Archive for August 28th, 2020

Hospitality and Covid 19

Probably no real estate sector has been hit as hard as hospitality, which of course includes restaurants, hotels, and the whole travel and leisure field. It’s a big field, employing lots of folks, and occupying lots of space.

McKinsey and Company, a widely respected research and consulting firm, released a study in June on U.S. hotels. It’s already a bit dated, but contains some great insights into how business leaders are thinking about this, and the ramifications of various public policy decisions.

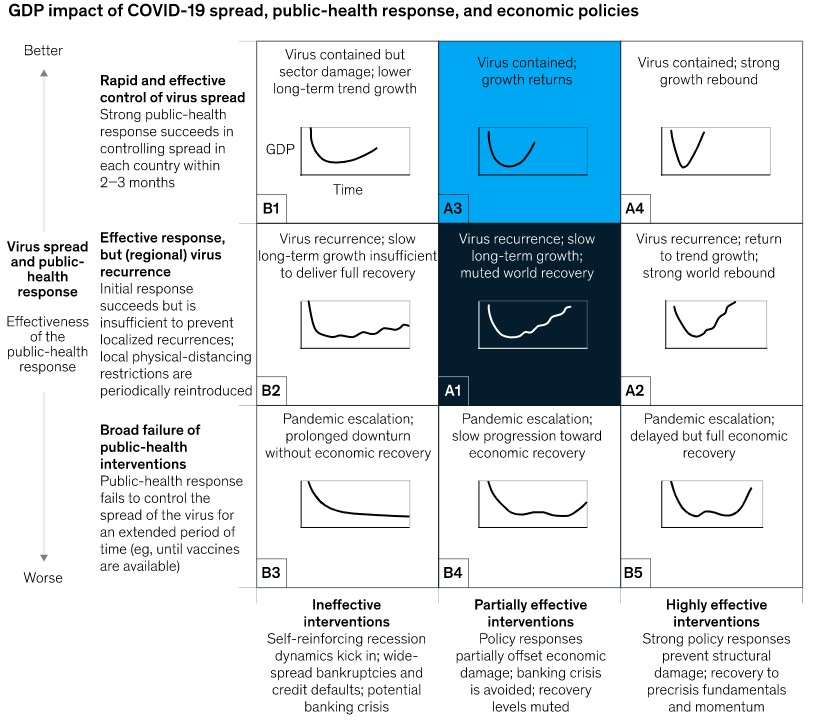

First, McKinsey constructed a common 3 X 3 matrix of low, medium, and high outcomes for Covid containment and economic impacts.

They then surveyed a large number of business leaders — which one of these do you think will be the most likely outcome? In their April survey, 31% opted for A1 (right in the middle) while 16% opted for A2 (broad success on the epidemiological front, but muted outcomes on the economics). By May, these percentages had risen to 36% and 17%, respectively. Thus, a small majority of business leaders do not believe in an economic miracle. By the way, fully 31% in May opted for B1, B2, and B3 combined, with ineffective economic results. Only 10% of respondents thought that economic interventions would be “highly effective”.

So, what does all this mean for the hotel industry? McKinsey gamed this out, and under both Scenario A1 and A3, hotel revenues are down to between 35% and 45% of 2019’s totals. They then tracked likely outcomes out to 2023, and their model suggests that under A1, hotel revenues are still down by 20% compared to 2019. Scenario A3 is much better, with a near full recovery in 2022, and revenues actually up by 2% in 2023.

Scenario A3 assumed that travel restrictions were lifted for most U.S. domestic travel by June of this year, which was only partially true, and lifted for some international travel by July, which is a mixed bag. A3 assumes that after travel restrictions are fully lifted, buying behavior will be based on economic rather than health related factors, and that there is an effective, scaled-up treatment or vaccination. Of course, neither of these has come true yet. However, there is some hope that the outcomes they had looked for in mid-year may come to pass in early 2021, and so these forecasts can be shoved down the road 6 months to a year.

By the way, not all hotels are affected the same. Luxury properties and “upper upscale” saw revenue per available room (RevPAR) fall by nearly 90% by mid-2020, and these sectors will probably only recover to the 80% point by 2024 (again, given McKinsey’s scenarios). Conversely, economy chains fell by about 40%, and should recover to the 90% point by mid-2024. What’s worse, McKinsey points out that to cover costs, luxury hotels need occupancy rates 1.5X those of economy hotels. Many luxury hotels require a minimum of 100 employees just to open the doors. Economy hotels have much more flexibility in their cost structure.

McKinsey’s white paper is titled Hospitality and Covid-19: How long until “no vacancy” for US Hotels. The authors were Vik Krishnan, Ryan Mann, Nathan Seitzman, and Nina Wittkamp. Click on the title for a link to the paper itself. It’s somewhat aspirational now, but gives a great template for thinking about these issues.