Posts Tagged ‘Yield Curve’

Why things suck, part deux

The Bureau of Labor Statistics just released the 94th consecutive positive monthly jobs report. This is nearly a record, and should be great news. Indeed, the zeitgeist among the workforce should be euphoric. Should be, anyway….

Of course, the devil’s in the details, and our good friends at Seeking Alpha, normally a bullish lot, took the liberty of dismembering the trends and statistics, and have found some trouble right here in River City (and everywhere else, for that matter). For sure, there has been nattering from both the learned and les gens ordinaires about things like “underemployment” and “wage growth”. Indeed, my own earlier column, Why Things Suck, demonstrated that for the last 40+ years, wages in America have not kept up with the cost of living, and the cumulative differential is now huge. In other words, folks are getting jobs, but those jobs really suck.

The folks at Seeking Alpha did something more interesting, though. They looked at cycles and trends, and particularly those relative to the onset of recessions. (Note that I looked at this same trend with respect to the Yield Curve back in late August.) In an article on Thursday titled “Employment: It’s the Trend That Matters”, Lance Roberts did a great job of dismembering the current news into the key and critical trends.

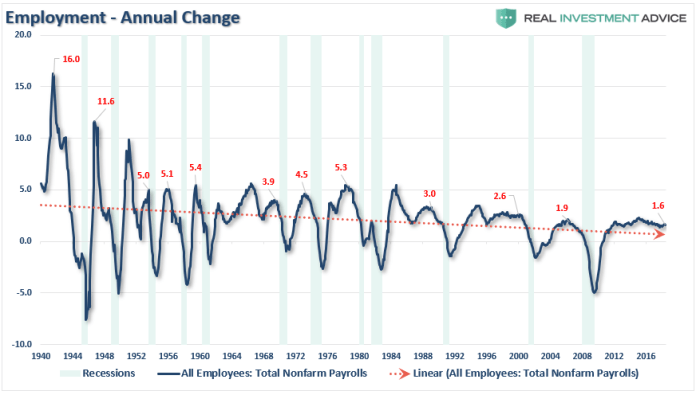

He starts off with giving the devil his due — the seasonally adjusted trend line in employment is sharply upward. However, when you take a peek at some of the underlying issues, you come away with some very different information. Workforce participation stinks, in no small measure due to the fact that over-55 workers are staying in the workforce, to an extent crowding out younger workers. He notes that for many of these older workers, retirement is simply not an option today. Many of these folks will simply have to work until they die.

More to the point, though, the actual rate of change in employment is trending downward, both in the long-term and the short-term. Roberts goes back several decades and finds that the general employment trend in America, as a rate-of-change percentage, is downward.

Courtesy Lance Roberts, Real Investment Advice

In short, when you take a simple linear trend over the last 3/4 of a century, back as far as we’ve been keeping good data, the suggestion is that our workforce growth is really declining. This has some broader implications for a maturing economy with a lot of upscale opportunities, a lot of service-oriented jobs, and not much in the middle.

Of more immediate concern, though, the jobs numbers, while positive, are trending in a way that suggests a recession is not far off in the future. Recall in my article about the Yield Curve I noted that this market looked a lot like some other trends we’d seen before. Roberts doubles down on that with employment numbers.

Courtesy Lance Roberts, Real Investment Advice

In the end, Roberts issues an homage to those of us who watch yields more closely than employment, noting that one or the other — yields or employment — will soon break. His question is, which first?

Share this:

Yield Curve Inverting

There has been a good bit said lately about the yield curve inverting. Historically, so they say, an inverted yield curve forecasts a recession. I decided to explore that concept a bit. Like all generalizations, this may have a grain of truth in it, but there is more than meets the eye.

By the way, this topic has been explored in greater depth, and with more granular data, by economists who actually focus on this topic. (Just as a reminder, my area is Real Estate Securities). If you are reading this with an eye to fleshing out some masters thesis somewhere, I’d suggest you keep looking for authorities. That said, the FED leadership is meeting in Jackson Hole this weekend, and you can bet this is on the agenda.

Speaking of the FED, I grabbed a bit of data from them — monthly 10 year treasuries and 6 month bills back to December, 1958. I actually explored some other time periods and even daily data, but this was the best pairing I could get in short order. Anyway, the “shape” of the yield curve is essentially the gap between these longer term rates and the shorter term ones. For a normal yield curve, the long bonds (10 year) should be about 2 to 4 percentage points above the short term yields. That makes some intuitive sense — in “good times”, borrowers are willing to pay more to borrow longer term, and investors are willing to accept less return for shorter term loans. When borrowers sense that there may be trouble ahead, they are less willing to borrow long-term, and hence the demand for long term money falls relative to short-term stuff. When things go really topsy-turvy, the short-term money is actually more expensive than the longer term, because borrowers simply don’t want to borrow long-term at all. The topic is w-a-a-a-a-y more complex than this, but hopefully you get the picture.

Speaking of pictures, I then took the difference between these two yields and graphed it. Along with that, I graphed the incidence of all of the recessions since 1958. Here’s what I got:

Data courtesy Federal Reserve, graphic (c) Greenfield Advisors, Inc.

Not EVERY inversion was followed immediately by a recession. although almost all were. The only exception was in 1966. That one is generally considered a “false positive” because it was triggered not by general economic trends but by a short-term reduction in Federal spending.

More interestingly, though, is the long-term bull market of the 1980’s, which was followed by the recession of 1991. That long-term market followed the double-dip recessions of 1980 and 81, which are often considered one long recession. (I know — I was there.) More to the point, the recession of 1991 was not following a yield curve inversion. Indeed, the yield curve spread, measured on a monthly basis, never got below 0.38%, in November, 1989. Also, notably, the behavior of the yield curve over the course of the 1980’s mimics what we’ve been seeing of late.

There is also an argument that rates are behaving more like the 1992-2000 period, and there is some rationale for that. If that’s the case, then the question is whether the yield curve recovers from here or takes a swan dive below zero. If the former, then we may have 2 years or so of continued positive GDP. If the latter, then we’re headed for a rough patch.

The yield curve spread ended July at 0.78%, and closed yesterday down at 0.59%. Again, this is the data the FED leadership is discussing in Jackson Hole. We’ll keep you posted.

Share this:

Livingston Survey

I’ve noted in the past that one of my favorite economic forecasts comes from the Philadelphia FED. The semi-annual Livingston Survey captures the sentiments of 28 leading economic forecasters on key metrics, such as unemployment, GDP growth, and inflation. Year after year, the forecast remains fairly accurate and steady — much to the disappointment of politicians who fail to realize that the worlds largest non-centrally-planned economy changes course fairly slowly.

Of course, 2017 may be a bit of an exception. Indeed, so was 2009. The forecast can’t take into account shocks to the system (such as the recent economic melt-down) nor can it handle significant policy shifts from D.C. I have some “gut” feelings that differ a bit from the Livingston folks, and I’ll note those at the end.

Now, on to the details. GDP growth for the second half of 2016 was a bit better than had been previously forecast, coming in at about 2.7% rather than the previously forecast 2.4%. Looking forward, the forecasters project a 2.2% annualized growth in the economy during the first half of the coming year, rising slightly to 2.4% in the second half of 2017.

Ironically, unemployment appears to be coming in slightly higher than forecasted, about 4.9% rather than the previously projected 4.7%. Of course, neither of these numbers is anything to complain about. Forecasters look to continued improvement in the unemployment numbers through the coming year, ending up around 4.6% next December.

Inflation measured by the consumer price index (CPI) is right on target at 1.3%. Next year, forecasters are projecting 2.4% (slightly up from previous 2017 forecasts) and the crystal balls (which is all they are this far out) suggest 2.5% in 2018. The yield curve is ending the year a bit steeper than previously projected. Earlier forecasts put the short end (3-month T-Bill) at 0.75% and the long end (10-year) at 2.25%. Currently, they see the year ending at 0.55% and 2.3% respectively. For 2017, the soothsayers forecast a year-end 1.12% at the short end and 2.75% at the high. This is somewhat higher at the high end and lower at the near end than had been projected previously, suggesting an expectation of higher overall interest rates in the future. Finally, forecasters see the stock market rising over the next two years, but at a fairly lackluster rate.

I promised my own bit of forecasting. During the tumultuous months surrounding the recent melt-down, I played a bit of follow-the-leader with this survey, and went on record that the melt-down would be short-lived. Boy was I wrong! As noted, this survey is pretty good when the economic ship is on a steady course, but doesn’t handle rough water very well. For the past several years, we’ve had an unprecedented period of economic growth, by all metrics (GDP, stock prices, unemployment, and inflation). Just from a pure market-cycle perspective, we may be overdue for some unpleasantries. Looking at the political horizon, I’ve already noted that politicians are generally disappointed that the economy doesn’t move as quickly as they wish or even in the desired directly. That said, we have a Congress that is frothing to trim the Federal budget, and will probably opt to do so in the transfer payments arena (welfare, health care subsidies, etc.). They’ll hope to balance this with tax cuts. However, tax cuts fall slowly, and on one sector of the economy, while entitlement cuts (and any budget cuts, for that matter) happen quickly and are usually borne by a different segment of the economy. I think I’ll be watching GDP reports fairly closely for the next couple of years. I would note what happened in the years leading up to the 1982 recession — not withstanding inflation (driving nominal interest rates), the economy looked OK in 1981, and the metrics were generally pointed in the right direction. (For a good visual representation, I’d refer you to the August, 1981, report to Congress of the Council of Economic Advisors, a copy of which you can view on the St. Louis FED’s website by clicking here.)

All in all, we’ve been focused on politics for the past several months, and now we’re going to find if those political decisions have actual economic repercussions. Stay tuned!