Archive for November 2nd, 2020

ACCRE, October, 2020

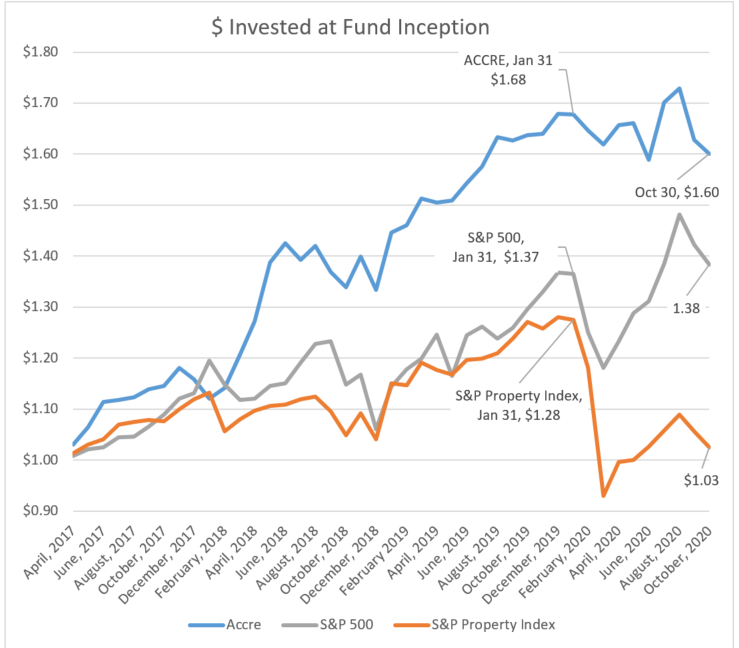

Let’s just start by acknowledging that October was a terrible month for investments in general, and particularly real estate. The Covid-related recession tsunami is catching up with impacted RE sectors, and much of this is slowly being capitalized into both the REIT market and the broader indices. Case in point — this morning, two major retail REITs (CBL and PREIT) which between them own 130 shopping centers, had to file for Chapter 11. This came as little surprise, since some of their largest tenants, including JC Penney, Tailored Brands, and Ascena Retail Group, have also filed for bankruptcy.

We feel very fortunate that ACCRE has continued to hold its value in the face of this wave. Our overall performance since January 31 (arguably, the end of the bull market) has been only slightly below the S&P 500 (which is now right back where it was 8 months ago) and is well above the overall S&P Property Index, which tanked in the spring and has had very real difficulty regaining its footing since then.

The Financial Times Stock Exchange (FTSE) tracks 159 equity REITs in conjunction with the National Association of Real Estate Investment Trusts (NAREIT). REITs are often bought for the inflation-hedged dividend yield, as as of the end of October, the average equity cash-on-cash yield was 3.98%, which of course compares well with corporate bonds. However, on a compound annual total return basis, the typical equity REIT has shown a total negative return of -16.25% for the year ending October 30. Peeling back the layers of the onion, we find that the actual returns have been all over the map. Not unexpectedly, lodging/resorts has been the worst major sector performer (-46.78%) followed by retail at -44.72%. However, even within retail, regional malls, as a sub-sector, have seen a -54.41% return.

That said, some sectors have done quite well. Data center are up 20.27% on the year, while infrastructure is up 11.95%, industrial up 8.28%, and self-storage is up 8.15%. Residential has suffered (-26.03% on the year) but within residential, single-family homes are almost breaking even (-3.42%).

By the way, mortgage REITs are suffering the same way they did in the 2008/10 debacle. At ACCRE, we avoid mortgage REITs, private REITs, and un-traded REITs.

Recent statistics suggest that as many as 44% of American households own REITs either directly or indirectly in their portfolios. Real estate is a nearly ubiquitous part of the global investment portfolio, and a well-curated REIT selection can add both diversification and positive returns to the portfolio. Drop us a line if we can help.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com