Archive for December 2020

Back rent problem — take 2

In my previous post, I talked about the accumulated “back rent” problem stemming from the COVID recession. It’s a growing problem, and one which the newly signed COVID relief bill only partially addresses. Here’s what we know today about rental assistance forthcoming.

I would stress at the onset that state and local agencies will be the conduits for this relief, as was done in the previous CARES Act. Notably, it took weeks or months for many of these agencies to spin-up the actual relief payments. Hopefully they have some lessons learned from earlier this year, but don’t expect relief to come in the next few days.

Relief payments must be used to fund the following:

- Rent and rental arrears

- Utilities and other home energy expenses, but current and in arrears

- Other pandemic-related housing expenses

Assistance may continue for up to 12 months, and in some circumstances for up to 15 months if situations warrant. Eligible tenant households must meet all of the following three criteria:

- An individual in the household has qualified for unemployment benefits or the household has experienced an income reduction, experienced significant pandemic-related costs, or can document other pandemic-related financial hardships. (Note: applicants must attest to this in writing.)

- One or more individuals in the household must demonstrate a risk of experiencing homelessness or other housing instability, such as a past-due utility or eviction notice or unsafe or unhealthy living conditions.

- The household income is less than or equal to 80% of the area median income, based either on total income for the year 2020 or confirmed monthly income at the time of the application.

Priorities will be given to households with income less than 50% of the area median and households where one or more persons have been unemployed for 90 days or more. Landlords may provide application assistance but will need to obtain the signature of the tenant, provide documentation of the application to the tenant for their records, and use any payments for current or past-due rent.

As noted, the conduit for all of this will be state and local government agencies and tribal units. Those agencies will be responsible for collecting and reporting certain documentation to the U.S. Treasury Department, including the number of eligible households receiving payments and average payments per household, the types of assistance provided, the acceptance rates, the average number of payments covered by the assistance, and the household income levels by median income category (e.g. — less than 30%, 30% to 50%, and 50% to 80%).

We’re all waiting to see how this pans out, and quite obviously this will not cure the problem. However, it is clearly a step in the right direction. Please stay in touch — we look forward to hearing from you all.

John A. Kilpatrick, Ph.D. — john@greenfieldadvisors.com

Share this:

How bad is the back rent problem?

It is axiomatic that landlords do NOT want vacant space, and coupled with eviction moratoriums there is a growing backlog of unpaid rent, particularly by small businesses and residential tenants. Anecdotally, the problem is widespread and growing, but just how big is it? Experts differ, but generally agree it is huge and portends a huge humanitarian problem in 2021.

One of the most quoted experts on the topic is Mark Zandi, chief economist at Moody’s. He estimates that 11.4 million renters owe an average of $6,000 in back rent. Add to that late fees on utilities and such, and we’re probably looking at a $70 Billion problem, more or less. Most of this has accrued since the CARES Act expired last summer.

Even back in September, the overdue rent bill had already reached an estimated $34 Billion, according to a study commissioned by the National Council of State Housing Agencies. Note that this problem is not just limited to renters — Since August, the FHA mortgage delinquencies have been setting new records, at 15.6% on September 30th, the highest rate since 1979. Note that the peak during the Great Recession was between 14% and 15%. The Mortgage Bankers Association is tracking forbearances among lenders, and estimated that 5.5% of mortgages, or 2.7 million, were in some sort of forbearance in November. The delinquency rate in September was 7.6%, and while this is down from 8% in April, it is dangerously close to the 10% peak seen in 2009/10. The Credit Union Trends report released in late November forecasted delinquencies to “broadly rise in the fourth quarter and charge-offs to rise in the first quarter” of 2021.

The economy is definitely bifurcated right now. The upper tier has seen the value of their stock portfolios grow by well over $1 Trillion this year, but as Zandi notes, the renter population is at the bottom tier of the economy. They’ve already borrowed as much as they can. Over the weekend, the President signed the COVID relief package, but while the eviction moratorium continues, back rents continue to accrue. One recent study suggested that at present, as many as 14 million rental households are in arrears, and this number will clearly get worse over the winter. Another, issued by the National Low Income Housing Coalition, put this number at 6.7 million. The Census Bureau’s latest Housing Pulse Survey (from November) indicated that 11.6 million people would not be able to pay their rent or mortgage payment in December. Whatever the final number, at some point, the piper will need to be paid.

Notably, the bill signed yesterday includes $25 Billion in emergency rental assistance. Exactly how this will be distributed, and how much of the rental backlog this will actually assuage, will be seen in the coming days. Notably, when the CARES Act included such assistance, it took some state housing finance agencies months to actually enable rental aid programs.

Again, anecdotally, landlords have shown very real forbearance in this area. I would note that the rental market, ranging from single family housing to large apartments, are generally ultimately owned by individual investors. At the lower end of the spectrum (rental houses, for example), individual investors usually directly own and manage these properties. At the upper end, REITs or Trusts may own the properties, but the rental income flows to investors or their retirement accounts. Further, rental income employs property managers, maintenance people, and a host of other service providers. In short, this is a problem that reverberates across many sectors of the economy.

Share this:

So what do we know about COVID relief?

I spoke with some folks “in the know” this morning, and the details are still unfolding. The real estate sector should pay very close attention to this, as so many aspects of the relief bill affect it.

First, what do we think we know? There are apparently 6 categories of aid in this package:

| Supplemental Employment Insurance | Weekly payments of $300 (half of what was provided in the original CARES Act) for up to 11 weeks |

| Direct Payments | One time payment of $600 for individuals making under $75,000 and for each dependent child (again, half of the CARES Act) |

| Small Business Relief | PPP loans of $284B (about $100B less than CARES) plus $15B specially allocated to theaters and live entertainment venues |

| Rental Assistance | $25 Billion, and the national moratorium on evictions extended until Jan 31 |

| Vaccine Assistance | $48 Billion for healthcare, and $20 Billion for vaccine distribution |

| Education | $82 Billion for local schools, colleges, & child care plus $13 Billion for supplemental nutrition programs |

It is axiomatic that the lowest wage earners, who have generally been hit the worst by this recession, are most likely to be renters. Further, a large portion of rental properties are owned by small real estate investors. Hence, there is a bit of a two-edged sword here, in that some parts of this may flow directly to those landlords who are often retirees or others dependent on rent collection. From a practical perspective, the eviction moratorium isn’t nearly as powerful as it seems, because so many landlords would rather keep a non-paying tenant in place than to go thru the cost of eviction only to have an empty property.

It’s far too early to even conjecture as to how much (or little) impact this will have. Many businesses kept their doors open only due to the CARES Act PPP loans, but all too many of those have now shuttered permanently. For example, CNN Business reported last week that 10,000 restaurants have closed for good in the past 3 months. Every one of those restaurants had a landlord who is now not getting paid. Back in September, YELP reported that 163,735 small businesses that they track had shut their doors, and that almost 98,000 of those were projected to be permanent closings. Of course, large chain bankruptcies and closures are well publicized.

One intriguing study from iPropertyManagement.com suggests that apartment and rental housing vacancies vary widely according to location — inner city versus suburbs. Apparently, major cities are seeing an uptick in apartment vacancies (Manhattan’s has tripled), but suburban vacancy rates are actually down, suggesting renters are fleeing congested cities. Indeed, non-metro area vacancy rates are also down.

By the way, this is usually the week I re-visit our REIT Fund-of-Funds, ACCRE LLC, and report on the S&P correlations and other diversification benchmarks. Going forward, I’m going to consolidate the two ACCRE reports into one at the beginning of each month. This mid-month blog post will now be just about economic and real estate issues.

This is also my last post (I think!) before the Christmas holiday. All of us at Greenfield hope you and yours are enjoying a safe holiday season. I know we’ve lost all too many friends and colleagues this year, and we look forward to getting COVID under control in the very near future. Best wishes,

John A. Kilpatrick, Ph.D. — john@greenfieldadvisors.com

Share this:

Trophy Property and the Pandemic

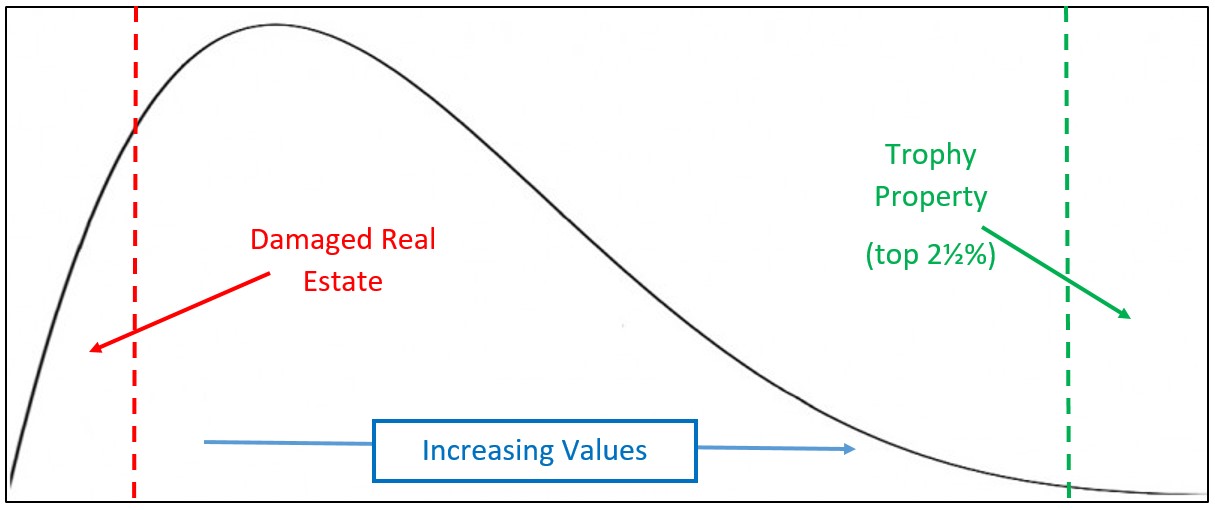

I spend a significant amount of my time at two somewhat opposite ends of the real estate spectrum – “damaged” property (particularly environmentally damaged, such as brownfields) and “trophy” property. Neither of these sectors behave like “normal” real estate even in “normal” times. Damaged property may eventually be remediated, converted, or in some way improved into the normal market. Ironically, demand for some kinds of damaged property, such as foreclosures, may actually improve during recessions or other “normal” market disruptions.

Trophy property is typically any property in the top 2.5% of its subclass. The market for such properties transcends normal markets for that subclass. Consider all of the office buildings in a given city — even New York or London. Investments in Class C and B offices may appeal to local buyers, while Class A properties will typically be marketed to trusts, REITs, pension plans, or the like. However, at the very top — the “named” properties which really anchor the city as a whole — the investment market may be entities or individuals for whom the trophy investment will provide halo effects or collectable effects for the rest of the portfolio. Normal metrics — income or cash/on/cash rates of return and such — may not apply to trophy investments. Much like a fine painting or other object d’art, an investor may want to own a trophy property simply for the sake of owning it. Of course, it doesn’t hurt that over long periods of time, trophy real estate has a great history of maintaining and improving value. It doesn’t hurt that trophy property investors often have very long time horizons, perhaps even multi-generational.

So, how is trophy property faring during this pandemic-induced recession? As with any good analysis, it may be too early to tell, but some anecdotal info coming our way suggests that trophy investors look at this recession as a real opportunity to pick some low-hanging fruit. One case in point was the acquisition of the Viceroy L’Ermitage Beverly Hills Hotel in October by EOS Investors. Admittedly, this property had a “damaged” component — the property had been taken over by the U.S. Government as a result of prosecution of an international money laundering case. Further, hotels in general remain strained, with many transactions falling into the “damage” category. However, EOS ended up paying $100 million for the 116-room trophy property, nearly $1 million per room, a figure that bears almost no connection to the realities of the hospitality market today.

At the other corner of the country, Manhattan trophy residences recorded one of their best weeks of the year in late October, albeit with a fairly large inventory of top-tier properties coming on the market. As an example, a 30,000 square foot, 5-story home on West 11th Street in Greenwich Village sold this month for $45 million. Originally listed for $49.5 million in January, 2019, this was the second highest price residential sale in New York City this year, and the highest since the pandemic began. Another New York City trophy residence sale in late October was a Perry Street (Tribeca) 5-bedroom duplex, with a private pool, for $20 million. According to one source, the average sale-price-to-list-price discount for Manhattan trophy residences stands at 11%, and the average time on the market in this sector is about 2 years. The last week of October showed 5 New York City contracts at $10 million or more.

Finally, in the middle of the continent, trophy ranches continue to sell to investors looking for recreation, retirement, or just pure collection purposes. Recent top-tier sales include the Pole Mountain Ranch in Wyoming (2,300 acres, 8,000 square foot main home, $8 million), a vacant pond-side lot at the Elk Creek Ranch in Colorado ($1.1 million for 2,850 vacant acres), and the Winding River Ranch in Wyoming (376 acres, 1.5 miles of Platt River frontage, custom built 5-bedroom lodge, for $2.2 million).

In short, there is some disruption right now in the trophy property market, as many properties seem to be coming on the market and inventories are strong. However, buyers with cash and/or resources are definitely in the market, and are looking to cherry-pick trophies that come available.

Share this:

2021?

This week, I sat thru a great presentation (virtual, of course) by John Chang, the Director of Research at Marcus and Millichap. Like any research report, it has to be taken in the context of all of the other information out there. However, I get a deluge of this stuff, and I thought Chang’s work on the subject was quite good.

He starts out by noting what we all pretty much know — four real estate subsectors were hit the hardest this year: Hotels, Senior Housing, Sit-Down Restaurants, and Experiential Retail. Three sub-sectors actually did quite well: Industrial (and I would note data-centers in particular), Self-Storage, and “Necessity” retail. Later in his presentation, he points out that Offices and Housing (I would note with the exception of student housing) also held onto some core value.

Chang comments — and I concur — that never in our memories have we seen a real estate recession that was so geographically broad and across so many sub-sectors. For example, the 2008/10 debacle was primarily focused on housing and the mortgage backed securities market, and while the entire real estate securities market declined, it was more related to correlations with the broader market than with underlying real estate fundamentals. Today, however, we’re seeing some very real systemic changes throughout the real estate economy.

So, what does 2021 look like? The first half of the year is, at best, a continuation of where we are right now. Small businesses, and the real estate that supports those businesses, are hanging on by fingernails. Chang suggests that a recovery in the 2nd half of 2021 depends on three variables:

- The size and quality of the next recovery package. In his opinion — and I agree — the mid-sized package would be in the range of $1.5 Trillion, and would include expanded unemployment, PPP expansion for small businesses, housing assistance, assistance for state and local governments, public health assistance, and provisions for vaccine distribution. If the next stimulus package is smaller than this, then business and real estate in the U.S. will face considerable headwinds.

- “How long” will a medical solution require? If a medical solution can be rolled out by mid-2021, then a 2nd half recovery may be in the offing. However, time is not our friend, and there will be continued attrition until a solution is in place.

- “How effective” will a medical solution be? There will undoubtedly be setbacks. How well will we overcome the medical road blocks along the way?

If all of this come to fruition in a timely fashion, then a recovery may come along slowly in the 2nd half. The “down” sectors, particularly tourism related and in regular tourist destinations like Orlando and Las Vegas, may see a slow recovery start up by the end of 2021. Other down sectors may see some light at the end of the tunnel. Conversely, sectors which enjoyed the greatest benefit during Covid (data centers, for example) may lag the market. Offices and housing should continue to hold their own.

Again, I don’t necessarily agree with everything Mr. Chang said, but his opinions are some of the best I’ve seen, and I wanted to share this with you all. If you have any questions, please don’t hesitate to reach out.

John A. Kilpatrick, Ph.D. — john@greenfieldadvisors.com

Share this:

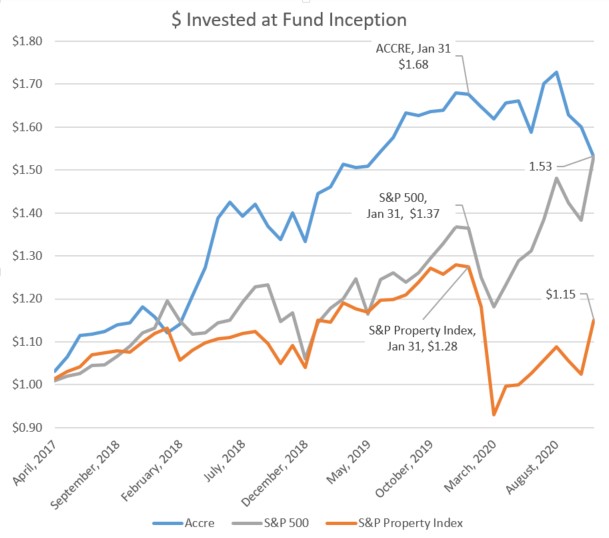

ACCRE, November, 2020

The chart says it all — the past 3 months have been the worst stretch in the history of ACCRE. Ironically, it has been a very good period for the S&P and for REITs and real estate as a whole. Why, you ask? Simply put, we had positions adverse to student housing and other holdings that were laggards due to COVID, but the good news of November — which is good news for us all — caught us by surprise. Indeed, all of our losses happened in just a few days mid-month.

It is axiomatic not to be too aggressive in clawing back losses. We made a small portfolio adjustment, and December is already looking positive. We’ll probably take on some other positions in the coming days. Note that one of our principal strategies is to stay sane with our portfolio — historically, we’ve only beaten the S&P 50% of the time, on a month-to-month basis. However, we try to stay away from big market moves, enjoying the upside without suffering big bear market moves.

As always, our subscribers receive same-day notification of any portfolio changes. Best wishes to you all — we hope you had a great Thanksgiving, and you’re all looking forward to a great holiday season.