Archive for April 2019

Sad news from Seattle

It’s been a busy April, and sadly, this blog gets shoved to the back burner w-a-a-a-ay too easily. But, two very sad issues from Seattle have attracted my attention of late, and I wanted to comment on them.

First, we are all saddened by the loss of life from a high-rise crane that collapsed on Saturday. The crane was working on the new Google campus, located in the hot South Lake Union area, just about a mile north of downtown. Our hearts go out to the four people killed and the others injured in this terrific incident. Given the proliferation of cranes in Seattle, we hope the authorities immediately get to the bottom of the cause of this tragedy and learn from it.

That leads, inexorably, to the second sad thing. A TV station in Seattle, owned by a an out-of-town consortium with no ties to Seattle, produced an editorial (labeled as a documentary) titled “Seattle is Dying”. This editorial has garnered some attention among the chattering class who believe Seattle is badly governed. Now, everyone is entitled to their opinion, and I am a firm supporter of the First Amendment. That said, labeling an “opinion” as a “documentary” is a bit disingenuous, but that’s what the fringe media does now-a-days. I am also not really the biggest supporter of Seattle’s governance, but that’s another story entirely.

What I really wanted to point out is that Seattle has the highest number of these high-rise cranes of any city in the United States. Read that sentence again, folks. We’re the 20th largest city, but #1 in high-rise cranes supporting our exploding skyline. From a real estate development perspective, Seattle is the hottest market in the country right now, if not the world. If you believe in Richard Florida’s concept of the “creative class” (and I certainly ascribe to that), then Seattle is the center of the universe. The arts, sciences, education, economy, and business opportunities in Seattle are all world-class.

Now, admittedly Seattle has it’s problems, as does every city on the globe. We have a really serious homeless problem, our transportation infrastructure needs attention, and to quote one famous NYC politico, “The rent’s too d*&^ high!” But dying? Me thinks the TV folks protest too much…

Share this:

Yield curves and real estate

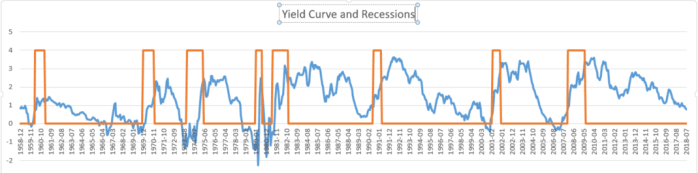

Every economist and his kid brother are out there touting the negative slope on the yield curve as a harbinger of the Apocalypse. I have to confess I raised the issue in a blog post back in August. (https://johnakilpatrick.com/tag/recession-risk/) Dr. Ed Yardini of Yardini Research released some charts yesterday which suggest that all this wailing and rending of clothes may be a bit premature (https://www.yardeni.com/pub/bearmktind.pdf). Nonetheless, none of this says anything about the yield curve and real estate.

To reflect, here is the core chart I used back in August, although I’ve updated it to reflect end-of-February numbers. Note that as of the end of February, the yield curve was still positive. It didn’t turn negative until last week.

The orange line notes the incidence and length of recessions. (I happen to use 6-month t-bills in my data, while other analysts use 3-month. The difference is negligible.)

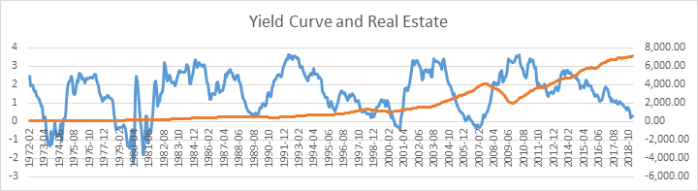

Last week, I took a look at the NAREIT index back to 1972 (the earliest data I have available). Admittedly, the NCREIF index might be a bit more telling, but NAREIT also includes income along with capital gains, and as a matter of simplicity, I don’t have NCREIF data handy right now. Anyway, I did two things. First, I replicated the chart above but rather than looking at the incidence of recessions, I looked at the incidence of down-turns in the NAREIT index. To smooth thing out, I used a 12-month moving average. The results are visually interesting, and in fact very conclusive.

As you can see, real estate returns, when viewed on a 12-month scale, have been fairly positive almost continuously since 1972, with the exception of course of the “great recession” of 2007-2009. Indeed, visually there appears to be no relationship at all between the yield curve and real estate returns.

To analyze this a bit further, I looked at the relationship with a simple regression. There is simply no relationship at all (p-value = 0.50) between the yield curve and real estate returns. Indeed, notably, the real estate downturn in 07-09 followed a yield curve inversion, but by over two years. I think few economists would disagree that the 07-09 downturn was related to a host of structural issues, and had very little to do with a yield curve inversion. Indeed, one might posit that the yield curve inversion was driven by real estate returns, and not the other way around!

In short, while the stock market may be shuddering from yield curve flu, the real estate markets are another thing entirely. That’s one of the reasons why properly and expertly curated real estate is usually viewed as an excellent diversifier in a portfolio.