Economies of Scale in Real Estate

In MBA school, students learn about economies of scale. The concept is pretty simple — the more of something you do, the more you can flatting out overhead. Let’s put this in the most basic terms. Joe owns a small plumbing company. He has to buy a truck and tools and a supply of plumbing gadgets. If he only services one customer a day, he may barely break even. However, if he can service 10 customers per day, he might be able to hire a cheap apprentice and make a lot of money. Economies of scale. Get it?

Mostly, students are shown graphs that look like this:

The implication is pretty straightforward — if we can just build a bigger and bigger algorithm, we can own the universe. Indeed, some real estate companies have certainly tested the boundaries of this idea. Until the mid-1990’s, most REITs were fairly small, compared to today. Sometime around 1996, there was a systemic shift upward in the size of REIT IPOs, and today, REITs are orders of magnitude larger than they used to be.

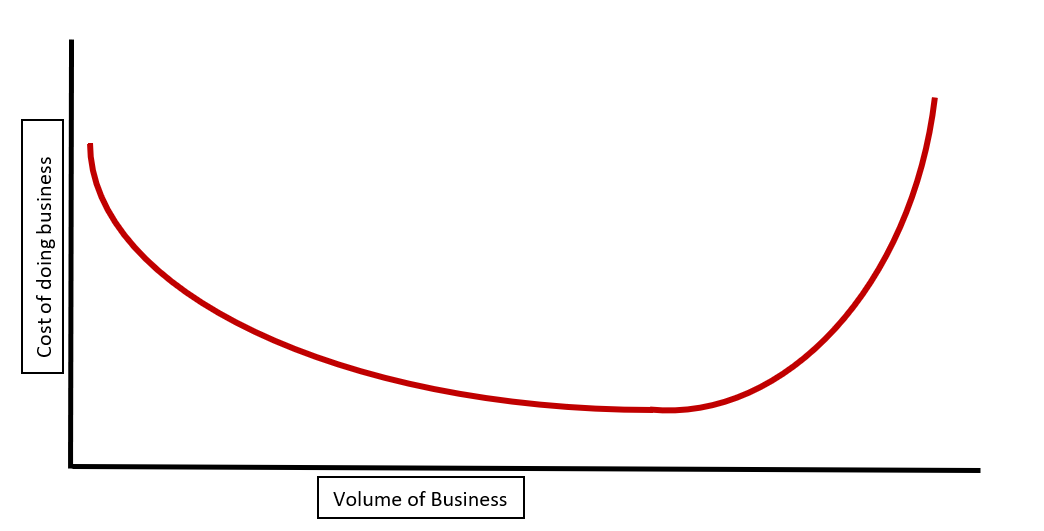

Nonetheless, in some corners of the real estate field, smaller still seems to be better. Brokerage, for example, benefits a bit from some aggregation, but is still very much a local hand-shake sort of business. Less-than-investment-grade investing (“B” and “C” properties) is still a localized business. Brownfield redevelopment and other niches are have proven difficult to aggregate. Indeed, in some niches of nearly every field of endeavor, the economies of scale equation looks more like this:

Beyond a certain point of inflection, the cost of doing business actually rises. Span of control is a difficult problem, particularly in complex fields. The more something can be commoditized, the further out that point of inflection is. However, there are limits to commoditization.

I was brought to think about this by the recent embarrassment of Zillow and their iBuying experiment. It was a very simple idea, really — local “flippers” were making tons of money buying dog properties in good locations, spending a few bucks on cosmetics, and selling into the rising price market. Indeed, my pet Pomeranian could have made money in residential real estate in the past 2 years. However, when markets start to flatten, some localized talent is needed. “You gotta know when to hold ’em, know when to fold ’em” as the old song goes. When markets shift, the economies of scale inflection point scales with it.

For those of you who weren’t keeping up with the Zillow news, the company set up a buying service a few years ago and started simply cutting a check on properties that their algorithm indicated could be flipped for a profit. I would argue that in normal markets, this is the sort of business that requires extensive localized knowledge. In rapidly changing markets, even more so. This isn’t a critique of mass appraisal models. Indeed, I’m a big fan of those, and they prove useful in many situations. However, the act of taking an individual property thru the “flip” process is complex and fraught with risks. A mass appraisal model can inform the participant, but can’t be a substitute for entrepreneurial effort.

Reportedly, Zillow had quite a few billions of dollars on the table, so this isn’t a small undertaking. Zillow is laying off about 1000 people — around 25% of their entire workforce. The investments were in about 25 or so secondary sunbelt cities, like Phoenix and Las Vegas. They’re said to be dumping about 18,000 residences, expecting to take a 5% to 7% loss on the transactions.

About 5.64 million homes sold in America in 2020, so 18,000 isn’t a real macro market mover. Of course, this is a pain for the 1,000 Zillow employees who are losing their jobs, and Zillow stock is down about 40% from the peak in late October. Conversely, the housing market is still pretty good and Zillow’s exit may create niches for local entrepreneurs. We’ll keep you posted.

As always, if you have any questions on these issues, please don’t hesitate to reach out. We look forward to hearing from you!

John A. Kilpatrick, Ph.D., MAI — John@greenfieldadvisors.com

Leave a comment