Archive for January 7th, 2020

Seven Biggest Real Estate Mistakes

I’m dusting off a new lecture series for 2020 with the above title. I thought I’d go ahead and give everyone a peek here on the blog. In the coming weeks, I’ll post a brief discussion on each of the seven.

Mistake #1 — Misuse of Leverage

Leverage is usually taught as a powerful advantage for real estate investors. Residential buyers can commonly enjoy loan-to-value ratios above 80% and even approaching 100% with good credit. Investors can typically enjoy 60% or 70% LTVs, and we recently advised one investment group that was offered 80% for an apartment development.

The question all-to-often is not “can you do it” but “should you do it”. Inarguably, the recent housing debacle was triggered in no small measure by the mis-use of leverage. Intriguingly, though, many shrewd investors who understood the proper use (and potential mis-use) of leverage came thru the real estate crisis quite well.

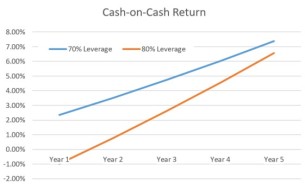

Consider a $1 million commercial investment which can be financed with either a 70% LTV loan or an 80% loan. The initial “cap rate” is 7%, and both net rents and value are expected to increase by 5% per year:

Cash-on-cash return favors 70% leverage, due to the lower debt service burden. However, in a positive-growth scenario, the 80% leverage situation catches up after year 5. As far as equity return is concerned, it is hands-down an 80% leverage race, with much steeper increases from the start.

However, consider a model with some negative returns. Let’s say, just for an example, that rents actually decline by 10% after year 1, but then return to a positive trend after that. The scenario is quite different:

With just a little negativity, the 70% LTV model dominates cash-on-cash return, in fact dominates the equity return until after year 4. Naturally, these sensitivity analyses can be run quite easily for any one of a number of potential scenarios.

So, what do the smartest folks in the room do? One clue comes from successful REITs, many of which enjoyed positive returns thru the last recession. Admittedly, REITs in problematic sectors (mortgage REITs, for example) were in trouble. However, every sector faced struggles with vacancy, collections, and rent growth during the recession. REITs that are successful in the very long turn use leverage sparingly. For example, Hudson Pacific Properties, which owns about 50 or so office buildings on the west coast, has about $7.5 Billion in assets. They are only leveraged about 47% as of the last SEC filing. Essex Property Trust is one of the largest apartment REITs, with about 60,000 apartments across the U.S. Their $13 Billion in assets are funded by only about 50% debt, even though apartments are generally recognized as fairly low on the risk scale.

In general, well-managed real estate portfolios maintain leverage somewhere south of 60% or even 50% in more risky sectors. While real estate is generally considered to be a great hedge against troubled economic times, that hedge won’t work if it is over-leveraged. Leverage can be your friend, but can at times also be your enemy.

As always, I or colleagues at Greenfield may or may not have investments in firms mentioned in this blog. Mentioning a firm in this blog is not to be construed as a recommendation to buy, sell, or hold a particular investment. Always consult with your advisors on these matters.