Archive for September 2020

Seven Biggest Real Estate Mistakes — Part 7

When I first published Real Estate Valuation and Strategy, one of our marketing plans was a series of small-group talks, mainly for clients of bank wealth management advisors. As I noted in the book — indeed, it’s one of the running themes of the book — most wealthy families, and those who want to become wealthy, either directly or indirectly (through business investments) have substantial real estate holdings. Unfortunately, investment advisors rarely have the tools or techniques to aid in managing that portion of the portfolio or integrating it into the rest of the portfolio. Nor do they want to — it’s just not part of what they do. That’s my job.

Nearly 90% of all millionaires became so through owning real estate — Andrew Carnegie

So, my “seven biggest mistakes” was just one of the planned themes for nice cocktail hour conversations with folks who need some guidance in starting, managing, or optimizing their real estate investments. Sadly, Covid-19 got in the way, so now I have a nice series of blog posts.

Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world. — Franklin Roosevelt

Mistake #7 — Not having a strategy

Wow, this sounds so simple. Time and time again, though, I see folks who don’t know how to get started in real estate investing, who have made terrific mistakes with their investments, or who don’t know how to get out of an investment rut. Regularly, these investments turn out to have been made opportunistically, out of emotion, or often as adjuncts to business acquisitions. This latter category is one of my favorites — a business gets sold, but the original investors keep the real estate. Suddenly, the real estate has no value absent the business, and the investors find that a disproportionate chunk of what used to be their wealth is tied up in something the don’t really know what to do with.

Buying real estate is not only the best way, the quickest way, the safest way, but the only way to become wealthy. — Marshall Field

One investor I met decided to dabble in rental property in his post-retirement years. (I say “one” but this story has been replicated time and time again.) Now, “dabbling in rental property” can be a good thing. However, what is your strategy for this? Do you want capital preservation? capital gains? Pure income? A hobby to keep yourself busy? What this investor ended up with was a smorgasbord of disparate properties, none of which really tied into each other. Every time he had to make a decision about one or the other property, it was like re-inventing the wheel. Eventually, he got sick and tired of the mess, and dumped the entire portfolio at fire-sale prices. (That, by the way, is how I met him!)

Landlords grow rich in their sleep. — John Stuart Mill

I knew one lady who owned a profitable business in a growing part of town. She saw that rents were going up steadily, year after year, and so decided to buy the building in which her business was located as a hedge against such rent increases. That was such an immediately good idea that she started buying surrounding buildings and enjoyed both the rent income as well as the capital appreciation. Since she was located in that part of town, she could carefully monitor the local economics, and a couple of decades later, when she saw the market turning, she was shrewd enough to roll out of these investments near the top of that market.

The major fortunes made in America have been made in real estate. — John D. Rockefeller

The specifics of a given strategy have to be tailored to the investor. Nonetheless, there are some key, crucial questions every investor at every stage of their investing life should ask:

- What’s your “end game”? Where do I want to end up with this? Just saying “rich” isn’t enough. You should have a fairly specific set of goals which may include ongoing income thru retirement, capital preservation or gains (to sell and re-invest at a later date), passing on a portfolio via a trust to your heirs, supporting a family-owned business, or perhaps just pure recreation. The list of possibilities goes on, but if you can’t write these goals down, you can’t manage them.

- How much do you know about real estate? The corollary to this is, how well advised are you? I can recommend a couple of great books (well, one in particular…) but seriously, this is an area in which specialized knowledge is more than just a bit helpful. By the way, good, solid research goes hand in hand with this.

- How active do you want to be? I’ll give you a hint — there can be some very real tax advantages here, if you’re careful. This is a discussion you and your tax advisors should have sooner rather than later. On the other hand, successful people, at the peaks of their careers, often have little or no time to devote to active management. This is a critical decision you need to make early in your investment strategy. Note that real estate can be MUCH more time consuming than a mutual fund, but considerably more profitable!

- Are there synergies between your real estate investments and your business?

- Conversely, does real estate help you diversify a portfolio that is heavily weighted toward your business assets?

- Timing… timing… timing…

- And yes (as trite as it is…) location… location… location…

Look at market fluctuations as your friend rather than your enemy; profit from folly rather than participate in it. — Warren Buffett

Successful real estate investing requires a very long-run. Whenever the market is hot, the televisions are replete with “fix and flip” shows. In the Seattle market, where I spend much of my time, I’ve occasionally gone to real estate auctions at the courthouse. At one time, you could easily spot the “Tech Millionaires” who had watched too many of those shows, and suddenly considered themselves to be real estate “flip” experts. They’d buy some dog of a property, head down to the lumber store, figure out which end of a hammer should hit the nails, and spend the next 27 weekends learning to be flippers. After selling, some of these math wizzes would divide their profit total by the number of hours they’d spent hitting their thumbs with the afore-mentioned hammers, and figure out that they’d been working for minimum wage. Sadly, of course, there were plenty of real estate strategies that would have left them with plenty of time for golf and tennis, plus actual long-term-capital gains.

Before you start trying to work out which direction the property market is headed, you should be aware that there are markets within markets. — Paul Clitheroe

So, where does that leave us? Consider your long-term end game, develop a strategy that fits you and your situation, and stick to that strategy. Avoid fads, don’t get trapped in schemes, and be sure that your real estate strategy is congruent with the rest of your investment strategies.

Now, before I go, here is a link to the other six articles. I hope you enjoy!

Mistake #6 — Getting Emotionally Involved

Mistake #5 — Right Property, Wrong Location

Mistake #4 — Trying to Catch a Falling Knife

Mistake #3 — Not Realizing You Own Real Estate

Mistake #1 — Misuse of Leverage

Stay safe everyone, and I’ll see you again next week!

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Share this:

ACCRE Mid-Month Report, September, 2020

The mid-month report always deals with diversification and the Sharpe Ratio (the risk-adjusted abnormal returns). Every month, month after month, we exceed the S&P and show solid diversification. August was no exception.

However, we talk about diversification as a given, without ever really justifying why it’s a good thing. Indeed, when we teach investments in college (and I just finished team-teaching investments at WSU in the Spring Semester), we accept that everyone buys into diversification as a predicate to discussing the topic.

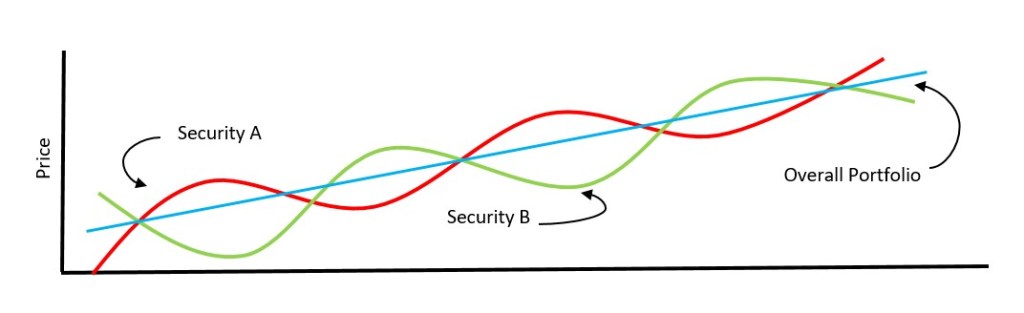

A diversified portfolio allocates investments in a way that reduces exposure to the volatility of any one asset. However, by itself, that’s not enough. The goal is to have a portfolio with less variance than the weighted average of all of the variances of the constituents, and in fact a well-diversified portfolio should have less overall variance than even the lowest individual security in the portfolio. In the figure following, assume you own just one asset, “Security A”. Its general trend over time is upward, but at any given point in time it may actually have declined in value, by cycling around the trend line. Now you add “Security B” to the portfolio. It is nearly perfectly counter-cyclical to A, and so the overall price trend is still solidly upward but with almost no volatility.

Of course, in a perfect world, such absolute diversifications doesn’t exist. However, as we’ve shown, ACCRE does a great job at attenuating a typical securities fund (i.e. — an index of the S&P 500), without giving up liquidity.

Now, on to ACCRE. It was another solid month for both ACCRE and the S&P, as demonstrated below:

| S&P 500: | |

| Average Daily Excess Return | 0.0379% |

| Standard Deviation | 1.3401% |

| Sharpe Ratio | 2.8271% |

| ACCRE Fund: | |

| Average Daily Excess Return | 0.0532% |

| Standard Deviation | 1.1379% |

| Sharpe Ratio | 4.6796% |

| Correlation (overall) | 55.8098% |

| Correlation (monthly) | 51.6244% |

Note that ACCRE has a better Sharpe ratio on two counts. First, the absolute value of the average daily returns is higher. Second, ACCRE has a substantially lower level of volatility, measured by the standard deviation over time. Finally, while pointed in the same direction as the S&P (positive correlation), the correlation is well less than 100%, showing a high degree of attenuation in the portfolio.

Well, that’s about it for this month. Stay safe, and we hope to see you all again soon.

John A. Kilpatrick, Ph.D., john@greenfieldadvisors.com

Share this:

Stigma revisited, yet again…

In 2018, I presented a paper at the American Real Estate Society titled “Stigma Revisited, Again…” It was a play on a seminal piece published by Peter Patchin in the Appraisal Journal some 30 years ago about environmental stigma and real estate value implications. Much was written on this topic over the ensuing decades, and I thought it was time to perhaps bring the literature up to date. As it happens, I and some fellow researchers found that the breadth and depth of the literature is too broad for just one paper. Instead, I’m aiming for a series of essays I’ll collect in a new book in early 2021.

In the meantime, it’s helpful to take a very brief glance at where we stand today. Fundamentally, stigma is the label we put on the loss in market value of an impaired property over and above any cost to remediate. My former business partner, Dr. Bill Mundy, is credited with introducing the term stigma into the appraisal lexicon with “Stigma and Value”, also published in the Appraisal Journal, in 1992. The scholarship in this field has been robust, with intertwined writings on the fundamental psycology of stigma, legal implications, methods, and valuation standards.

Stigma can arise from a property being directly contaminated, contaminated and then remediated, being adjacent to a contaminated (or remediated) brownfield, or even being proximate (that is, in the same neighborhood) as such a property. Kevin Haniger of the USEPA, Lala Ma of the U. Kentucky, and , and Christopher Timmons of Duke, writing in the Journal of the Association of Environmental and Resource Economists in 2016, documented the impact that a brownfield can have on residences within 5 kilometers of a brownfield, in the context of how remediation of that brownfield can impact the values of those surrounding houses. Zie Zhuang of Michigan State, along with a host of co-authors, wrote a piece in the American Behavioral Scientist, also in 2016, acknowledging that the behaviors of market participants, when faced with a contamination problem, were frequently at odds with the facts and even their understanding of the facts. Indeed, this is consistent with a stream of behavioral finance literature calling into question the rational expectations model.

Courts generally understand how stigma works. For example, In Re Bilmar Team Cleaners (Sup Ct of Vermont, 2015 WL 1186157) the Court acknowledged that a property could be stigmatized to the extent of future estimated remediation and other costs. In Harley-Davidson Motor Co. V. Springettsbury Township (Sup Ct of Penn, 2015 WL 5691056), the Court acknowledged that potential for future environmental claims constituted a stigma impact on the property’s value.

I’ll keep you posted as this next book progresses. Wish me luck!

Share this:

ACCRE LLC, August, 2020

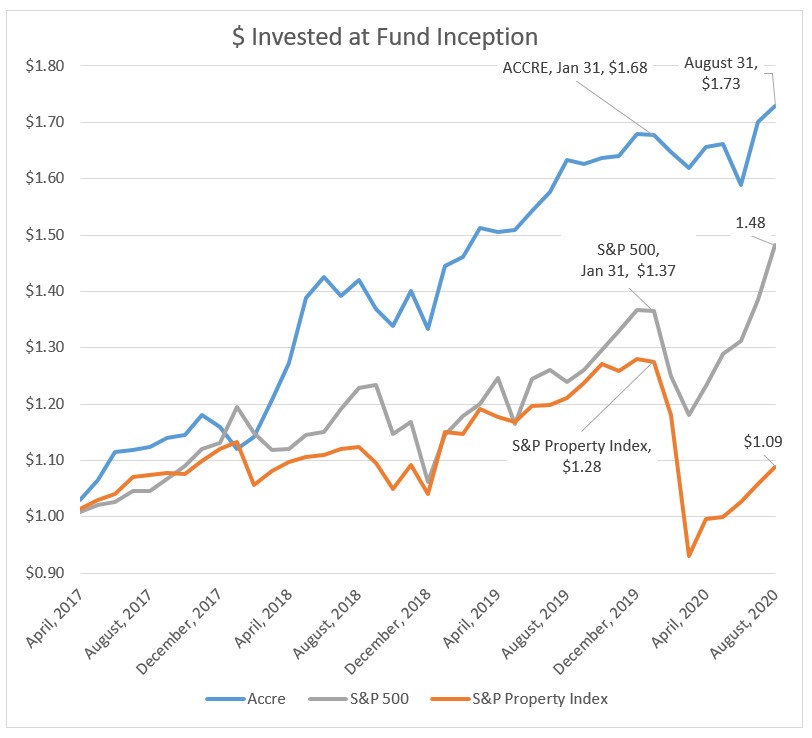

A well curated real estate fund should enjoy both above-average returns AND some attenuation of the risk in a securities portfolio. As noted a couple of weeks ago, ACCRE has about a 56% correlation with the S&P, which means that when the rest of the market is charging ahead, we’re tagging along, albeit at a slower pace. However, when the rest of the market falls out of bed, we don’t do so badly.

Case in point was the month of August, contrasted with the first few days of September. August was a gang-busters month for the S&P, and real estate in general did OK as well. ACCRE overall returns continue to be well above the S&P, but it is a horse race! A dollar invested in ACCRE at the inception (April 1, 2017) would be worth $1.73 on August 31, compared to that same dollar in the S&P only worth $1.48. Of course, the overall S&P Real Estate index fell apart after the onset of the recession, and is only partially back in the black today.

All that said, as every investor knows, this week has been painful for the broader market, with the S&P down about 4% since Wednesday’s close (as of this writing, mid-day Friday). ACCRE is also down, but only by about half as much. We’re still fully invested, but of course watching our positions carefully.

I would note that our strategy has been selective both on a macro and micro level. We’re looking for real estate sectors which we believe will do well in this economy, then within those sectors, we look for both the best and worst players. Yes, this is a fundamentalist strategy, but we also pay close attention to what the market is telling us. After all, REITs tend to be a sophisticated investment, and we gain a lot of insight by seeing how other investors interpret the tea leaves.

Best wishes to you all! As always, if you have any questions on real estate finance, economics, valuation, and such, please do not hesitate to drop me a line.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com