Archive for August 2020

Hospitality and Covid 19

Probably no real estate sector has been hit as hard as hospitality, which of course includes restaurants, hotels, and the whole travel and leisure field. It’s a big field, employing lots of folks, and occupying lots of space.

McKinsey and Company, a widely respected research and consulting firm, released a study in June on U.S. hotels. It’s already a bit dated, but contains some great insights into how business leaders are thinking about this, and the ramifications of various public policy decisions.

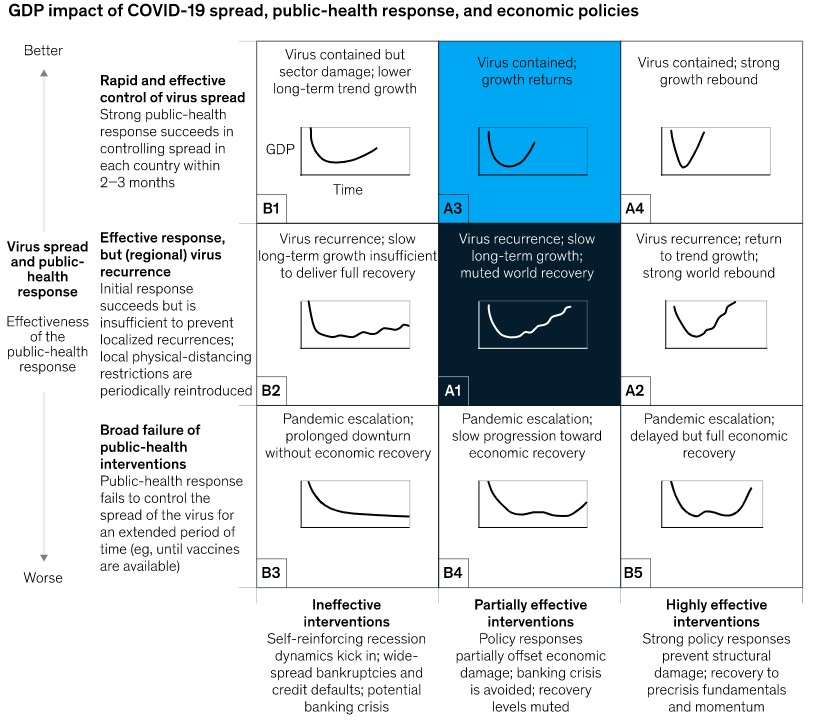

First, McKinsey constructed a common 3 X 3 matrix of low, medium, and high outcomes for Covid containment and economic impacts.

They then surveyed a large number of business leaders — which one of these do you think will be the most likely outcome? In their April survey, 31% opted for A1 (right in the middle) while 16% opted for A2 (broad success on the epidemiological front, but muted outcomes on the economics). By May, these percentages had risen to 36% and 17%, respectively. Thus, a small majority of business leaders do not believe in an economic miracle. By the way, fully 31% in May opted for B1, B2, and B3 combined, with ineffective economic results. Only 10% of respondents thought that economic interventions would be “highly effective”.

So, what does all this mean for the hotel industry? McKinsey gamed this out, and under both Scenario A1 and A3, hotel revenues are down to between 35% and 45% of 2019’s totals. They then tracked likely outcomes out to 2023, and their model suggests that under A1, hotel revenues are still down by 20% compared to 2019. Scenario A3 is much better, with a near full recovery in 2022, and revenues actually up by 2% in 2023.

Scenario A3 assumed that travel restrictions were lifted for most U.S. domestic travel by June of this year, which was only partially true, and lifted for some international travel by July, which is a mixed bag. A3 assumes that after travel restrictions are fully lifted, buying behavior will be based on economic rather than health related factors, and that there is an effective, scaled-up treatment or vaccination. Of course, neither of these has come true yet. However, there is some hope that the outcomes they had looked for in mid-year may come to pass in early 2021, and so these forecasts can be shoved down the road 6 months to a year.

By the way, not all hotels are affected the same. Luxury properties and “upper upscale” saw revenue per available room (RevPAR) fall by nearly 90% by mid-2020, and these sectors will probably only recover to the 80% point by 2024 (again, given McKinsey’s scenarios). Conversely, economy chains fell by about 40%, and should recover to the 90% point by mid-2024. What’s worse, McKinsey points out that to cover costs, luxury hotels need occupancy rates 1.5X those of economy hotels. Many luxury hotels require a minimum of 100 employees just to open the doors. Economy hotels have much more flexibility in their cost structure.

McKinsey’s white paper is titled Hospitality and Covid-19: How long until “no vacancy” for US Hotels. The authors were Vik Krishnan, Ryan Mann, Nathan Seitzman, and Nina Wittkamp. Click on the title for a link to the paper itself. It’s somewhat aspirational now, but gives a great template for thinking about these issues.

Share this:

Brief thought on a Wed afternoon

For the quarter ending June 30, McDonalds (yes, the hamburger people) reported gross revenues of $3.76 Billion. Let that sink in.

Of that, only $1.59 Billion was from company owned restaurants. The rest, $2.09 Billion was fees from franchisees. (There was also some minor misc revenue, but not much.) So, of the $2.09 Billion from franchisees, $1.31 Billion was from “rents”. That’s slightly over 1/3 of their entire top line, and it pretty much all flows to the net income line. You see, McDonalds owns boatloads of real estate. They own the dirt under the franchisees locations, and rents that dirt (we call those “net ground leases”) back to the franchisees, as a way of controlling the locations.

I point this out to remind you that yes, McDonalds is in the hamburger biz, but they are much, much, more in the real estate biz. For that matter, so is every business, they often just don’t realize it.

Oh, and I’ll do the quick math for you. That means McDonalds will collect approximately $5.2 Billion in rents this year. Let that sink in, too.

Share this:

Real Estate Adaptive Re-Use

On Wednesday, I’m appearing in a video for the Appraisal Institute on adaptive re-use of real estate. It’s a panel of leading experts designed to provide guidance for AI members and others on the impact of the pandemic. My own contributions will mainly be on the adaptive reuse of brownfields and other contaminated sites, and at the other end of the spectrum, high-end properties, such as historic structures, which are worthy of preservation.. However, I anticipate a wide ranging discussion from the panelists.

Consider a building which still has life in it, or perhaps needs to be preserved for architectural or preservation reasons, but the original uses are no longer economically feasible. One of my favorite examples is the old Greyhound Bus Station in downtown Columbia, SC:

Built in the 1930’s, it was closed in 1987, but designated for preservation and named to the National Register in 1989. It was acquired by a local bank and adaptively re-used, with the old ticket windows becoming teller windows. The bank eventually left, and the building was adaptively re-used again, now as a plastic surgeon’s office. Clearly, the building still has life in it, and in fact contributes to the Commercial Historic District which is now also listed on the National Register.

Within the National Association of Realtors, there is a great organization called the Certified Commercial Investment Member Institute, or CCIM for short. The CCIM designation, awarded to Realtors who meet their exacting standards for ethics, training, and experience is analogous to the Appraisal Institute’s MAI or SRA designations. The CCIM Institute has been on the forefront of tracking adaptive re-use for quite some time now, as this is an important component of the real estate landscape. They issued a great report on this topic in 2018, and if interested, you can download it here.

The CCIM Institute is in the early states of developing an adaptive re-use index, focusing first on major CBDs such as Los Angeles, Dallas-Ft. Worth, Chicago, Atlanta, and Charlotte. Early sampling, reported in their study, suggests that as of 2018, adaptive reuse constituted 1% – 2% of all commercial real estate space in the U.S., and that figure was expected to grow to about 4% as a result of store and mall closings, e-commerce, and artificial intelligence. I would add that this growth rate will probably accelerate due to the impact of the pandemic and the resultant recession. While these numbers may not seem huge, the CCIM Institute suggests that adaptive reuse is in the early states of its lifecycle, and that this will become an important investment vehicle in the same way that historic preservation became investment-worthy in the early 1980s.

Note that Realtor is a registered trademark of the National Association of Realtors.

Share this:

ACCRE Mid-Month Report, August, 2020

Diversification is an oft-misunderstood thing. In an individual business, diversification is generally not a good idea. Internal to the business, there is an old saying, “To Dominate, Concentrate”. Indeed, few businesses have succeeeded in more than one line of businesses (Microsoft, General Electric, and to an extent Apple are among the rare exceptions). External to the business, investors like to see an individual firm concentrate in a very narrow field. That’s a function of the way common stocks work. If I invest in a firm, and it succeeds, I reap the rewards, but if it fails, I only risk what I’ve invested. Heads I win a lot, tails I don’t lose that much. This may be the core secret to why capitalism works so well.

But in a portfolio of investments, we want diversification, for two somewhat different reasons. If I pick 10 stocks at random, and half do well and half do poorly, I will be better off, from a probability perspective, than most managed funds. (The writer, Andrew Tobias, demonstrated this on television back in the 1970’s with a monkey throwing darts at the WSJ stock pages.) This explains the popularity of index funds. Second, if I have a well diversified portfolio, then the ups-and-downs of the various stocks will attenuate one another. My overall portfolio value will rise over time, but without the major swings of the individual components.

Now, that brings us to real estate (and my mid-month report). While it’s been well known and understood for many years that real estate is a great diversifier for portfolios, few investors — even the most sophisticated ones — understand how to take advantage of it. In my experience, the majority of investment advisors know very little about real estate, and hence steer their clients away from it (to the detriment of their clients!).

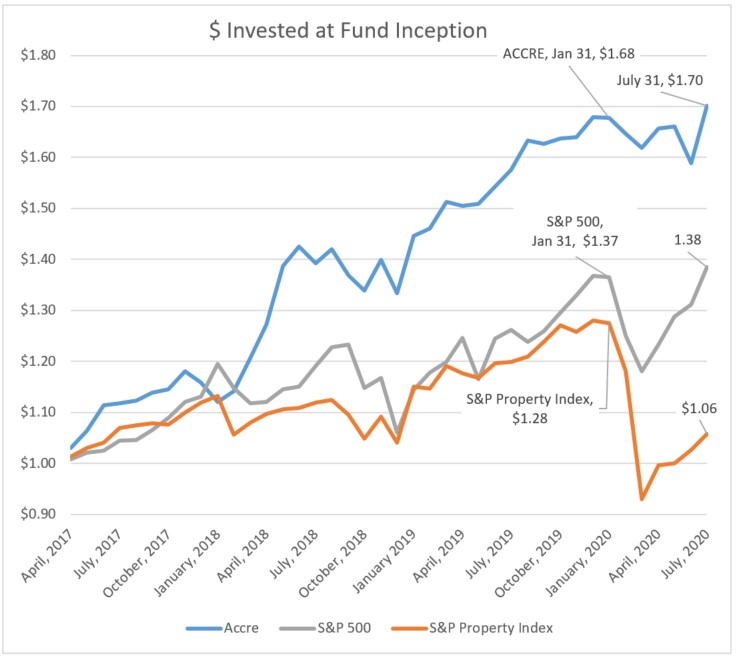

Anyway, ACCRE continues to outperform the benchmarks both on absolute terms (as noted in our end-of-month report) and on a risk-adjusted (Sharpe Ratio) level. Further, our correlation to the S&P is still right where we want it — in the positive direction, but well under 100%.

| S&P 500: | |

| Average Daily Excess Return | 0.0308% |

| Standard Deviation | 1.3537% |

| Sharpe Ratio | 2.2727% |

| ACCRE Fund: | |

| Average Daily Excess Return | 0.0526% |

| Standard Deviation | 1.1405% |

| Sharpe Ratio | 4.6079% |

| Correlation (overall): | 56.3606% |

| Correlation (monthly): | 57.3961% |

The average daily excess return is the daily return minus the t-bill returns for that day. (For consistency, we use the coupon-equivalent daily T-bill price as promulgated by the U.S. Treasury.) The Sharpe Ratio is simply that daily return minus the standard deviation, thus adjusting for volatility risk.

As we’ve noted repeatedly here, these are complicated times for both real estate and investing as a whole. A well-curated real estate portfolio can provide above-average returns, diversification, and risk attenuation. If we can answer any of your real estate questions, please let us know.

Share this:

Eminent Domain and Severance Damages

As I mentioned in my newsletter last week, several of our investment clients – and their attorneys – have called recently about eminent domain “takings” of their investment property. Specifically, the acquiring agencies often fail to understand how a partial acquisition can impact the highest and best use – and thus the value – of the part remaining.

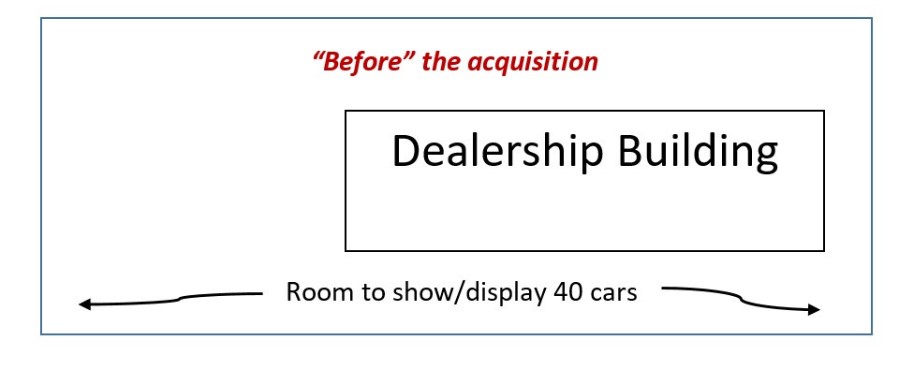

Let’s take a very simple example, which is actually drawn from our files from several years ago. A highway department wants to change the turn radius on a thoroughfare, and will “take” a slice of the front of a car dealership. The before-and-after sketch looks a bit like this:

The highway department proposed that since they were only taking about 20% of the land, and none of the building, the highway department proposed a very minimal estimate of just compensation – about 5% of the total value of the site. However, the dealer was able to successfully show that the highest and best use of this site was for a car dealerships, and those were valued heavily on the ability to provide road-frontage display of cars. Hence, the loss of the ability to display 30 vehicles was a very real damage to the remainder. The Court accepted the dealer’s theory on this, and the just compensation was significantly higher than originally proposed.

My good friend, David Matthews, and I wrote a chapter about “Rails to Trails” acquisitions in the Appraisal Institute’s 2019 book, Corridor Valuation. In it we noted, that the severance damages to the adjacent properties can often exceed the value of the rail right of way being taken. In a recent court case in Oregon, a landlord provided overflow parking for a rental house on an adjacent parcel, which was “taken” for a transportation easement. The rental house itself wasn’t touched, per se, but now the tenants would have to park on the street. The landlord was able to show that the loss of the adjacent parcel impacted the marketability of the rental house. In Sweden, they have done exensive studies on the value impact of new rail lines on adjacent residential and commercial properties, and found that the noise has a statistically significant impact on value, even when no actual land is being taken.

The examples go on, and while this may seem to be a situationally specific problem, there are extensive common themes and common methodologies which can be brought to bear to measure this. You’ll probably see more about this from us in the very near future.

Share this:

ACCRE LLC, July, 2020

It was a great month for the market as a whole and real estate in particular. ACCRE earned 7.08% in July, and is now back up above where it stood on Jan 31 (roughly, before the short bear market). Comparatively, the S&P earned 5.51% in July, and the S&P Global Real Estate Index earned 3.08%.

Why is real estate doing well? In part, because the market as a whole is doing well, and there is a lot of liquidity flowing into blue chips and safe vehicles. Further, the soft sectors in real estate were obvious from the beginning — big retail, hospitality, and such. Those tanked early. ACCRE was out of those sectors before the melt-down, so didn’t suffer as badly as the Global Real Estate index. Successful RE fund strategies this year have been fairly obvious — data centers, some industrials, selected office funds, and infrastructure. Of course, not all strategies are alike — some apartments, for example, are heavily weighted in student or senior housing. Some industrial are tied more closely to retail. Some offices are doing well, and others are exposed in the wrong areas. It’s all in the details, as they say.

Anyway, we hope your investment strategies are doing well. We’ll be back mid-month with our diversification report. Until then, best wishes, and stay safe!