Archive for February 2017

Dreams of GDP growth

Paul Krugman and I don’t necessarily agree on everything, either in politics or economics, but I respect his research (and yes, envy his Nobel Prize). That said, he has an insightful piece on his blog about The Donald’s economic projections, which both Paul and I find probably untenable. I encourage you to read it here.

In short, The Donald projects 3% to 3.5% GDP growth throughout his tenure in the White House. Under Reagan, it was at the lower end of this scale, and under Clinton it hit 3.7%. Remember that both of those presidents inherited crappy economies, and so a pendulum bounce in GDP would have been expected. The Donald is inheriting a healthy overall economy (admittedly, with pockets of problems). As such, growth in the 2+% range is more likely. So why are they projecting such glossy numbers? In short, they back into what they need to say in order to fit their rosy projections.

I would note that the Chair of the Council of Economic Advisors sits vacant as of this writing, with no nominee in the offing. This Council serves the president, among other ways, by putting a reasonableness test on just such projections. Truly excellent economists have served on this Council thru the years, from all sides of the economic spectrum (and yes, there are more than two). In the absence of trained, academic economists in this role, these projections are left up to whim.

Unlike Paul K, I have some hope that Paul Ryan may be a voice of sanity here. He seems to understand that balance sheets need to balance. Let’s see how that works out.

Share this:

The long lost shopping mall?

Common wisdom holds that the shopping mall is on life support. I venture into maybe one or two a year, and my most recent ventures weren’t very encouraging. Two recent Wall Street Journal articles illustrate the complexity of repurposing.

First, in a January 24th article by Ester Fung, “Mall Owners Rush to Get Out of the Mall Business”, the Journal notes that even the big-names in the biz are making use of strategic default to get rid of underwater properties. Citing data from Morningstar, the story detailed that from January to November 314 loans secured by retail property were liquidated, totaling about $3.5 billion. According to the story, these liquidations resulted in losses of $1.68 billion. Washington Prime, CBL and Simon have all sent properties back to lenders in recent months. Ironically, these big players have seen no dings to their credit ratings, and the equity market in fact views these put-backs as evidence of financial discipline. On the downside, surrounding properties, such as out-parcels and other nearby retailers, such as restaurants, that depend on spillover from the mall, are suffering from the loss of shopper attraction.

One alternative to strategic default is a revamping of the real estate itself. This often includes attracting a new or new type of anchor tenant or demolishing the mall entirely to make way for offices or apartments. Unfortunately, as detailed in a February 14 WSJ piece by Suzanne Kapner, existing tenants often have covenants or restrictions standing in the way of such revamping. In “Race to Revamp Shopping Malls Takes a Nasty Turn”, Ms. Kapner outlines how many department stores want to protect existing parking or existing exclusivity through “reciprocal easement agreements”. For example, large swaths of unused parking space have value for repositioning. However, as Gar Herring, chief executive of the MGHerring Group, a regional mall developer, put it, “But if you want to put a snow cone shack in a parking space furthest from the mall, you need the agreement of every department-store anchor.” Currently, for example, Sears is suing a mall developer in Florida to prevent it from adding a Dicks Sporting Goods as an anchor. Lord & Taylor filed suite in 2013 to stop a Maryland mall’s demolition to make way for offices, residential properties and a hotel. The retailer claimed violated an agreement signed in 1975 that prevents the landlord from making changes to the property without its consent.

The shopping mall is three different things. From a consumer perspective, it’s a place of gathering and consumption. Indeed, the loss of the shopping mall, which replaced Main Street, has sociological implications as well. Does Amazon.com now become a place of gathering as well as consumption? That’s an interesting subject for another day. Second, from a business perspective, the mall is a bundle of contracts, and sorting through those contracts will keep lawyers and real estate experts busy for some years to come. Finally, a shopping mall may be, in some circumstances, a valuable piece of real estate. Repositioning that real estate, either as retail with different tenants and focus, or as something other than retail, will be an interesting story in the coming years.

Share this:

Well THAT’S interesting…

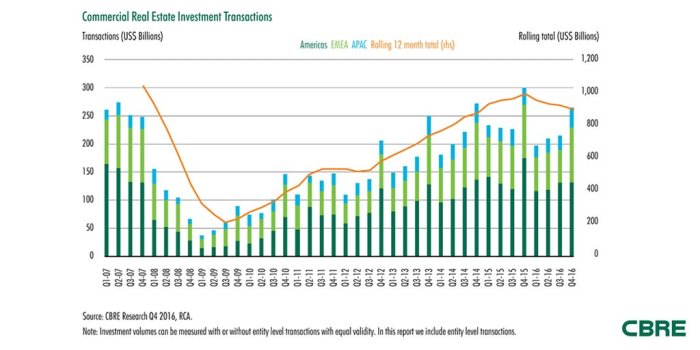

Most of the conversations I’ve had about real estate and The Donald focus on housing, and particularly the storm clouds forming over low-income housing. However, while The Donald is one of the luckiest income presidents in history in terms of inheriting a great economy, his Achilles heel may be the commercial real estate sector.

CBRE was kind enough to tweet the accompanying chart this morning, which is pretty self explanatory. (Of course, I’ll go ahead and explain it anyway.) After the real estate storm that Obama inherited, commercial transactions have regained lost ground in the past several years. Note that we peaked in 2015 with total commercial transactions of nearly $1 Trillion for the year. However, the market backed-off considerably, with the first three quarters of 2016 coming in a bit lower than the previous year, and then the 4th quarter coming in nearly $50 billion lower than the same period in 2015.

Did we just see a trend line break? One wonders. Commercial real estate feeds a lot of other sectors of the economy. For example, new construction employs lots of the sorts of jobs The Donald is promising. We need to keep our finger on this particular pulse.

Share this:

…and the next thing…

I’ve been critical of the current occupants of the White House, and particularly their apparent naivity about the economy. One might falsely surmise from my criticism that I’m a raging lefty. I would rejoinder that competence knows no political stripes. That said, I would note this morning that an economist from two leading conservative think tanks also expresses skepticism over The Donald’s trade policies.

The conservative bona fides of the Club for Growth and the Heritage Foundation are beyond question. The former bills itself as, “…the leading free-enterprise advocacy group in the nation,” while the latter is lead by former GOP Congressman and Tea Party stalwart Jim DeMint, from my former home state of South Carolina. Stephen Moore, a Heritage economist and co-founder of the Club for Growth, appeared on CNN’s Party People podcast, and said, “On trade, I think he’s playing with fire here.” He went on to say, “And I think the idea of a tariff against Mexico is a terrible idea. I think it would hurt Mexico a lot, and I think it would hurt American consumers as well. We don’t need a trade war with Mexico.” He did, however, give a tentative pass to The Donald’s attitude toward China, noting “I kind of approve of some of the things he’s doing on China.”

Full disclosure here — I don’t necessarily agree with Moore on every point he makes. Moore invokes the legacy of Harry Truman, and says that Truman got off to a rocky start but learned the Presidency quickly. I would beg to differ on the validity of Moore’s analogy. Truman had held significant local office in Missouri, was an Army Reserve Colonel, and was late in his second term as a Senator when the nod for the VP job came along. The Truman Committee in the Senate, during the war years, provided extraordinary oversight to the conduct of the war and investigated every aspect of government management during the several years he was chair. As such, Truman was probably the most prepared person to assume the presidency available at the time. (Many would have preferred South Carolina’s Jimmy Byrnes, but Byrne’s record on segregation would have made him a tough sell.)

Any “rough start” to the Truman presidency had to be taken in the context of inheriting a 2-front war, an atomic bomb, the beginnings of the cold war, massive demobilization, turning the American economy from war production to consumption, open rebellion from two wings of his own party (the Dixiecrats under Thurmond and the Progressives under Wallace) and devastation around the world. The Donald, on the other hand, has inherited a stable, growing economy, no inflation, low unemployment, and a loyal majority in both houses of congress.

Ahem…. If The Donald screws this one up, it’s all on him.

Share this:

Strong vs weak dollar

Ahem…. this may or may not be the truth, but in the words of my fellow Low-Country South Carolina expat, Stephen Colbert, it’s certainly “truthy”. Reportedly, according to Huffington Post, The Donald called his national security advisor, Flynn, at 3am, to ask whether a strong dollar or a weak dollar was good for the economy. Reportedly, Flynn told The Donald to ask an economist. Since then, economists of all stripes have offered advice, because, well, this is important stuff for a President to know, along with “war is bad” and “full employment is good” and stuff like that.

So, here we go. I’ll take a stab at it. Whenever the world roils, investors of all stripes look for stable currencies in which to invest, and the dollar is the “mother of all stable currencies”. Until Brexit, the same could be said of the Euro and the Pound. Now, not so much. Anyway, paradoxically, the election of The Donald roiled the world’s zeitgeist, causing investors to seek the dollar, and thus strengthening our currency. Now, what’s the impact? Well, a strong dollar makes it tough to export stuff, but it makes it easy to import stuff. That wrecks the trade imbalance, and costs jobs in exportive industries. Conversely, a weak dollar suggests lack of faith in the American economy, but helps with American jobs, albeit makes American consumption more expensive.

ALSO, a strong dollar makes it easy to borrow. As America runs deficits (both fiscal and trade), we have to borrow and much of this borrowing occurs in foreign markets. Conversely, a weak dollar drives up the cost of borrowing.

In short, if The Donald wants to bring American jobs home, he’ll opt for a weak dollar, but that will inevitably drive up the cost of consumption as well as the cost of borrowing. Ironically, the way to achieve a weak (or lets say, “less strong”) dollar is to achieve some sort of stability in the world, and that doesn’t seem to be in the offing.

Share this:

Low Income Housing Threatened

OK, folks, this gets complicated, so follow along with me. The Reagan era tax cuts, and specifically the U.S. Tax Reform Act of 1986, adversely affected many of the incentives for investing in low income rental housing. To provide some balance, the Low Income Housing Tax Credit (LIHTC) program was added to the Act. This program provides a tax credit which can either be used or sold by the developer.

Usually, the tax credits are sold or syndicated, and corporations that anticipate that they’ll have taxable income over the next 15 years will buy the credits, which can be used to offset future tax bills. The developer uses the proceeds from the tax credit sales as the equity for the low income housing development. Coupled with the program is a substantial emphasis on fiscal discipline (audited financial statements, regular reporting, etc.) and as such, these low income multi-family developments have had a foreclosure rate of less than 0.1%, which is far better than comparable market-rate properties.

Typically, a developer will cobble together several programs, such as FNMA debt financing, Section 8 vouchers, and state and local incentives. The LIHTC program is administered by State Housing Authorities, and of course has oversight from the IRS.

Here’s where it gets both interesting and complicated. The selling price for the credits is a function of two things — the discount rate (which is very low now-a-days) and a company’s forward-looking tax burden. Let’s say, just as an example, I believe my company will have $1 million per year in net income in the coming fifteen years. My tax rate is 40%, so I’ll end up paying $400,000 in annual federal income taxes, and I’d be willing to pay for credits which would erase that tax burden. In short, I’m agnostic as to whether I send the money to the IRS or to a developer who wants to use the money to build an apartment complex. (Actually, it’s w-a-a-a-a-y more complicated than this, but bear with me.) Now, my tax burden over the coming 15 years will be $6 million ($400,000 per year times 15), but the present value of that cash flow is what I’d pay today instead of the $6 million. If my cost of capital is 5%, the present value of that 15 year tax bill is actually closer to $4.15 million. So, I’d be willing to pay $4.15 million to avoid paying $6 million in taxes in the next 15 years. A given developer is awarded a certain level of tax credits based on the overall value of the project being proposed.

So, what’s the problem? Ahhh…. “problem” depends a bit on your perspective. As it happens, the new administration, and Congress for that matter, are bent on cutting corporate tax rates. Good for them. I own a couple of corporations. I’d like to save some money. However, if a corporation envisions that their tax bills over the next 15 years will be much lower than previously anticipated, then the amount they’re willing to pay TODAY to avoid those tax bills is much lower. How much, you say? Well, let’s assume our company had it’s effective tax rate lowered from 40% to 15%. The tax bill over the next 15 years would only be $2.25 million, and the present value of THAT is only $1.56 million. Ahem…..

I’m not knocking tax cuts, but everything has a cost, and building low income housing employs a lot of people, provides a much-needed private sector solution to a public problem, and creates investment. We’re already seeing this market dry up. An article in today’s Pittsburgh Post-Gazette, by Kate Giammarise, outlines the problems that developers are already facing. One solution may be for Congress to increase the level of available tax credits, so that developers can be left whole even with the tax cuts. This will, by its nature, be a nationwide problem.

Share this:

Economic Baseline

I just returned from a hectic several days in NYC. I have to tell you, the vibrancy of the Big Apple never ceases to amaze me. Then again, I was in Lexington, KY, week-before-last, and the core of downtown is alive with new construction. (My darling wife speaks fondly of the Kilpatrick Index of Economic Activity, which is the number of high-rise cranes I can see from my office window.) I was in Atlanta a week ago, and saw much the same, particularly in the tony suburbs of Cobb County. My own main base of Seattle is awash with new construction.

Bottom line — America is actually working pretty well right now. Unemployment is well under 5%, which is an amazing level for a developed economy. Goldman Sachs tells me that global GDP growth should be in the 3% to 3.5% range in the coming year (where it’s been for the last 5 years) driven in no small part by a healthy U.S. economy. According to tradingeconomics.com, U.S. GDP growth was 3.5% in the 3rd quarter of 2016, and is expected to come in at 1.9% in the 4th quarter. Again, for a developed economy, these are not bad numbers.

One great measure of the health of the job market is the Gallup Job Creation Index, which is a weekly survey of 4,000 working adults. It takes into account both job growth (at the respondents workplace) as well as anticipated job shrinkage. The index bottomed below zero in 2008-09, but has steadily increased since then, and now stands as high as it has since the index was started in early 2008. Inflation has been nearly non-existent for the entire century.

I point all this out, because this is the economic baseline that the Trump Administration takes over. This is what they argue they will improve upon. I don’t doubt that there are corners of the U.S. that aren’t on the same economic plane, and I would concur that we, as a nation, should direct attention in those directions. That said, for the nation as a whole, things are going quite well. Most of us in business have seen the flow chart that starts with the question, “Was it broken?” and asks, “yes” or “no”. If no, then it asks, “did you mess with it?” So, here we are, with an economy that, by and large, works pretty well for most people. Let’s see how this works out…… I’ll keep you posted.