Posts Tagged ‘commercial real estate’

Demand & Supply

I just read a nice piece by Deloitte’s Robert T. O’Brien, their Global and U.S. Real Estate and Construction Leader, titled Commercial Real Estate Outlook 2017. It’s far too interesting and too packed with info to summarize here, so have a glance for yourself. However, I’ll point out a couple of things I believe stand out in his analysis.

First, homebuilders are under pressure due to what he calls the “demand-supply dichotomy.” I’ve been concerned about this for a while. During the recession — which admittedly was several years ago — big chunks of the housing infrastructure collapsed, including acquisition-development-construction (ADC) finance, skilled labor, permanent finance securitization, and local government permitting capabilities. As such, we now actually have a bit of a housing shortage in hot areas (think “Seattle”). Mr. O’Brien worries that homebuilders’ financial projections may be dampened. I’m a bit more concerned with the upward price pressure on houses, which could put us back in a bubble situation. Deloitte believes interest rates hikes by the FED may temper some of the demand side.

He believes private equity fundraising will decline this year, “…as managers focus on deploying existing funds.” He believes managers will face increasing competition looking for good investments. I would add that new managers or managers with a new story to tell will find 2017 a bit easier for fundraising than 2016.

O’Brien also sees slowing in the commercial construction arena, and so slugging financial performance for engineering and construction firms. REITs should do well, though, albeit with continued portfolio repositioning.

Deloitte sees GDP growing about 2.5% this year and unemployment below 5%, which is in line with metrics we see here at Greenfield. They also see several things disrupting the economy both this year and in out years. The “collaborative economy” will certainly have implications for the way new start-ups use and lease commercial real estate. The internet is rapidly disintermediating brokerage and leasing services, with implications for traditional brokers. A shortage of talent in the STEM area and other shifts in the way millennials view the workplace have implications for location strategies. Speed and mode of retail delivery — the “last mile” disruptions of Amazon — are still being sorted out.

Share this:

Well THAT’S interesting…

Most of the conversations I’ve had about real estate and The Donald focus on housing, and particularly the storm clouds forming over low-income housing. However, while The Donald is one of the luckiest income presidents in history in terms of inheriting a great economy, his Achilles heel may be the commercial real estate sector.

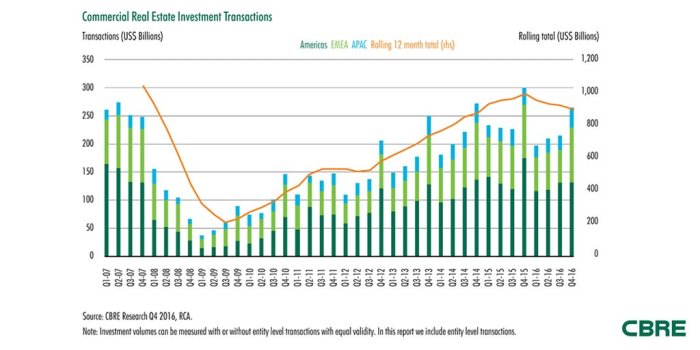

CBRE was kind enough to tweet the accompanying chart this morning, which is pretty self explanatory. (Of course, I’ll go ahead and explain it anyway.) After the real estate storm that Obama inherited, commercial transactions have regained lost ground in the past several years. Note that we peaked in 2015 with total commercial transactions of nearly $1 Trillion for the year. However, the market backed-off considerably, with the first three quarters of 2016 coming in a bit lower than the previous year, and then the 4th quarter coming in nearly $50 billion lower than the same period in 2015.

Did we just see a trend line break? One wonders. Commercial real estate feeds a lot of other sectors of the economy. For example, new construction employs lots of the sorts of jobs The Donald is promising. We need to keep our finger on this particular pulse.

Share this:

PWC Surveys Investors

PriceWaterhouse Coopers does a great job with they’re quarterly survey of commercial real estate investors. Previously known as the Korpacz Survey, after it’s founder, Peter Korpacz, the lengthy but highly readable review gives investors, brokers, appraisers, and others a snapshot of anticipated market performance both by property type (retail, office, etc.) and market (regional, and in some cases by metro area). The most recent issue just hit my desk, and as usual it’s terrifically informative.

The headline this quarter is, “Investors Scrutinize Cash Flow Assumptions”. As it turns out, the assumptions and resultant aggressiveness (or lack thereof) varies significantly by property type and geographic market. For example, strip shopping centers (nationally), apartments (also nationally), and regional warehouses in the pacific and east-north-central regions are enjoying increased optimism, measured by very significant declines in overall capitalization rates. On the other hand, 20% of investors surveyed expect regional mall cap rates to increase over the next six months, and 40% of investors felt the same about the overall Denver market.

Intriguingly, cap rates in CBDs trend lower than in the suburbs of those same cities, driven mainly by higher barriers to entry and a lack of available land downtown. Additionally, most downtown cores in major markets provide the sort of 24/7 lifestyle and transportation alternatives that appeal to younger workers, and hence the firms that employ them. As such, the downtown locations are viewed as less risky, overall.

Overall, vacancy rate assumptions have remained steady over the past year. Coupled with that, tenant retention rates have also remained steady across markets.

In general, office markets remain fundamentally strong, and PWC survey respondents project falling vacancy and rising rental rates over the next few years. Retail market conditions are improving, with no major markets currently in recession and an increasing number in expansion. In the industrial sector, the expansion of the past few years is likely to abate, according to the survey, and a few metros may find themselves in the overbuilt state (Austin, Jacksonville, Las Vegas, Portland, and DC). Apartments will continue in expansion in many markets, but the peak may be near, and an increasing number of markets are reported to be in contraction as 2015 turns into 2016.

As noted, the report is detailed, and this issue also features their less frequent surveys of medical office markets, development land, and student housing. For your own copy (they come at a subscription cost, by the way) visit www.pwc.com/realestatesurvey.

Share this:

Mueller’s Market Cycle Monitor

Sorry it’s been so long — I’ve been traveling a good bit lately, and it’s hard to keep up!

One of my favorite real estate pieces hit my desk while I was gone — Dr. Glenn Mueller’ Market Cycle Monitor, published by Dividend Capital. He developed this model about 15 years ago, and it tracks occupancy and absorption of major commercial property types in about 50 geographic markets. As a property type (in a given market) sees increasing occupancy, market participants bring new property on-line. This creates an expansion. At the peak of the expansion curve, “hypersupply” begins, following which the new supply exceeds the market ability to absorb property. Vacancy rates increase, even as new property is still coming on line. This stimulates a recession. During the recession, no new property comes on-line, and occupancies hit a nadir. At that point, natural expansion of the economy stimulates a recovery, during which excess properties are absorbed and the cycle continues. The following, taken from Dr. Mueller’s excellent 1995 paper, captures the entire idea:

Currently, the market can be best described as “flat-lined”. Office occupancies were flat during the first quarter, and rents were actually down slightly (0.3%, on an annual basis). Industrial occupancies improved slightly, but rents actually fell signficantly (3.1% annualized). APartment occupancies improved slightly, and rental growth improved significantly (2.8% annually). Retail occupancy actually improved significantly, but rental growth trended downward (3.1% annually). Finally, hotel occupancies improved a bit (0.8%), and hotel income (measured as RevPAR, or Revenue per available room) increased 8.9% on an annualized basis.

For a complete copy of Dr. Mueller’s report, click here or write us at info@greenfieldadvisors.com.