Archive for January 2020

Fed meets — yawn

I don’t mean to be snide, but pretty much everything released today was fully discounted in the market. For a great and detailed synopsis of today’s release, see Jeff Cox’s excellent article at CNBC here.

The short answer is that the FED will keep the benchmark funds rate at 1.50%-1.75% for the time being. (Market prognosticators foresee no changes at least thru the end of the 3rd quarter.). Of more interest, the Open Market Committee has agreed to continue its repo activities for the time being. This has been described by some as a form of quantitative easing, and has boosted FED reserves to over $4 Trillion — not unlike the explosion in the monetary base we saw after the 2008 meltdown. Indeed, very little of the monetary expansion from that era had been liquidated before the current operations began.

Graphic courtesy SeekingAlpha.com, October 24, 2019.

The repo process allows banks to sell high-grade instruments to the FED in trade for much-needed liquidity. One can pretty much track the stock market performance of late to the repo activity. Forecasters generally predicted a continuation of this, and not surprisingly the S&P has performed well, if not spectacularly, since the announcement today.

For the initiated, there are actually two “FEDs”. The 7-member Federal Reserve Board oversees the operation of the Federal Reserve System itself. The meat-and-potatoes policies, such as today’s, are the province of the Fed Open Market Committee, made up of the 7 fed members, the president of the NY Fed Bank, and 4 of the other 11 bank presidents (a rotating membership). There is no rule that the FED chair also chair the FOMC, but that’s been the custom since 1935 when the FOMC was created.

Share this:

Seven Biggest Real Estate Mistakes — Part 2

Two weeks ago, I introduced this series as a sneak peek at a new lecture series I’m developing for this year. We hope to kick this off coincidental with the March release of my new book, Real Estate Valuation and Strategy.

Mistake #2 — Overpaying

Doesn’t this seem like common sense? It really should be, but it’s amazing how many overpriced deals close every day.

Overpricing is often tied to falling in love with a property, an investment, an investment pool or team, or just being sloppy and having to put some money somewhere. A real estate mentor of mine w-a-a-a-y back when taught me about the importance of walking away from a bad idea — that there will always be another “deal” coming along tomorrow. There is no amount of inflation, great management, or market demand that will get you back to even on an over-priced investment.

For example, imagine a small investment which should throw off $1 million in Net Operating Income (NOI) during the first year. Rents and net operating income are expected to grow by about 4% per year. The market currently values investments of this type and quality at a capitalization rate of about 8%, and we expect this to remain fairly constant for the foreseeable future. Thus, the indicated value, and purchase price, should be about ($1mm / 8% = ) $12,500,000. However, for a variety of reasons, you are coaxed into overpaying for this — paying a “cap rate” of 7%, which translates into a purchase price of just over $14 million. Obviously, this is a materially large difference, but more importantly, getting back to even will take some serious time.

Since the value at any point in time is the capitalized income, and income is increasing, then the “fairly” purchased investment should always be worth more than we paid for it (ignoring transaction costs and such). However, the badly-purchased investment will be underwater until sometime in year 3, and that is only if everything else works out right. Of course, we will be collecting rents, which increase year-to-year, so that will offset a bit of the mistake. However, the overall return on investment (ROI) for the badly priced project will simply never catch up with the well-priced project.

If we had to sell the badly-priced property at the end of year 1, we’d actually have a negative ROI, even accounting for rents collected. ROI (including both sales proceeds and collected rents) turns barely positive in year 2, but will never actually catch up.

What’s worse, investors stuck with overpriced properties eventually realized that they overpaid, and invariably these become the neglected mutts in the portfolio. I’ve often seen overpaying to the extent that no amount of increasing rents will ever bail out the bad purchase price. Invariably, such properties get neglected in favor of properties with better anticipated ROIs, and are often the last to be sold if a portfolio needs to be liquidated. Remember, too, that in a liberal lending environment (such as we have right now), banks can be enablers of such mistakes, lending too much money on too little project. In those scenarios, the actual loan-to-value, and the actual debt-service-coverage, will exceed the expectations, and the investors will find themselves owing too much money for too little collateral.

How to avoid these situations? I would suggest five rules for taking on any real estate investment:

- Be sure to get the advice of an independent consultant or appraiser. Pay someone who doesn’t have a horse in this race to evaluate the deal.

- Beware of projects that only seem to work with complex financing structures. I recently looked at a project that was attractive because the general partner had extremely favorable financing. Once we re-evaluated the project with market-normal financing, the pricing of the deal made no sense.

- Beware of the seller’s estimates of expenses, revenues, vacancy and collection problems, and miscellaneous rents. Test these against market norms, and re-evaluate the operational structure against various scenarios.

- Be very concerned when you hear the phrase, “if this works out the way we plan…” (There is an old proverb: If you want to hear God laugh, tell him your plans.)

- Never be afraid to walk away from a deal.

I’m a big fan of value-added or opportunistic investments, of which there are always plenty available. In that context, chasing overpriced investments is a real waste of time, effort, and money.

Share this:

Seven Biggest Real Estate Mistakes

I’m dusting off a new lecture series for 2020 with the above title. I thought I’d go ahead and give everyone a peek here on the blog. In the coming weeks, I’ll post a brief discussion on each of the seven.

Mistake #1 — Misuse of Leverage

Leverage is usually taught as a powerful advantage for real estate investors. Residential buyers can commonly enjoy loan-to-value ratios above 80% and even approaching 100% with good credit. Investors can typically enjoy 60% or 70% LTVs, and we recently advised one investment group that was offered 80% for an apartment development.

The question all-to-often is not “can you do it” but “should you do it”. Inarguably, the recent housing debacle was triggered in no small measure by the mis-use of leverage. Intriguingly, though, many shrewd investors who understood the proper use (and potential mis-use) of leverage came thru the real estate crisis quite well.

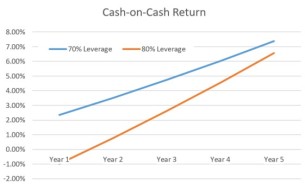

Consider a $1 million commercial investment which can be financed with either a 70% LTV loan or an 80% loan. The initial “cap rate” is 7%, and both net rents and value are expected to increase by 5% per year:

Cash-on-cash return favors 70% leverage, due to the lower debt service burden. However, in a positive-growth scenario, the 80% leverage situation catches up after year 5. As far as equity return is concerned, it is hands-down an 80% leverage race, with much steeper increases from the start.

However, consider a model with some negative returns. Let’s say, just for an example, that rents actually decline by 10% after year 1, but then return to a positive trend after that. The scenario is quite different:

With just a little negativity, the 70% LTV model dominates cash-on-cash return, in fact dominates the equity return until after year 4. Naturally, these sensitivity analyses can be run quite easily for any one of a number of potential scenarios.

So, what do the smartest folks in the room do? One clue comes from successful REITs, many of which enjoyed positive returns thru the last recession. Admittedly, REITs in problematic sectors (mortgage REITs, for example) were in trouble. However, every sector faced struggles with vacancy, collections, and rent growth during the recession. REITs that are successful in the very long turn use leverage sparingly. For example, Hudson Pacific Properties, which owns about 50 or so office buildings on the west coast, has about $7.5 Billion in assets. They are only leveraged about 47% as of the last SEC filing. Essex Property Trust is one of the largest apartment REITs, with about 60,000 apartments across the U.S. Their $13 Billion in assets are funded by only about 50% debt, even though apartments are generally recognized as fairly low on the risk scale.

In general, well-managed real estate portfolios maintain leverage somewhere south of 60% or even 50% in more risky sectors. While real estate is generally considered to be a great hedge against troubled economic times, that hedge won’t work if it is over-leveraged. Leverage can be your friend, but can at times also be your enemy.

As always, I or colleagues at Greenfield may or may not have investments in firms mentioned in this blog. Mentioning a firm in this blog is not to be construed as a recommendation to buy, sell, or hold a particular investment. Always consult with your advisors on these matters.