Archive for November 2020

ACCRE Mid-Month Report

It’s been a mixed-bag for REITs this month. While many sectors continue to lag, short positions can be dangerous. The market is hungry for good news, and leaps at anything tossed in the water. Case in point, we saw one REIT with terrible earnings projections, but the market price rebounded when Funds from Operations (FFO) came in “less bad” than previously forecasted. Another REIT has a spread of analysts targets of over 100% from bottom to top, proving that optimism has a home in the real estate sector.

This month, I’m going to provide both LAST month’s stats on ACCRE as well as this month, just to show what a difference a month makes:

| September, 2020 | October 2020 | |

| S&P 500 | ||

| Average Daily Excess Return | 0.0327% | 0.0290% |

| Standard Deviation | 1.3451% | 1.3429% |

| Sharpe Ratio | 2.4315% | 2.1576% |

| ACCRE Fund | ||

| Average Daily Excess Return | 0.0455% | 0.0426% |

| Standard Deviation | 1.1540% | 1.1520% |

| Sharpe Ratio | 3.9436% | 3.6984% |

| Correlation (overall) | 56.4666% | 55.8996% |

| Correlation (monthly) | 73.4120% | 57.0514% |

ACCRE continues to out perform the S&P, both on an unadjusted (Average Daily Excess Returns) and a risk-adjusted (Sharpe Ratio) basis, the correlation between ACCRE and the S&P really whip-sawed in October. In the previous month, we had a very tight correlation (73%) which is actually higher than we want it. A correlation in the 50’s serves our two-pronged goal of outperforming the benchmarks in the long run and providing diversification for a mixed portfolio.

Our private newsletter subscribers received some trade alerts today, and there will probably be more soon. This market has a great deal of volatility, as well as election-year and end-of-year roiling. We avoid run-and-gun trading (REITs really don’t day-trade well!) but the market we see right now requires some close inspection.

As always, if you have any questions or comments, please let me know.

John A. Kilpatrick, Ph.D. — john@greenfieldadvisors.com

Share this:

OK, First the Good News…

The stock market revived quite nicely this month, with the Dow up about 12.5% in the first 11 trading days, although I’ll admit that real estate in general (and ACCRE, our in-house fund) had a couple of tough weeks. Why, you ask? I’m getting to that.

Now for the tough news. Fed Chair Jerome Powell today, speaking at the European Central Bank Forum, noted that “We’re covering, but to a different economy.” In short, the economy as we knew it is probably a “thing of the past.” We’ve suspected this for some time. In many ways, both macro and micro, the economy has shifted out from under us. Some examples, taken just from my personal experience, in no particular order…

- Technology has taken the place of in-person meetings. I probably attend more meetings per week now than I did a year ago, but they’re all on zoom or such. I have three scheduled for today, and that’s not unusual. The good news — my travel time, finding a parking space, calling for an Uber, etc., are way down. The bad news — the folks who drive those Ubers, the servers and cleaning staff who work in conference centers, the folks at Starbucks who get me my coffee for the drive, indeed the guy at Brooks Brothers who sells me neck-ties, are all out of work.

- Lack of in-person means dramatically less demand for hotel space. In an average month pre-Covid, I’d take two business trips with anywhere from 2 to 5 nights in a hotel. Now? None of the above. No need for office space, hotel meeting rooms, airplanes, etc.

- Ditto restaurants. I can’t remember the last time I darkened the door of a sit-down establishment.

The lowest paid workers, those in jobs requiring face-to-face contact, are shouldering most of this burden. The recovery, such as it is, can be decidedly described as “K” shaped, with some parts of the economy (those heavily invested in the stock market) doing very well, while others are running out of oxygen.

Not to belabor the point but this all has some very real implications for real estate. If Mr. Powell is correct — and I believe he is — then the tough sledding we’ve seen thus far in the property market is bound to get worse in 2021. The S&P property index, measured in terms of total return, is down 7% for 2020. Now, given how well it’s performed over the past 10 years, that’s not a bad pull-back. However, Mr. Powell suggests we may see ourselves oversupplied with property next year, particularly in categories where workers meet customers on a face-to-face basis. While the market has already discounted a lot of this, such as in REIT prices, the workout problems will be immense.

As always, I enjoy hearing from you. Please reach out if you have any comments or questions.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Share this:

The Election and Real Estate Investments

As of this writing (near the end of the business day on Monday) the Dow Jones Industrial Average is up 2.95% on the day, and has risen about 8.3% in the past 5 trading days. The broader S&P is up about 7.3%, and the NASDAQ is curiously down on the day but still up about 7% since last Monday. This morning, the bond market was up, consistent with expectations of lower interest rates. While real estate is only peripherally impacted by the securities markets, these liquid markets give some insight into investor sentiments in the wake of the election outcome.

As of today, it appears Joe Biden will be the 46th president, the Senate will still be in republican hands (although slightly less so) and the democrats will continue to control the house. This implies two very significant things for governance in the coming four years:

- The Biden Administration will need to govern much closer to the center than if they had a democratic-controlled Senate; and

- There will be considerably more stability in White House relations with capitol hill.

Clearly, the thousand pound gorilla is Covid, and any restoration of the economy to pre-pandemic state hinges on that. Wall Street is already discounting a small but very real stimulus package which should juice the GDP a bit — not as much as the first one, but something. What does all this imply for real estate?

Residential Investment

The homebuyer market and the rental investment market have done well this year despite the recession. Low interest rates have fed home buying, and the desire for social distancing has provided some marginal preference for single family rentals as opposed to apartments. Indeed, the apartment REITs are generally down on the year (there are exceptions) with particular problems in the student housing and eldercare sectors. However, built-to-rent REITs are doing fine.

The Biden administration is hoping to provide support for first time homebuyers (a group that the homebuilding community says is in short supply today) with a $15,000 tax credit. Biden would also propose some sort of tax credits for renters and increase Section 8 vouchers. We suspect this will be met with widespread support.

However, Biden has also proposed some sort of rent and mortgage forgiveness. This may have some struggles — in many cases, rental property is owned by small to medium sized investors, and the trickle-down impact on real estate service providers, who are already stretched thanks to foreclosure and eviction moratoriums, would be difficult. This would probably face head-winds on capitol hill.

Commercial Investment

The FTSI/NAREIT index of REITs was up 4.23% last week. Note that the index is down 15.61% for the year-to-date. Obviously, there are some gems in there — our ACCRE index was up about 2.4% last week but down about 2% on the year.

Every category of REIT showed positive movement last week with the exception of self-storage and regional malls. The big winners were residential, up 6.31% and industrial up 5.49%. Even lodging/hospitality, which has had an abysmal year, was up 2.97% on the week. Mortgage REITs, which have also had a terrible year, were also up marginally on the week.

This suggests broad optimism going into 2021, although it remains to be seen how all of this will play out. The best estimates we’ve seen thus far suggest three to four years for the worst-hit sectors to revive to pre-Covid levels after some sort of containment or vaccine is effective. That said, much of the worst is probably already captured in real estate prices, and absent some further or unexpected negative events, we may see some slow progress back to normalcy in the real estate markets.

As always, if you have any questions about this, please reach out! Best wishes, and stay safe!

John A. Kilpatrick, Ph.D. — john@greenfieldadvisors.com

Share this:

ACCRE, October, 2020

Let’s just start by acknowledging that October was a terrible month for investments in general, and particularly real estate. The Covid-related recession tsunami is catching up with impacted RE sectors, and much of this is slowly being capitalized into both the REIT market and the broader indices. Case in point — this morning, two major retail REITs (CBL and PREIT) which between them own 130 shopping centers, had to file for Chapter 11. This came as little surprise, since some of their largest tenants, including JC Penney, Tailored Brands, and Ascena Retail Group, have also filed for bankruptcy.

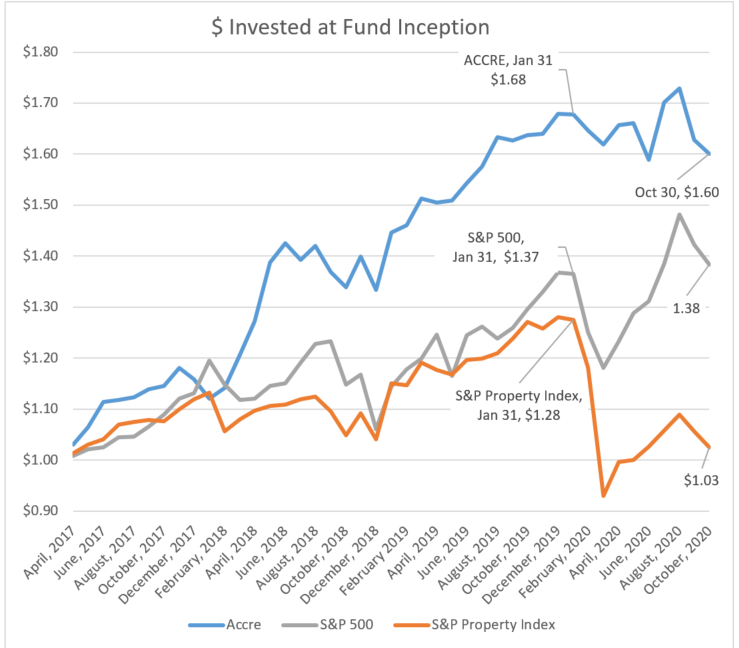

We feel very fortunate that ACCRE has continued to hold its value in the face of this wave. Our overall performance since January 31 (arguably, the end of the bull market) has been only slightly below the S&P 500 (which is now right back where it was 8 months ago) and is well above the overall S&P Property Index, which tanked in the spring and has had very real difficulty regaining its footing since then.

The Financial Times Stock Exchange (FTSE) tracks 159 equity REITs in conjunction with the National Association of Real Estate Investment Trusts (NAREIT). REITs are often bought for the inflation-hedged dividend yield, as as of the end of October, the average equity cash-on-cash yield was 3.98%, which of course compares well with corporate bonds. However, on a compound annual total return basis, the typical equity REIT has shown a total negative return of -16.25% for the year ending October 30. Peeling back the layers of the onion, we find that the actual returns have been all over the map. Not unexpectedly, lodging/resorts has been the worst major sector performer (-46.78%) followed by retail at -44.72%. However, even within retail, regional malls, as a sub-sector, have seen a -54.41% return.

That said, some sectors have done quite well. Data center are up 20.27% on the year, while infrastructure is up 11.95%, industrial up 8.28%, and self-storage is up 8.15%. Residential has suffered (-26.03% on the year) but within residential, single-family homes are almost breaking even (-3.42%).

By the way, mortgage REITs are suffering the same way they did in the 2008/10 debacle. At ACCRE, we avoid mortgage REITs, private REITs, and un-traded REITs.

Recent statistics suggest that as many as 44% of American households own REITs either directly or indirectly in their portfolios. Real estate is a nearly ubiquitous part of the global investment portfolio, and a well-curated REIT selection can add both diversification and positive returns to the portfolio. Drop us a line if we can help.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com