A brief primer on interest rates

Someone asked me, “Should I wait to buy a house since interest rates are headed to zero?”. Huh… well, dude, I got bad news for you – – interest rates whipped past zero a while ago. Denmark just this week issued some bonds with negative yields. I’m not saying this is as low as it gets, but it might be helpful to understand a bit more about how interest rate changes affect the consumer.

First, note what I’ll call “wholesale” rates and “retail” rates. I bought a dozen eggs this week at the grocery. Locally sourced, cage free, no anti-biotic eggs, from chickens that ate a nice diet of bugs and stuff — the sort of stuff chickens like to eat. I paid $3.99 (plus tax). I’m sure we can both agree that the farmer didn’t get all of that $3.99. Some of it went to the grocer. Some of it went to the truck driver. Some of it went to the wholesaler. The farmer was probably lucky to get $2 (but that’s another story).

Mortgage loans are like that. Most mortgages get bundled into mortgage backed securities and sold through a somewhat complex pipeline to investors (Fannie Mae, Freddie Mac, certain trusts and pension plans, etc.). These trusts cannot purposely buy paper at negative yields. The managers have a fiduciary duty to their clients not to do that. Hence, there is a floor below which wholesale mortgage rates cannot fall, and that floor is not a negative number.

Now, above that floor, everyone has to get a piece of the action, just like the people in the pipeline who sold me eggs. Let’s face it, they have bills to pay, and want to take home a paycheck on Friday, just like the grocer and the truck driver. Finally, there is a fee for servicing the loan, which has to be added to the top before you hear about the retail rate. W-a-a-a-a-y back when I started in this game, that fee was statutorily set at 55 basis points, or 0.55%. Thus, if you had paid 10.55% for your mortgage (not a bad rate back then), the point-five-five part went to the people who collected the monthly payments, kept the books, made sure you paid your taxes and insurance, and handled the foreclosure if it came to that. The remainder — the 10% part — went down the pipeline to all the investors. The laws were changed a number of years ago, and the servicing rights have become competitive (in other words, the fees have dropped). However, it’s still a real, positive number.

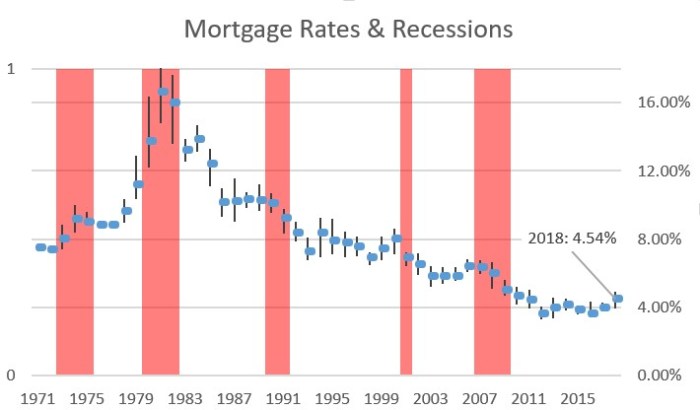

Probably the more interesting question is what happens to mortgage rates before, during, and after a recession. Since everyone seems to think one is coming, how should we be prepared? Here is a chart of mortgage rates (high, low, and average) versus the years in which we had a recession.

We’ve actually had 7 recessions since 1970, but a couple of them ran into one another, so this chart only shows five recessionary periods. No matter, for our purposes. Note that in the first two, we were going thru a period known as “stag-flation” where the impacts of the recession were exacerbated by high inflation. Since the 1980’s, inflation has more-or-less been throttled, so those recessions are more useful as predictors. From 1989 until 1992, average mortgage rates dropped about 2 percentage points (from 10.32% to 8.39%). From 2000 to 2002, spanning the shortest of these recessions, rates fell about a half of a percentage point (from 7.44% to 6.97%). Before-and-after the recent housing melt-down and recession, rates fell from 6.41% in 2006 to 4.69% in 2010 — a difference of slightly over two percentage points.

The average 30-year, fixed-rate mortgage in 2018 was 4.54%. Today, most lenders are quoting a rate of 3.75% on that same mortgage. Could rates drop two percentage points (to 1.75%) in an incipit recession? History suggests that is entirely a factor of the length of the recession. A brief dip, such as happened in 2001, might have little impact on mortgage rates. A longer recession would probably have a more dramatic impact. Notably, of course, there is an absolute floor, and it’s not at zero percent.

Leave a comment