In a paper I presented at the American Real Estate Society annual meetings about 10 years ago, I noted that post-WW2 data indicated that house prices/values should be expected to grow annually at a rate of about 2 percent points above the inflation rate. I checked, and the actual inflation rate over that period measured by the CPI totaled 36%, more or less. That averages about 2.1% per year, compounded. The doubling of house prices in 15 years equates to an inflation rate of about 4.7%. So…. 4.7 minus 2.1 = 2.6. Thus, by my estimation based on historical averages, house prices have been growing about 0.6% per year faster than they should have since 2002.

You might argue that some of that was the last few years of the housing bubble, but that sponge got squeezed out in the post-bubble collapse. Nope, folks, what we’re seeing is the echo bubble. You might also argue that 0.6% doesn’t sound like much, but here’s what it amounts to over time. If house prices had actually grown at the rate suggested by previous post-WW2 data, then prices would only have gone up by about 170% over that time period. That means that a $175,000 house from 2002 should today be selling for about $295,000. The difference (350,000 minus 295,000) of about 17% is the measure of the echo bubble — it’s the degree to which houses are currently overpriced.

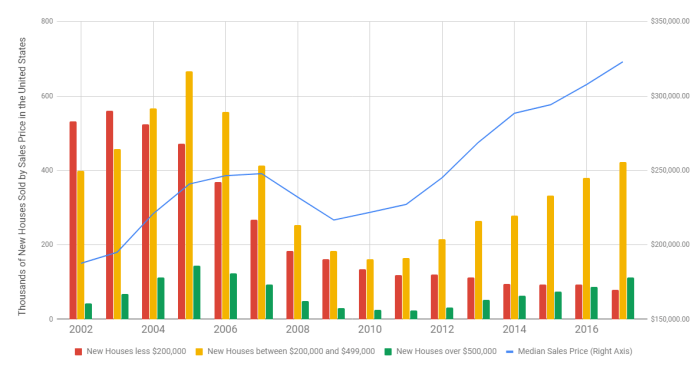

Ahem…. that’s NOT the point of this story. That’s just the introduction. The more important story comes from deconstructing house prices into various tranches. This graphic I found does a wonderful job of that:

Here’s my point in a nutshell. Note that in 2002, the plurality of homes built were in the “less than $200,000” category. Today, that’s the smallest category (the one in red). Conversely, we’re building about twice as many homes in the expensive category (the green bar) as we were in 2002. While all housing starts are down from the peak, compared to the earlier years, we’re now building the bulk of the housing in the two most expensive categories, which is a real shift from 2002.

Why? The market is constantly screaming about the lack of supply for “affordable housing”. Why aren’t builders building to that tranche of the market? The answer is cost. Two very disruptive forces are plaguing the homebuilding industry today. First, the labor and infrastructure for building died off during the recession. We have relatively fewer trained and skilled tradespeople, fewer developed lots (and a shrunken pipeline for development) and more expensive construction lending. Second, the building materials themselves — lumber and steel — are in short supply, have been affected by price increases, and are now faced with tariffs. Builders have no choice but to build more expensive homes to be able to cover the cost of construction.

Are we headed for a new bubble? Back in the dark ages, when I was in graduate school, we were taught that inflation could be caused by either demand-pull (too much money chasing too few goods) or cost-push (increases in commodity costs). Either way you look at it, the cost of owner-occupied housing is going thru the roof (pun intended).

Share this:

Lumber and other simple stuff

Tariffs anyone? Jann Swanson wrote a great piece for Mortgage News Daily last week, titled “NAHB: Lumber Shortages and Prices Hamper Affordability.” In short, the shortages of framing lumber are “now more widespread than any time” since the National Association of Homebuilders began tracking in 1994. About 31% of single-family builders reported shortages of framing lumber in the most recent survey, along with shortages in other building materials. A full 95% of homebuilders reported that prices of these materials were having an adverse impact on housing affordability.

While there are numerous reasons for this, including a shrinkage in the building infrastructure during the several years following the housing melt-down, the NAHB notes that the top five building materials with shortages are on the Trump Administrations list of tariff targets.

Share this:

So, folks, where are we going to live?

Much has been said recently about housing starts being back up to where they were before the recession. If this is the case, then why does Seattle, for example, have a 0.9 month supply of homes for sale? As usual, the details are much more complicated than the headlines.

Prior to the “meltdown” (let’s say, 2004 – 2007), housing starts in the U.S. averaged about 1.865 million units per year. Now, few analysts disagree that this was too many, but figuring out the right number is harder than one might think. In 2008, the number dipped down to about 905,000, and hit a low of 583,000 in 2009. Since then, the annual starts have trended up. However, in 2016, we still were only at 1.207 million. Of that, only 751,000 were single family units, compared to an average of 1.4 million single family homes per year in the 2004-2007 period. Hence, nationally, we’re building about half as many homes as we were 10 years ago.

From 2004-2007, we started 7.462 million dwelling units in America, but in the past four years we’ve only started a total of about 4.432 million (all varieties). That’s a shrinkage of about 3 million new homes, and most of that shrinkage is in the single family category.

One might posit that the decline in home ownership rates should have freed up some demand, and some of that’s true. The home ownership rate in America peaked at 69% during the run-up to the recession, and dropped steadily after the melt-down, to a low of 62.9% in the 2nd quarter 2016. As of the end of the 3rd quarter this year, it sits at 63.9%, or about 5 points below the peak of a decade ago.

There are about 76.146 million owner-occupied housing units in the U.S. today. A five-percent swing in this number is a little over 3.5 million houses. In short, we’ve now “absorbed” the decline in starts, and structurally we’re more-or-less “over” the recession, and we’re simply not building enough new homes to meet the demand.

Several consequences came out of the melt-down. First, developing land takes quite a few years — five or more in the “hot” areas like Seattle, where land has to go thru a permitting and entitlement phase long before a house can be built. All of this requires land planners, both in the private sector and downtown at the county or city hall. Many of these folks lost their jobs during the 2008-09 period, and indeed some county and city planning offices were eviscerated. New home development frequently requires a significant outlay in public infrastructure, including schools, roads, and utilities. Worse than that, many construction trades were gutted, with no replacements available. Financing for acquisition, development, and construction is now problematic (although, arguably, it was too liberal pre-recession).

As such, it’s a sellers market for homes, and in hot markets, buyers compete by bidding up prices beyond reasonable levels. Some pundits are nervous, and with good reason.

(Thanks to the U.S. Census Bureau for the October 31 data.)

Share this:

Low Income Housing Threatened

OK, folks, this gets complicated, so follow along with me. The Reagan era tax cuts, and specifically the U.S. Tax Reform Act of 1986, adversely affected many of the incentives for investing in low income rental housing. To provide some balance, the Low Income Housing Tax Credit (LIHTC) program was added to the Act. This program provides a tax credit which can either be used or sold by the developer.

Usually, the tax credits are sold or syndicated, and corporations that anticipate that they’ll have taxable income over the next 15 years will buy the credits, which can be used to offset future tax bills. The developer uses the proceeds from the tax credit sales as the equity for the low income housing development. Coupled with the program is a substantial emphasis on fiscal discipline (audited financial statements, regular reporting, etc.) and as such, these low income multi-family developments have had a foreclosure rate of less than 0.1%, which is far better than comparable market-rate properties.

Typically, a developer will cobble together several programs, such as FNMA debt financing, Section 8 vouchers, and state and local incentives. The LIHTC program is administered by State Housing Authorities, and of course has oversight from the IRS.

Here’s where it gets both interesting and complicated. The selling price for the credits is a function of two things — the discount rate (which is very low now-a-days) and a company’s forward-looking tax burden. Let’s say, just as an example, I believe my company will have $1 million per year in net income in the coming fifteen years. My tax rate is 40%, so I’ll end up paying $400,000 in annual federal income taxes, and I’d be willing to pay for credits which would erase that tax burden. In short, I’m agnostic as to whether I send the money to the IRS or to a developer who wants to use the money to build an apartment complex. (Actually, it’s w-a-a-a-a-y more complicated than this, but bear with me.) Now, my tax burden over the coming 15 years will be $6 million ($400,000 per year times 15), but the present value of that cash flow is what I’d pay today instead of the $6 million. If my cost of capital is 5%, the present value of that 15 year tax bill is actually closer to $4.15 million. So, I’d be willing to pay $4.15 million to avoid paying $6 million in taxes in the next 15 years. A given developer is awarded a certain level of tax credits based on the overall value of the project being proposed.

So, what’s the problem? Ahhh…. “problem” depends a bit on your perspective. As it happens, the new administration, and Congress for that matter, are bent on cutting corporate tax rates. Good for them. I own a couple of corporations. I’d like to save some money. However, if a corporation envisions that their tax bills over the next 15 years will be much lower than previously anticipated, then the amount they’re willing to pay TODAY to avoid those tax bills is much lower. How much, you say? Well, let’s assume our company had it’s effective tax rate lowered from 40% to 15%. The tax bill over the next 15 years would only be $2.25 million, and the present value of THAT is only $1.56 million. Ahem…..

I’m not knocking tax cuts, but everything has a cost, and building low income housing employs a lot of people, provides a much-needed private sector solution to a public problem, and creates investment. We’re already seeing this market dry up. An article in today’s Pittsburgh Post-Gazette, by Kate Giammarise, outlines the problems that developers are already facing. One solution may be for Congress to increase the level of available tax credits, so that developers can be left whole even with the tax cuts. This will, by its nature, be a nationwide problem.

Share this:

“5 Economic Trends to be Thankful For”

First, I hope everyone had a great Thanksgiving! For those of you who in countries that don’t share our festival of thanks, I hope you had a great Thursday!

Kuddos to Neil Irwin, writing in the Washington Post yesterday. I agree 100% with his list, and wanted to reproduce it here:

1. Household debt is way down. Neil lists this as his first item, but I would suggest it has plusses and minuses to it. On the plus column, we really WERE over-debted as a society. On the minus side, changes household debt carries with it complex implications for the consumption side of GDP, as well as corporate investment (see my prior blog post) and even trade relationships. Nonetheless, this is, on net, a good thing.

2. The cost of servicing that debt is way down — as Neil points out, from 14% of disposable income in 2007 to 10.7% today. Of course, remember that one person’s interest EXPENSE is another person’s interest INCOME. Nonetheless, this constitutes a significant wealth transfer from people who HAVE money back to people who NEED TO BORROW money.

3. Electricity and natural gas prices are falling. It’s hard to find a downside to this one. From last year, consumer natural gas prices are down 8.4%, and electric rates are down 1.2%. I would add to Neil’s analysis that more of this money is staying at home — the U.S. is well on its way to being import-neutral on energy. Of course, this has some geopolitical implications, which we’ll deal with on another day.

4. Businesses aren’t firing people. While unemployment remains high at 7.9%, at least the arrows are pointed in the right direction.

5. Housing is dramatically more affordable. Neil points out that in 2006, the typical homebuyer faced a payment equal to 41% of the average wage of a private-sector worker. Today that’s 26%. This is a combination of both lower house prices (which proportionally lowers down payment requirements) and lower mortgage interest rates.

Congrats to Neil Irwin and the Washington Post for an insightful and timely article!