Archive for June 2021

Inflation and Real Interest Rates

This morning, the Philadelphia FED released an “update” to their periodic inflation report. “Updates” should always get your attention, and this one is particularly loaded with questions and, perhaps, a few answers.

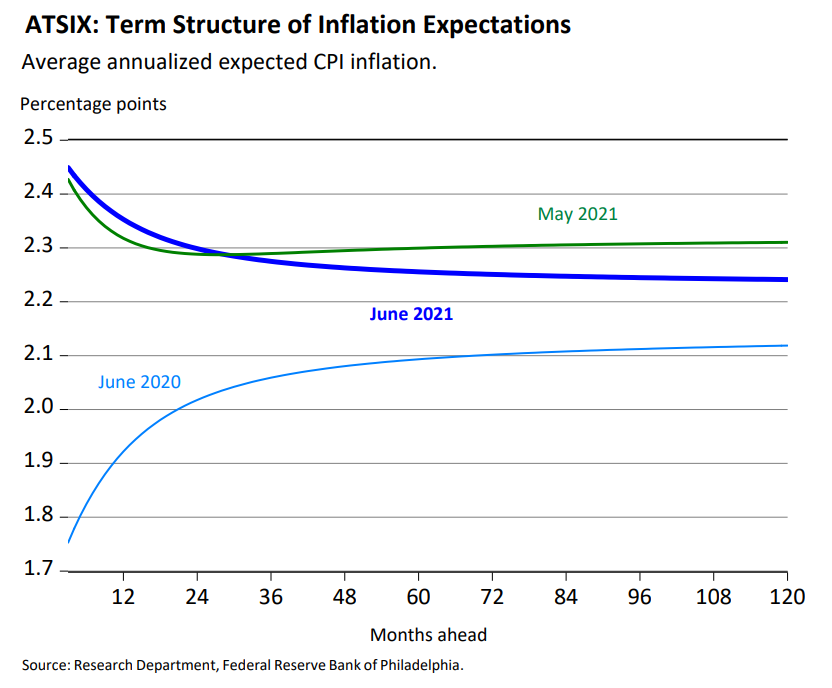

First, the Phily FED’s forecasts interest rates over the next 10 years using a hybrid model that combines information from the yield curve plus a Delphi-type survey of professional forecasters. A year ago (June, 2020), their model forecasted very low short-term inflation, rising to about 2% – 2.1% in the longer term. However, inflation fears led to revisiting the model in May, and at that time, the inflation curve had flipped — somewhat higher short-term rates (about 2.4+%) and then calming down to about 2.3% in the longer term. Today (June, 2021), the short-term inflation rate is still expected to come out in the 2.4% range, but inflation should settle out a bit lower (roughly 2.25%) in the future.

However, this model is highly dependent on real versus nominal interest rates, and right now, under any reasonable estimates of inflation, real rates are negative. Indeed, for the past 20 years, real rates have generally trended downward, with some occasional hic-cups into positive territory. While the outlook for real rates is somewhat more positive than it was a year ago, forecasters still see negative rates for the coming decade.

Before returning to the topic of inflation, it may be useful to explore how and why real rates would be negative. This may seem counter-intuitive — why would I PAY YOU to borrow my money? To consider that, it’s helpful to recall from ECON 101 the four principal factors of production: Land, Labor, Capital, and Entrepreneurship. The value of any of these at any point in time is dictated by its marginal productivity. For example, the marginal productivity of labor is the amount of value-added to the system by an additional unit of labor. Unfortunately, not all labor has the same value. Right now, for example, there is a high value-added for truck drivers, skilled trades persons (e.g. — electricians, plumbers) and health care workers. Conversely, there is very little value-add for unskilled (counter staff at a fast food joint). As such, employers for unskilled workers have little incentive to pay a penny higher than minimum wage, and employees have little incentive to work for those minimum wages. Hence, we have the paradox of a shrinking workforce and unfilled jobs.

As for interest rates, the system is awash with funds. Automation has made production extremely efficient, and so a lot of money gets spent — and thus multiplied in the system — with little demand for borrowing or investment. Even though returns to equity have been quite good of late, and are forecasted to continue to be good, there are lots of structural reasons why some tranches of capital need to go into bonds. Hence, there is a surplus of lendable capital and surprisingly little demand for that capital, driving down real interest rates. If nominal short-term rates are, say, 0.5%, but inflation is 2%, then the real rate of interest is (0.5 – 2.0 = ) negative 1.5%. That’s the world we live in today, and the world that market participants forecast for the next decade at least.

But, back to inflation. If the Phily FED has a model that depends on the somewhat flawed yield curve as well as a Delphi-like survey of forecasters to guess at inflation, how good can that model be? Yes, it’s the model we all use, but anecdotal evidence suggests some contrarian thinking may be deserved right about now. While models like this are used to forecast inflation, the actual measure of inflation comes from the Consumer Price Index, which tracks the prices of a basket of goods and services used by a typical household. Certainly, there are discussions about what goes into that basket and how those constituents ought to be weighted. Nonetheless, this is supposed to reflect how a consumer experiences actual pocketbook issues. Unfortunately, it’s not an instantaneous measure, and so we don’t actually know what inflation was until a while after it happens. However, we can examine anecdotal evidence and perhaps understand why both consumers and sophisticated researchers and investors are raising the red flag.

Clearly, some components of the basket of goods and services are all over the map. Gasoline is most likely just a rebound from a year ago when no one was on the road. Coffee is a head scratcher (although my local grocery is running a sale, so go figure…) and certainly residential real estate is giving us all pause.

So, is inflation a problem or are the models correctly forecasting that the shorter-term spikes will ameliorate over time? One thing that is obvious is that a lot of capital is being converted into real estate right now. In part this is a flight to safety, but in part it is simply a reflection of the negative returns in to bonds.

As always, if I can elaborate on any of this, or answer any of your questions, please let me know.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Share this:

Real Estate Investing 101

OK, maybe not 101… but certainly this is a pretty basic primer. Real estate is an excellent inflation hedge and provides diversification to a broader portfolio of assets. If you want liquidity (and this is true with any sort of investment) you may have to give up some potential returns by investing in publicly traded REITs. If you are willing to give up liquidity, you can potentially achieve higher returns with either direct investments or some pooled investment, such as a private equity or hedge fund. Either way, higher potential returns usually entail higher risks, and so diversification is key. I frequently use the word “curated” to describe a carefully selected and managed portfolio of real estate assets.

There’s more, but that’s a good start. So if this is so basic, why was the market shocked — SHOCKED, I say! — when Scotland-based Aegon shut down it’s £381 million property fund last week and Aviva shut down its £367 million fund due to liquidity problems. It comes as no surprise that Brexit has been a real mess for investments in the UK, and coupled with the pandemic, liquidations in British property funds have outstripped new investments. Aegon said last week that they hoped to begin distributions in the 3rd quarter, and it would take a year or two to get the money out to everyone. Apparently the same is expected for Aviva.

This says a lot about investments in the UK in general, and particularly the future of real estate in the UK in the post-Brexit, post-Pandemic world. It also says something about whomever had been investing in these funds in the last year or two. However, it says very little about real estate in general.

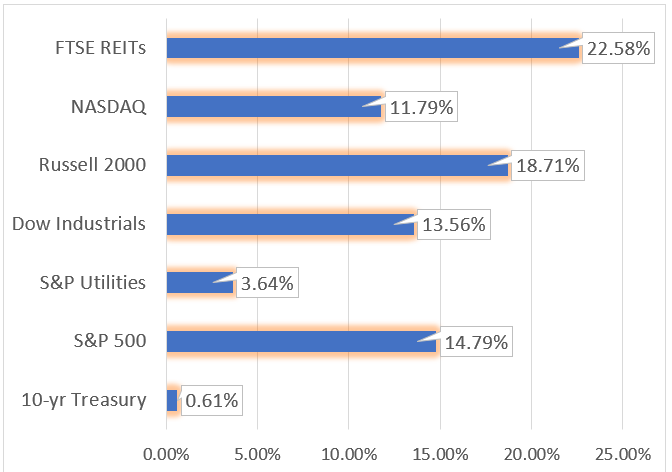

Here in the U.S., we know that some sectors are having some problems. Retail, for example, looked like it was going to completely tank last year, but then rebounded this year after we started making some headway on COVID. Of course, some funds are dug in too deep (see my recent commentary on Washington Prime Group, here) but we’ve been fully invested with ACCRE throughout the pandemic, and while this hasn’t always been a smooth ride, care and caution have paved the way. However, even an index fund of REITs this year has outperformed other indices, as shown below from the Financial Times FTSE index:

I hope this helps a bit. As always, if I can answer any questions, please let me know.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Share this:

US Global Leadership Coalition

This may sound wildly off the subject, but last week I had the very real privilege of attending (via Zoom) the US Global Leadership Coalition’s annual Global Impact Forum, followed up by a day-long “virtual” visit to Capitol Hill to meet with several members of Washington State’s congressional delegation and/or their staffs. I was invited to join the Advisory Council for USGLC back in 2020, and I’ve thoroughly enjoyed and appreciated the interaction.

Yes, my focus is on real estate finance and economics, and we usually think of real estate as being highly localized. However, real estate finance and investment is truly global. Just take a peek at a the holdings of any random sovereign wealth fund to confirm this. The vigor and vitality of America’s real estate market depends in no small part on America’s economic leadership in the world, and USGLC is focused directly on that.

Speakers at the Forum included a panoply of luminaries, such as former NATO commander Admiral Jim Stavridis, CEO of “Save the Children” Janti Soeripto, Deputy Sec. of State Wendy Sherman, Sen. James Risch (R-Id), “CARE” CEO Michelle Nunn, UN Foundation CEO Elizabeth Cousens, among many others. USGLC brings together more than 500 businesses and non-profit organizations to engage policymakers in D.C. and around the country to build support for America’s International Affairs Budget. “In today’s interconnected world, America must use all its instruments of national security and foreign policy to ensure we keep our citizens safe, strengthen our economy, and save lives. Our nation’s civilian tools of diplomacy and development are underfunded and undermanned, which is why the USGLC supports a strong and effective International Affairs Budget.” Former Sec. of State Gen. Colin Powell (USA-Ret) heads up the Advisory Council, and Admiral Jim Stavridis (USN-Ret) and Gen. Anthony Zinni (USMC-Ret) head up the National Security Advisory Council.

America’s international aid budget takes up a surprisingly small portion of our overall fiscal picture — less than 1%. However, we gain enormous leverage via that chunk of the budget, and any top military leader will tell you that diplomacy is cheaper than bullets. Our strong military, coupled with our international leadership, sets the stage for America’s powerful economy. “America’s diplomats and development workers help put the building blocks in place so that U.S. companies can expand their exports, reach new markets, and create more jobs here at home. With 95% of the world’s consumers outside of our borders and the fastest-growing markets in developing countries, it’s vital that we stay competitive in the global marketplace, ensure a level playing field for American businesses, and reach more customers.”

John A. Kilpatrick, Ph.D. — john@greenfieldadvisors.com

Share this:

Monday, Monday…

Washington Prime Group (WPG) filed for Chapter 11 reorganization late last evening, saying that COVID-19, “created significant challenges.” The stock dropped 55% in early trading this morning (although had rebounded somewhat by mid-day), and is down almost 60% on the year.

This apparently came as a bit of a surprise to the market. While equity REITs in general had a down year in 2020 (-5.12%), retail REITS performed the worst of any sector, down 25.18% overall, with regional malls leading the way at negative 37.15%. However, as of the end of the 1st quarter (the most recent data available to us), retail REITs were back on track, having clawed back most of their 2020 losses. (Overall, US Equity REITS had a total return of 8.32% in the first quarter, 2021.) WPG had a lackluster year, and from Dec 31 to May 28 was down 56%. However, it was in a rebound mode in June, having tripled in price by the beginning of last week. No analysts were rating WPG as a “buy”, but two were rating it a “hold” as of two weeks ago. Intriguingly, since the first of the year, numerous class-action suits had been filed against WPG, alleging they concealed the true financial picture from shareholders. Notably, as of their annual report in March, they had disclosed some “potential deleveraging or restructuring transactions” with certain holders of senior notes.

WPG owns about 100 shopping malls throughout the US., but mostly east of the Mississippi. They invest in a variety of retail malls, including both open-air and enclosed malls. Major tenants include Signet Jewelers, Dick’s Sporting Goods, Footlocker, Jared’s, Kay Jewelers, and ales Jewelers. As of their annual report, 59 stores comprising 4% of total rents were on their high credit watch list.

At Greenfield, in our in-house REIT fund “ACCRE”, we have purposely avoided long positions in retail since the beginning of the pandemic. For those of you tracking ACCRE, I might note that as of mid-day today. ACCRE was up 7.5% for the month, compared to less than 1% for the S&P 500.

As always, if you have any questions regarding real estate in general or your real estate investments, please don’t hesitate to reach out.

John A. Kilpatrick, Ph.D., MAI — JOHN@GREENFIELDADVISORS.COM

Share this:

ACCRE Report, May, 2021

We have mixed emotions when ACCRE beats the S&P 500. ACCRE is a diversifying adjunct to a well rounded portfolio. Hence, we want to see both ACCRE and the broader index do well each month. After a rocky year, ACCRE put together two great months — April we were up 2.94% followed by a 3.25% return in May. While the broad index had a super April (up 5.62%) it was flat in May, only up 0.55%. The global real estate metric has been positive for four months in a row, most likely emblematic of the continued positive sentiment for real estate as the economy gets back on its feet.

A dollar invested in ACCRE at the inception would be worth $1.61 today. Of course, that same dollar invested in the S&P 500 would be worth $1.78, having enjoyed the great “bull” run that started about 14 months ago. If you had invested that dollar in the S&P Global Real Estate index, you’d have $1.34 today. ACCRE is a carefully curated fund of REITS, with a goal of achieving liquidity, diversification, and superior returns.

Thanks also to the 14-month bull market, the risk-adjusted returns for the S&P continue to dominate, as evidenced by the Sharpe Ratio, as shown below. Again, the Sharpe Ratio measures the average daily returns (daily return minus the T-bill rate) divided by the standard deviation of those returns. In short, it tells you how much return you get for every unit of risk. In long bull markets, with little variation over time, the Sharpe Ratio is expected to be highly positive, as we see below. The correlation between ACCRE and the S&P over time is about 50%. This is our goal — to move in more-or-less the same direction but to offer some portfolio attenuation via diversification.

| S&P 500 | |

| Average Daily Excess Return | 0.0494% |

| Standard Deviation | 1.2908% |

| Sharpe Ratio | 3.8296% |

| ACCRE | |

| Excess Return | 0.0389% |

| Standard Deviation | 1.1947% |

| Sharpe Ratio | 3.2572% |

| Correlation (life of the fund) | 51.8333% |

| Correlation (month of May, 2021) | 43.0532% |

As always, if you have any questions about ACCRE, about REIT investing, or real estate investing in general, please drop us a note. We’re always glad to hear from you!

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com