Archive for August 2021

Investing in Single Family Rental Housing

Last week, I had the very real pleasure of speaking to partners in several boutique law firms about real estate, and specifically about issues facing their clients who invest in single family rental housing. Note that I am not a critic of these investments — far from it, in fact. However, there has been an explosive growth in single family rental investing in the past few years, and particularly during the pandemic. The investment growth, creating a significant supply of such housing, has been matched with demand growth as rental householders move out of central business districts into the suburbs and into larger rental units providing more room for home-work, home-schooling, and extended family households. Nonetheless, as new investors move into this market, and as prices are bid up to record levels, an abundance of caution may be in order.

First, some of the numbers. There are about 140 million housing units in America. If the average value of each unit is $200,000, then this is a $28 TRILLION market. Hence, even small shifts at the margin have very large economic impacts.

For the last 50 years, somewhere between 63% and 70% of these housing units have been owner-occupied. The trend got very close to 70% during the pre-2008 bubble, but generally hovers around 65%, slightly higher in the South and Midwest, and slightly lower in the Northeast and on the West Coast. At the end of the 2nd quarter, 2021, the number stood at about 65.4% nationally, but that was sharply down from 67.9% just a year ago. While a 2.5% movement may not sound like much, that’s a shift of about $700 BILLION in housing from owner-occupied to tenant occupied (and thus, investor owned) in one year.

Of that big slice of the market that is tenant-occupied (and investor-owned) about 37% is in single family residential (“SFR”) homes. By the way, another 29.4% is in duplexes, tri-plexes, four-plexes, and small apartments with 9 or fewer units. Historically, this type of investment has been owned by individual investors or perhaps small partnerships, although that model is rapidly going by the wayside.

Both publicly traded REITs and private funds (including private REITs) are getting into the game big-time. Public REIT investing offers a high degree of liquidity, but sometimes with the trade-off of lower returns. Private REITs and funds promise higher returns (although don’t always deliver) but with almost no liquidity. Traditional rules of thumb suggest that a public REIT may aim for combined returns, both price-return and dividend income in the range of 7% over the long haul. Statistics from the National Association of Real Estate Investment Trusts bear this out. Private investors aim somewhat higher, and usually there is a trade-off between potential price gains and potential dividend returns.

That said, this year has been nothing short of amazing for OWNERS of SFR homes, although perhaps not for those who have been buying into this bull market. Case in point, last week, Bloomberg News reported that US SFR rents rose 7.5% year-over-year in June. The largest increases were in the Southwest, with Phoenix reporting an increase of 16.5% and Las Vegas showing 12.9%, year-over-year. Not surprisingly, investors have been flocking to funds that are in those markets. Just as an example — and there are others we could use — Invitation Homes (INVH), a publicly traded REIT, owns over 80,000 SFR homes, mostly in those hot sunbelt states. Enjoying a 96% occupancy, their stock price has risen over 40% just this year, driving their dividend yield down to 1.67%.

Not all is smooth sailing, though, and increases in rents don’t always lead to an increase in rent INCOME. Case in point, in the face of such great statistics, why not raise the dividend yield? Consider, however, pandemic-related collection issues, commonly referred to in the industry as “tenant chargebacks.” In a normal year, we would expect this number to be in the range of 1% – 2% for a well-run fund. However, another REIT we examined, American Homes 4 Rent (AMH) has also exhibited greater than 40% stock price appreciation this year, but has a dividend yield at 0.95%. Digging deeper, we find that AMH reports a 13.5% tenant chargeback. As bad as this is, after the pandemic-related eviction moratorium runs out, this may be a ticking time bomb for some funds.

Private funds – with almost no liquidity – promise substantial returns when they finally close out, usually in 3 – 7 years. Expectations in 12% and above range are not uncommon. We were recently shown one fund, which shall remain nameless, and buried deep in their offering circular was some nebulous language about a 3-year maturity and a 13+% expected annualized return. However, upon closer examination, we found that this will be the developer’s third fund, and the only one of those to reach maturity (this summer) ended up with a somewhat disappointing 5.17% annualized return. Nonetheless, this developer will almost assuredly raise $20 million in $25,000 increments from hungry individual investors.

This chase after the bull real estate market isn’t just limited to individual investors. Consider New Residential Corp, which until recently was a publicly traded REIT. They owned 14,600 homes in nine sunbelt states with a “carry value” of $1.873 Billion. They’ve been losing money for a while, and in the third quarter, 2020, managed to lose $63 million on revenues of $57 million. Their debt/equity ratio was about 85%, which is comparatively high for a REIT. The “book” equity was only $312 million. Nonetheless, a private fund bought New Residential, lock, stock, and barrel, for $2.4 Billion.

Don’t get me wrong — real estate over the long haul has been a strong contender for a well-balanced portfolio. If you had invested $1 in a SFR on January 1, 2000, by today you would have $2.46 with surprisingly little volatility. Even with the housing “bubble” and crash, your investment would never have been out-of-the-money. Plus, over the years, you would have enjoyed tax benefits and either a place to live or rental income. Compare that with investing that same dollar in the S&P 500. Today, you would be a bit richer — $2.85 — but your investment would have been a loser for most of the last 20 years. Indeed, you wouldn’t have been “in the money” until 2013, but for a short period in 2007. Further, the market volatility would make your head swim.

There is a very real growth in both the demand for and the supply of SFR rentals. Portfolio benefits can be quite good, but caution is the watchword for newbie investors diving into this market. Historic rules-of-thumb and trade-offs between current income and capital growth may be out-the-window for a while, and there will almost certainly be a settling out period after the COVID pandemic is over.

Note: Dr. Kilpatrick and/or Greenfield Advisors may, from time to time, have investments which are mentioned in this presentation. Nothing in this presentation should be construed as investment advice.

If I can answer any other questions, or be of any assistance on these matters, please let me know.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Share this:

REAL Estate and ESG Investments

ESG is an acronym for “Environment, Social, and Governance.” It is the current buzz-word in the industry for what was formerly called “green building”, although as you can tell from the title, it is so much more than that.

The US Green Building Council was formed in 1993 to “promote sustainability in the building and construction industry”. While it is active in many areas of real estate, it is perhaps best known for the LEED building certification. For quite a few years, the National Association of Real Estate Investment Trusts (NAREIT) awarded the “Leader in the Light Awards” to honor REITs that “demonstrated superior and sustained energy practices.” Back in 2015, I conducted a study about these awards and presented a paper at the annual meetings of the American Real Estate Society investigating whether or not there was any stock price bump (or other meaningful market reaction) associated with such an award. While I couldn’t find any statistically significant market reaction to the award itself, there was anecdotal evidence to suggest that such “green” behaviors were already capitalized in the stock price and the return generating process.

In recent years, the focus has shifted away from just “green” issues toward broader themes, including all of the ESG topics. Both large and small consulting firms (including Greenfield) are engaged in some or all of the ESG issues, including such key elements as dealing with catastrophic events, setting corporate goals for community development, and establishing adequate data protection.

Real estate firms of all stripes are increasingly considering ESG in their business models. There are enormous direct benefits up and down the real estate ladder. Local governments are now looking policies, commitments, and goals in some or all ESG areas as a precursor for permitting. ESG is a significant marketing tool, and customers are reacting positively to the ESG message. For example, Blackrock’s CEO, Larry Fink, announced at last year’s Morningstar Investment Conference that they planned to integrate ESG metrics into all of their portfolio by the end of 2020. This year, NAREIT reported that 98 of the top 100 REITs reported publicly on their ESG efforts.

By some reports, climate change has been a primary driver of ESG attention. Energy usage at the property level can be immediately reported and analyzed for potential cost savings. Noting that the incidence of climate events causing $1 Billion or more in property damage have quadrupled in recent years, it comes as no surprise that this has nearly everyone’s attention. Recent back-to-back environmental disasters in Texas have been cited as particularly concerning to investors.

S&G — social and governance — have worked their way into investment underwriting, and despite a surplus of liquidity in the market, investors want to know that S&G issues are being meaningfully addressed. This is particularly acute with public funds and public securities holdings. The Pension Real Estate Association (PREA) has instituted annual ESG Awards “[T]o recognize excellence in ESG programs within institutional investors in real estate.”

Many say that the pandemic has catalyzed ESG policy adoption, although the trend was clearly strong before the COVID outbreak. Nonetheless, it is now almost universally recognized that the ESG momentum will continue to grow. This doesn’t mean that universal adoption is imminent. Some firms still stand on the sidelines waiting for the metrics to come in — capital flows and returns being key touchstones. Transparency and benchmarking will be key elements to further adoption down the road.

As usual, if we can answer any questions on this topic, please do not hesitate to reach out.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Share this:

ACCRE Report, July, 2021

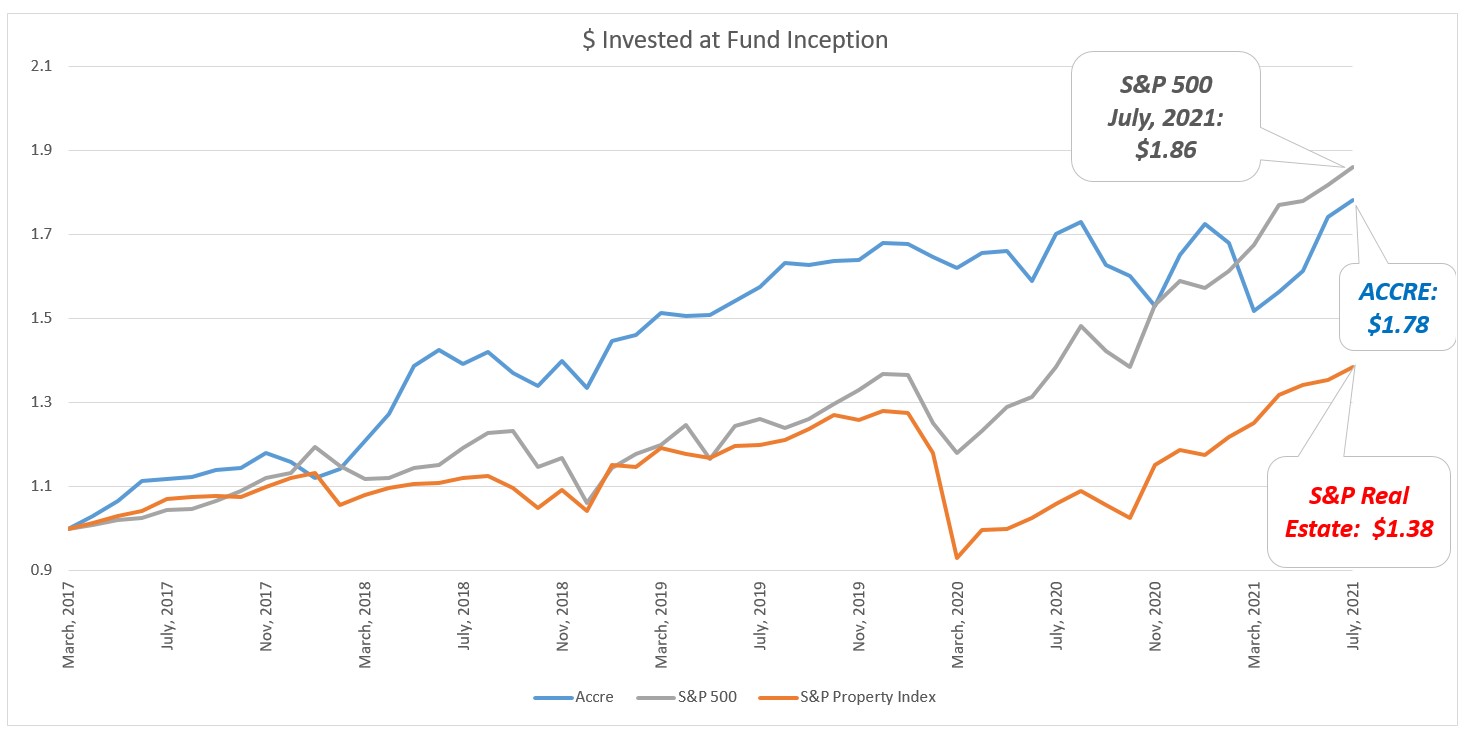

July was a “boringly good” month. I say that because ACCRE and other portfolio components all performed extremely well. ACCRE slightly outperformed the S&P (2.68% versus 2.27%) but neither of these can be sneezed at. The S&P Global Property Index had total returns of 2.36%, also a solid performance. I would note that the S&P broad market index has had 6 straight months of positive returns, and 17 positive months out of the past 24. As such, ACCRE is competing in rarefied territory.

Thus, a dollar invested in ACCRE at the inception (April 1, 2017) would be worth $1.78 today, for an average annual return of 14.36%.

| S&P 500 | |

| Average Daily Excess Returns | 0.0516% |

| Standard Deviation of Excess Returns | 1.2712% |

| Sharpe Ratio (Life of Fund) | 4.0604% |

| ACCRE Fund | |

| Average Daily Excess Returns | 0.0470% |

| Standard Deviation of Excess Returns | 1.1894% |

| Sharpe Ratio (Life of Fund) | 3.9508% |

| Correlation (Life of Fund) | 50.9401% |

| Monthly Correlation (July, 2021) | 12.0631% |

ACCRE continues a healthy overall correlation (life of the fund) with the S&P, but also continues a two-month run of surprisingly low monthly correlations. We suspect this has a bit to do with the volatility of both indices, but we’ll continue to monitor.

As always, if we can answer any questions about REITS or real estate in general, please reach out. We look forward to hearing from you.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com