Posts Tagged ‘Affordable Housing’

Deconstructing house prices

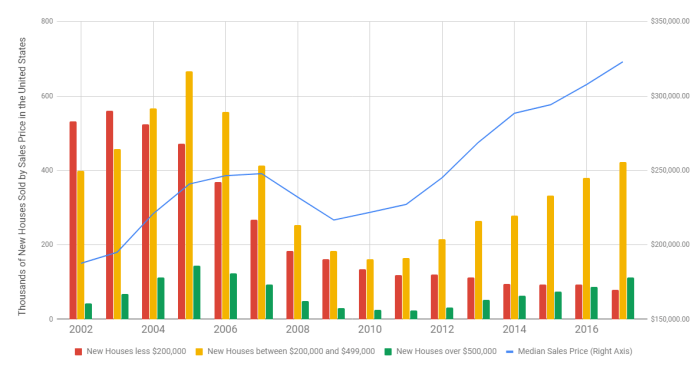

I stumbled on a very interesting graphic on the inter-web the other day. I can’t provide the citation just yet — it was posted anonymously on a data visualization web site. Nonetheless, I’ve done a bit of research to semi-validate these numbers, and even if they’re off a bit, it’s a very useful graphic.

First, it tells us that since 2002, the median price of a new home in America has approximately doubled, from $175,000 to about $350,000 (depending on exactly which metrics you use, this is about right). That’s an inflation rate of about 100%, more or less, in 15 years (end of 2002 to end of 2017). In a paper I presented at the American Real Estate Society annual meetings about 10 years ago, I noted that post-WW2 data indicated that house prices/values should be expected to grow annually at a rate of about 2 percent points above the inflation rate. I checked, and the actual inflation rate over that period measured by the CPI totaled 36%, more or less. That averages about 2.1% per year, compounded. The doubling of house prices in 15 years equates to an inflation rate of about 4.7%. So…. 4.7 minus 2.1 = 2.6. Thus, by my estimation based on historical averages, house prices have been growing about 0.6% per year faster than they should have since 2002.

You might argue that some of that was the last few years of the housing bubble, but that sponge got squeezed out in the post-bubble collapse. Nope, folks, what we’re seeing is the echo bubble. You might also argue that 0.6% doesn’t sound like much, but here’s what it amounts to over time. If house prices had actually grown at the rate suggested by previous post-WW2 data, then prices would only have gone up by about 170% over that time period. That means that a $175,000 house from 2002 should today be selling for about $295,000. The difference (350,000 minus 295,000) of about 17% is the measure of the echo bubble — it’s the degree to which houses are currently overpriced.

Ahem…. that’s NOT the point of this story. That’s just the introduction. The more important story comes from deconstructing house prices into various tranches. This graphic I found does a wonderful job of that:

Here’s my point in a nutshell. Note that in 2002, the plurality of homes built were in the “less than $200,000” category. Today, that’s the smallest category (the one in red). Conversely, we’re building about twice as many homes in the expensive category (the green bar) as we were in 2002. While all housing starts are down from the peak, compared to the earlier years, we’re now building the bulk of the housing in the two most expensive categories, which is a real shift from 2002.

Why? The market is constantly screaming about the lack of supply for “affordable housing”. Why aren’t builders building to that tranche of the market? The answer is cost. Two very disruptive forces are plaguing the homebuilding industry today. First, the labor and infrastructure for building died off during the recession. We have relatively fewer trained and skilled tradespeople, fewer developed lots (and a shrunken pipeline for development) and more expensive construction lending. Second, the building materials themselves — lumber and steel — are in short supply, have been affected by price increases, and are now faced with tariffs. Builders have no choice but to build more expensive homes to be able to cover the cost of construction.

Are we headed for a new bubble? Back in the dark ages, when I was in graduate school, we were taught that inflation could be caused by either demand-pull (too much money chasing too few goods) or cost-push (increases in commodity costs). Either way you look at it, the cost of owner-occupied housing is going thru the roof (pun intended).

Share this:

Low Income Housing Threatened

OK, folks, this gets complicated, so follow along with me. The Reagan era tax cuts, and specifically the U.S. Tax Reform Act of 1986, adversely affected many of the incentives for investing in low income rental housing. To provide some balance, the Low Income Housing Tax Credit (LIHTC) program was added to the Act. This program provides a tax credit which can either be used or sold by the developer.

Usually, the tax credits are sold or syndicated, and corporations that anticipate that they’ll have taxable income over the next 15 years will buy the credits, which can be used to offset future tax bills. The developer uses the proceeds from the tax credit sales as the equity for the low income housing development. Coupled with the program is a substantial emphasis on fiscal discipline (audited financial statements, regular reporting, etc.) and as such, these low income multi-family developments have had a foreclosure rate of less than 0.1%, which is far better than comparable market-rate properties.

Typically, a developer will cobble together several programs, such as FNMA debt financing, Section 8 vouchers, and state and local incentives. The LIHTC program is administered by State Housing Authorities, and of course has oversight from the IRS.

Here’s where it gets both interesting and complicated. The selling price for the credits is a function of two things — the discount rate (which is very low now-a-days) and a company’s forward-looking tax burden. Let’s say, just as an example, I believe my company will have $1 million per year in net income in the coming fifteen years. My tax rate is 40%, so I’ll end up paying $400,000 in annual federal income taxes, and I’d be willing to pay for credits which would erase that tax burden. In short, I’m agnostic as to whether I send the money to the IRS or to a developer who wants to use the money to build an apartment complex. (Actually, it’s w-a-a-a-a-y more complicated than this, but bear with me.) Now, my tax burden over the coming 15 years will be $6 million ($400,000 per year times 15), but the present value of that cash flow is what I’d pay today instead of the $6 million. If my cost of capital is 5%, the present value of that 15 year tax bill is actually closer to $4.15 million. So, I’d be willing to pay $4.15 million to avoid paying $6 million in taxes in the next 15 years. A given developer is awarded a certain level of tax credits based on the overall value of the project being proposed.

So, what’s the problem? Ahhh…. “problem” depends a bit on your perspective. As it happens, the new administration, and Congress for that matter, are bent on cutting corporate tax rates. Good for them. I own a couple of corporations. I’d like to save some money. However, if a corporation envisions that their tax bills over the next 15 years will be much lower than previously anticipated, then the amount they’re willing to pay TODAY to avoid those tax bills is much lower. How much, you say? Well, let’s assume our company had it’s effective tax rate lowered from 40% to 15%. The tax bill over the next 15 years would only be $2.25 million, and the present value of THAT is only $1.56 million. Ahem…..

I’m not knocking tax cuts, but everything has a cost, and building low income housing employs a lot of people, provides a much-needed private sector solution to a public problem, and creates investment. We’re already seeing this market dry up. An article in today’s Pittsburgh Post-Gazette, by Kate Giammarise, outlines the problems that developers are already facing. One solution may be for Congress to increase the level of available tax credits, so that developers can be left whole even with the tax cuts. This will, by its nature, be a nationwide problem.