Inflation and Real Interest Rates

This morning, the Philadelphia FED released an “update” to their periodic inflation report. “Updates” should always get your attention, and this one is particularly loaded with questions and, perhaps, a few answers.

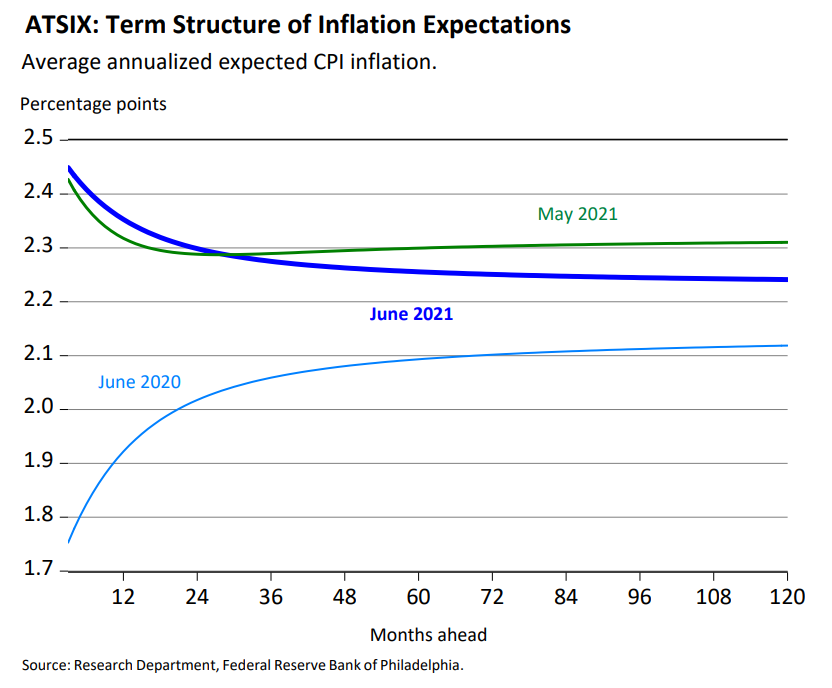

First, the Phily FED’s forecasts interest rates over the next 10 years using a hybrid model that combines information from the yield curve plus a Delphi-type survey of professional forecasters. A year ago (June, 2020), their model forecasted very low short-term inflation, rising to about 2% – 2.1% in the longer term. However, inflation fears led to revisiting the model in May, and at that time, the inflation curve had flipped — somewhat higher short-term rates (about 2.4+%) and then calming down to about 2.3% in the longer term. Today (June, 2021), the short-term inflation rate is still expected to come out in the 2.4% range, but inflation should settle out a bit lower (roughly 2.25%) in the future.

However, this model is highly dependent on real versus nominal interest rates, and right now, under any reasonable estimates of inflation, real rates are negative. Indeed, for the past 20 years, real rates have generally trended downward, with some occasional hic-cups into positive territory. While the outlook for real rates is somewhat more positive than it was a year ago, forecasters still see negative rates for the coming decade.

Before returning to the topic of inflation, it may be useful to explore how and why real rates would be negative. This may seem counter-intuitive — why would I PAY YOU to borrow my money? To consider that, it’s helpful to recall from ECON 101 the four principal factors of production: Land, Labor, Capital, and Entrepreneurship. The value of any of these at any point in time is dictated by its marginal productivity. For example, the marginal productivity of labor is the amount of value-added to the system by an additional unit of labor. Unfortunately, not all labor has the same value. Right now, for example, there is a high value-added for truck drivers, skilled trades persons (e.g. — electricians, plumbers) and health care workers. Conversely, there is very little value-add for unskilled (counter staff at a fast food joint). As such, employers for unskilled workers have little incentive to pay a penny higher than minimum wage, and employees have little incentive to work for those minimum wages. Hence, we have the paradox of a shrinking workforce and unfilled jobs.

As for interest rates, the system is awash with funds. Automation has made production extremely efficient, and so a lot of money gets spent — and thus multiplied in the system — with little demand for borrowing or investment. Even though returns to equity have been quite good of late, and are forecasted to continue to be good, there are lots of structural reasons why some tranches of capital need to go into bonds. Hence, there is a surplus of lendable capital and surprisingly little demand for that capital, driving down real interest rates. If nominal short-term rates are, say, 0.5%, but inflation is 2%, then the real rate of interest is (0.5 – 2.0 = ) negative 1.5%. That’s the world we live in today, and the world that market participants forecast for the next decade at least.

But, back to inflation. If the Phily FED has a model that depends on the somewhat flawed yield curve as well as a Delphi-like survey of forecasters to guess at inflation, how good can that model be? Yes, it’s the model we all use, but anecdotal evidence suggests some contrarian thinking may be deserved right about now. While models like this are used to forecast inflation, the actual measure of inflation comes from the Consumer Price Index, which tracks the prices of a basket of goods and services used by a typical household. Certainly, there are discussions about what goes into that basket and how those constituents ought to be weighted. Nonetheless, this is supposed to reflect how a consumer experiences actual pocketbook issues. Unfortunately, it’s not an instantaneous measure, and so we don’t actually know what inflation was until a while after it happens. However, we can examine anecdotal evidence and perhaps understand why both consumers and sophisticated researchers and investors are raising the red flag.

Clearly, some components of the basket of goods and services are all over the map. Gasoline is most likely just a rebound from a year ago when no one was on the road. Coffee is a head scratcher (although my local grocery is running a sale, so go figure…) and certainly residential real estate is giving us all pause.

So, is inflation a problem or are the models correctly forecasting that the shorter-term spikes will ameliorate over time? One thing that is obvious is that a lot of capital is being converted into real estate right now. In part this is a flight to safety, but in part it is simply a reflection of the negative returns in to bonds.

As always, if I can elaborate on any of this, or answer any of your questions, please let me know.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Leave a comment