Archive for March 2022

Dysfunction in the housing market

Yes, inflation’s bad. I just bought two racks of ribs at my local grocery store. For that price, Chef Gordon Ramsey should bring them over to my house.

But I digress. This is about real estate, and Axios this morning had an excellent article by Neil Irwin with the opening line, “The U.S. housing market this spring selling season is looking like a multi-car collision…” Irwin’s focus is on mortgage rates, which “…have spiked more rapidly than they have in decades…” He’s right, but that only tells half of the story.

Let’s start with house prices, which are utterly on a tear. Since the troughs of the 2008-2011 period, house prices have rebounded amazingly. Indeed, annual price increases in the 2013 period were at nearly the same level as they were during the peak of the “bubble” (remember the bubble?). Fortunately, annual price increases settled out for most of the last decade, at the somewhat normal level of about 2% to 3% above CPI inflation. Then COVID came, and suddenly home ownership was a way to achieve social distancing, home schooling, working from home, and smart investing all at the same time. Seemingly, the urge to own a home hasn’t been so viscerally felt since the period immediately after WW-II. Supply simply couldn’t keep up with demand, and construction materials and labor prices went thru the roof as well, putting amazing price pressure on homes. If you had a $100,000 house in an average city in America in January, 1991, it was worth $382,700 at the end of 2021. Of course, that’s an a average. If that house was in Austin, Texas, it went up to $640,230. In Boise, ID, the price today would be $578,260. In Salt Lake City, it’s $625,720. These are high demand cities, folks, and people want to move there and pay whatever price it takes.

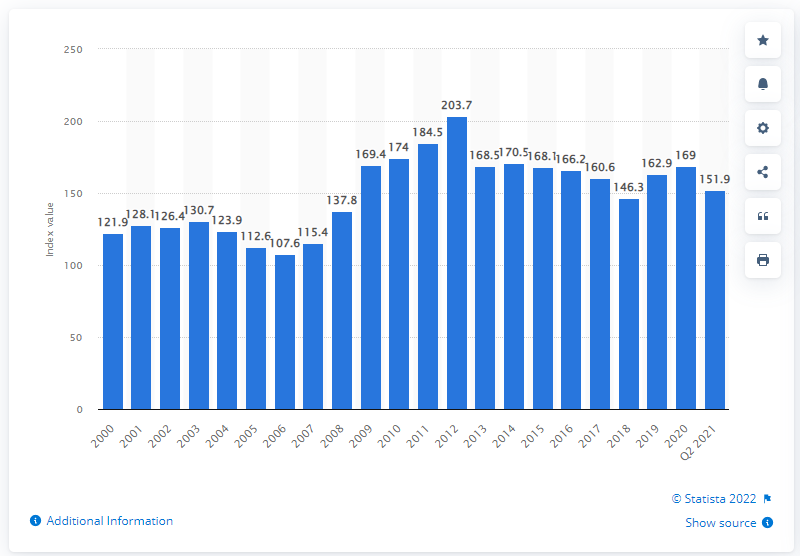

Now, add to that Irwin’s article, which is all about mortgage rates. Three weeks ago, a 30-year, fixed rate mortage was 3.76%. Today, it’s 4.42%. That means that a family which could afford a $2,000 per month house payment could have borrowed $424,000. Today, they can only borrow $375,000. Yet, prices continue to rise. We measure this with something called the Housing Affordability Index. If the HAI equals 100, then the median household in America has exactly enough income to buy the median house. Thanks to record low interest rates the past few years, the affordability index has been in positive territory (that is, above 100) since 2000, and indeed this positive affordability has fueled the run-up in house prices. However, that crashing sound you just heard was the index dropping remarkably from 169 to 151.9, the biggest year-over-year drop since the peak of the 2010-2012 recession (marked by the disappearance of extraordinarily favorable lending). While the raw numbers aren’t that bad, the trend direction, particularly coupled with all the other economic issues, does not bode well for the health of the housing market.

As always, if any of you would like to chat about this or have any comments, please reach out. I look forward to hearing from you!

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Share this:

Long time gone…

It’s been an extraordinarily busy winter! Yes, I’ve neglected this blog, my newsletter, and a host of other basic research. Why, you ask? Busy with that day-to-day “work” thing.

Whew, now that my mea culpa is out of the way, I wanted to comment on an article today by Derek Thomas in The Atlantic titled “Russia’s Economic Blackout Will Change the World.” It’s a great piece, and I encourage you to read it. However, it suggests some issues in the real estate sphere worth considering.

First, Thompson suggests that the world petroleum disruption results in the “green energy revolution goes into warp speed.” This will be particularly true in Europe, which is very much re-assessing their dependency on Russian oil. Europe has already been a lot more tolerant of nuclear than the US, despite the Chernobyl disaster, and its relatively stable energy demand (compared to Asia’s rapid demand growth) may give it the impetus to take a leading role in this transformation.

That leads a bit to his next point — Russia is about to become an economic dependency of China. China can certainly use Russia’s oil, and Russia can use just about everything China provides. Russia will rather quickly become a very large North Korea, and China will extract a steep price in terms of oil and natural gas from their new step-child. Unlike Korea, however, which shares certain cultural ties with China, this will be a tough relationship tied only by economic necessity. Further, Russia won’t be able to switch from Euro-centric oil deliveries to Chinese oil deliveries instantly. Putting in a pipeline infrastructure, particularly in the tough Asian terrain, will take years. Right now, all of Russia’s pipelines run in the opposite direction.

Thompson also notes that this war will significantly disrupt agriculture. Russia and Ukraine together produce about 30% of the world’s wheat and 20% of the corn. Russia and Belarus are also major fertilizer exporters. Thompson suggests that this isn’t entirely a bad thing in the long run for poor farmers in the world. About half of households in Sub-Saharan Africa are family farmers, living a subsistence existence. If this drives up crop commodity prices, a lot of the third could be lifted from poverty, albeit at the expense of consumers developed nations. However, this scenario suggests a long-term systemic disruption, and it is hard to imagine this war, or Ukraine’s disruption as a breadbasket, stretching out for the long-haul.

Anyway, I’ll try to be more attentive to my blog duties. See you again soon!

John A. Kilpatrick, Ph.D. — john@greenfieldadvisors.com