Archive for the ‘Uncategorized’ Category

Commercial real estate — MAYBE some good news

All of us in real estate know that some commercial property and investment sectors have been hit pretty hard. Our ACCRE fund-of-funds avoided those sectors (several of those were already over-valued before Covid hit) and has held its own, and continues to perform well against its benchmarks. Note, of course, that ACCRE is a carefully curated fund, and we’ve continued to monitor the portfolio.

Conversely, offices, hospitality, and retail are really at a cross-roads. A lot of equity had disappeared from those sectors and from funds which were heavily weighted in those sectors. However, are the fundamentals sound? That is, are we looking at cyclical downturns or are we going to be left with a lot of marginally worthless property when this all ends?

One signal – and it’s not at all a perfect one — comes to us from the Exchange Traded Funds (ETF) sector. Specifically, I’m looking at the iShares CMBS ETF, which purports to invest in high-grade commercial mortgage backed securities. This fund has had a very real bull market tear since late 2018, in no small part due to a solid yield in the face of an inverting bond curve. Since late 2019, it’s been extraordinarily volatile, and indeed its 50-day moving average has cycled twice in the last 3 quarters. However, for the past month or so, it’s been solidly up. This does not suggest that traders and investors think that the coast is clear for commercial real estate — far from it. However, it does suggest that the market thinks there is enough equity underpinning these loans to continue making mortgage payments.

Graphic courtesy iShares, as of mid-day, 6/26/20

Now, this all needs to be taken with several grains of salt. For one, the market as a whole has regularly proven itself fickle, if not outright wrong, several times in the past few months. Second, going into the last recession, Residential Mortgage Backed Securities (RMBS) were doing just fine until… well… they weren’t. However, this is a useful and potentially important data point that shouldn’t be missed by savvy investors.

On the other hand, what do we do with securities when markets peak?

Share this:

Nice quote this morning…

… in an article by Geoff Williams in U.S. News and World Report.

https://money.usnews.com/money/personal-finance/spending/articles/smart-ways-to-spend-1000

Of course, the interview was a but longer, and I noted that the thing that might be the best for the individual (socking the money away in the bank for an even rainy-er day than now!) might not be the best for the economy as a whole. If you really want to use “stimulus” money to stimulate the economy, then it needs to be spent, locally, on job-creating things. Money spent in that fashion quickly multiplies thru the economy. The local barber spends money to get his kid’s teeth fixed at the dentist, and then she uses that money to shop at the local car repair mechanic, who in turn buys from the local farmer’s market.

Best wishes, everyone, and stay safe!

Share this:

Another one bites the dust (maybe)

Now I read, today, that Tailored Brands (TLRD) is meeting with bankruptcy consultants. If you’re not familiar with them, you may be more familiar with the stores they run: Men’s Wearhouse, Jos. A. Banks, and K&G. They’ve been strong players in the clothing biz for quite a few years, and while bankruptcy doesn’t necessarily mean going out of biz entirely, at the least it will mean some painful restructuring of complex webs of contracts, debt, and banking relationships. My interest is in the real estate side.

Real estate usage changes over time. We think of these changes as slow, but in fact they can come fast and furious. For example, the 1920’s was a decade of explosive growth in the “built environment”, and many of the downtown city street facades date to this period. The depression put a halt to the 20’s growth, only to see suburbs explode after WW-2. The baby boom gave rise to shopping centers, neighborhoods anchored by elementary schools, and commuting on superhighways. Even though the “great recession” of 2009-10 was centered on real estate imploding, we really didn’t see a seminal change in the way people live and work. Home ownership went from about 69% to it’s historic, post-WW-2 level of about 64%. Shopping malls hung on for dear life, and the continued construction of big-boxes was unabated. If anything, real estate experts sat around wondering when, if ever, the Amazon phenomenon would catch up with brick-and-mortar stores. To an extent, the continued prosperity after 2010 put pause to any major changes.

Now, I’ll drop the other shoe. This year marks the fiftieth anniversary of Alvin Toffler’s Future Shock. Yeah. I know. If there is one resounding theme in Toffler’s work, it is that in the future, change will come at an increasingly fast pace. Hence, it should come as no surprise that the first six months of 2020 seem like a decade. So, with that in mind, a few observations…

First, the resurgence of downtowns in prosperous cities (Seattle comes to mind) assumed that people were willing to suffer with small residences (usually apartments or condos) in trade for a vibrant social scene on the streets and in restaurants, bars, entertainment facilities, and such. Last week, the AMC Theater chain announced that they probably could not survive the Corona Virus Pandemic. A significant number of people — not everyone, but a lot — will opt out of the social scene. I’m not suggesting we will become a nation or world of hermits, but three things are coming together to hit the reset button on this utilization model: a long time for people to “catch up” on discretionary spending after this nasty recession, a heightened sense of the risk of lending or providing credit to restaurants and bars, and an overall reluctance to rub elbows, at least by some folks.

Second, it’s not just retail, but it’s all the other stuff that supports brick-and-mortar retail. Every time you buy a pair of socks at Jos. A. Banks (and yes, they have very nice socks), someone had to deliver those from a warehouse. Now, of course, you are at least marginally likely to buy those socks from Amazon, and yes, they have warehouses, too. However, Amazon and their network of small businesses tend to be a bit more efficient than most brick-and-mortar retailers, and as such need less space and fewer people. Further, until the aftermath of this recession is over, it’s a simple fact that people will buy fewer socks, and fewer Ford F-150s, and fewer Weber gas grills. Not withstanding my previous jokes about Captain Morgan sales, reports have it that distilled spirit sales in America have been hit so badly as to endanger many famous liquor brands. Add to this the fact that “necessities” (e.g. — groceries, health care) are skyrocketing in cost, and you can quickly see that merchants focused on discretionary goods may have problems.

Owner occupied housing is nearly at a standstill. Real estate “listing” agents are having to be terrifically clever to sell homes. A lot of sales come from transfers, and there is little of that happening this summer. People are hunkering down, taking down the for-sale signs, and trying to keep their powder dry. By the same token, home builders, who have never fully recovered from the past recession (a story for another day) are now sitting on inventory they can’t sell. It’s not nearly as bad as 2008/9, but it’s not good, either.

A lot of construction happens by governments, both for new buildings and for public infrastructure. You can imagine that the brakes have been hit solidly on that. Transportation projects, which are often dependent on fuel or transportation taxes, are probably hitting the skids right about now.

There are some bright spots. Working from home demands a lot more bandwidth. Connectivity providers are doing what they can. If this trend continues, we’ll also see a marked demand for more cloud storage, which despite the name actually happens in places that look like warehouses full of computers.

Finally, and this is not entirely obvious, but existing rental units with tenants will do just fine, but new rental units will see longer periods to rent-up and get to stabilized levels. Why? Mainly because there will be less moving around and greater tendency for increased tenure in rental units. Existing landlords will increasingly cut deals to keep tenants in place, while new, vacant spots will have trouble competing for those tenants. In the residential rental space, this will be ameliorated a bit by the noted probable decline in home ownership. In the commercial space, even for industries that are doing fine, there will be difficulty competing for new tenants.

So there’s that. Some random thoughts for a Sunday afternoon. Y’all stay safe out there, and I look forward to hearing from you.

Share this:

ACCRE LLC, May, 2020

All of us at Greenfield Advisors hope all of you are staying as safe as possible as we continue thru this Covid pandemic!

As noted last month, ACCRE continues to perform well, having recaptured most of the bear impacts. None-the-less, we made some portfolio adjustments in late May to drop a few laggards and add a few positions we felt would serve well going forward this year.

As you probably know, the S&P 500 had a great month, but still lags behind ACCRE both lifetime returns as well as performance since the Feb-March bear slump. The overall S&P Global Property Index is just back to level territory, and had a dismal May.

We’ll be back mid-month with some portfolio metrics. Stay safe out there!

Share this:

ACCRE Mid-Month Report

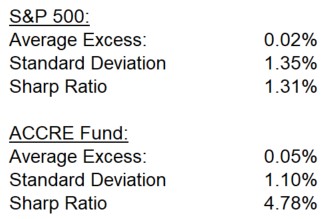

I hope all is well with everyone! ACCRE continues to chug along, doing somewhat better than the market as a whole. That said, this is the point in the month when I USUALLY provided the market diversification statistics, the Sharpe Ratio, and such and so-forth. I say USUALLY because, frankly, with all the Coronavirus mess, I’ve fallen w-a-a-a-y behind in my reporting duties. Mea culpa and all that, so let’s get started.

For those of you unfamiliar with the terminology, the Sharpe Ratio is a measure of “excess returns” adjusted for risk. What do we mean by “excess returns”? It is the average daily return of the security over and above what would have been earned had that money simply been put into T-bills. (For our benchmark, we use the 13-week, coupon-equivalent rate as published daily by the U.S. Treasury.) The average excess return is then divided by the standard deviation, which is a measure of the volatility risk. Hence, the higher the standard deviation (volatility), the lower the Sharpe Ratio. An investment with a high return and low volatility will have a correspondingly higher Sharpe Ratio. We measure the Sharpe Ratio over the life of the fund (since April 1, 2017):

ACCRE has enjoyed both a substantially higher average excess return over its life as well as somewhat lower volatility. Thus, it comes as no surprise that the Sharpe Ratio is nearly four times that of the S&P 500.

One other thing we monitor is the correlation between ACCRE and the S&P 500, which has been historically low — about 41% as of the end of 2019. Indeed, the correlation for the month of December was only 4.8%. Of course, monthly correlations of daily returns suffers from small sample bias, which is one reason why we focus on “lifetime of the fund” statistics. With that, I would note that the correlation over the past few months has been quite high, driving the overall correlation up to about 56%. Still, though, this suggests that ACCRE does a superior job of providing diversification for the portfolio.

We’ll be back after the first of June with our monthly returns report. Best wishes to you all!

Share this:

ACCRE LLC, April 2020

Wow, it is almost the middle of the month and I am JUST getting around to our April report. Mea Culpa, everyone. We’ve been busy. Not a great excuse, but it’s the one I have!

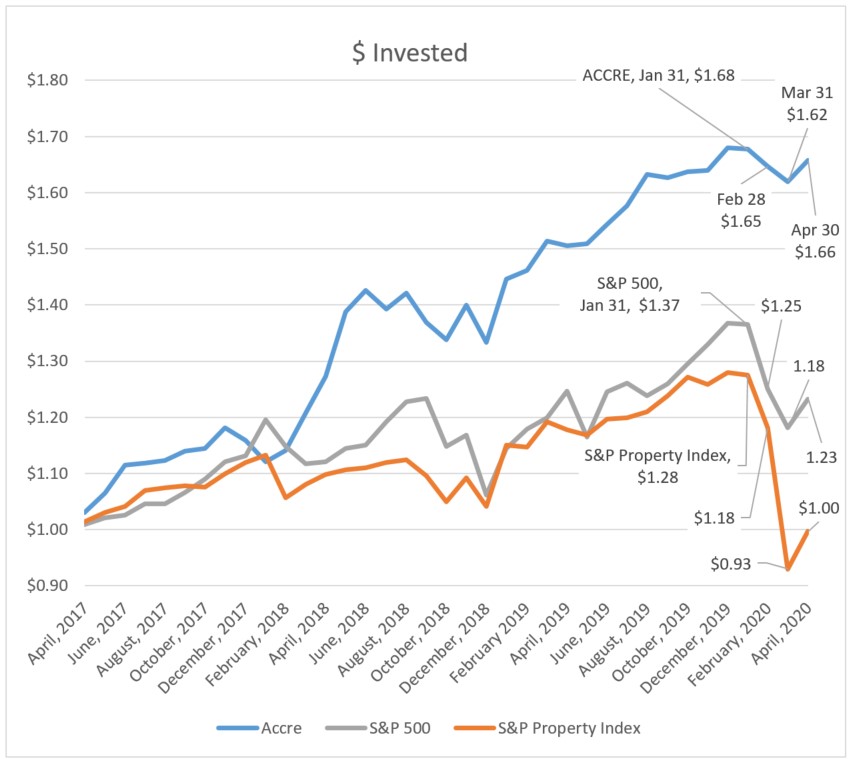

April was a nice rebound month for everyone. Since ACCRE didn’t fall very far, it comes as no surprise that the rebound was comparatively slight. Nonetheless, ACCRE continues to dominate the comparative indices by a tremendous margin.

(For the new readers, these indices are based on a dollar invested as of the inception of our ACCRE fund, April 1, 2017.)

More to the point, since January 31, ACCRE is only down 1.2% ($1.66 versus $1.68). Comparatively, since January 31, the S&P 500 is down 10.2% while the S&P Global property Index is down almost 22%.

I’ll be back in a few days with comparative portfolio stats and such. And, as always, our newsletter subscribers get updates on portfolio makeup and any trades we make.

Best wishes, and stay safe!

Share this:

Seven biggest real estate mistakes — part 4

Back in the winter, I began this series, and then we all got distracted with other things. In the interim, I’ve been deluged with e-mails about real estate investing, and particularly when would be the right time to look for opportunities. Whoa! Slow down, folks! Real estate prices and values aren’t like tech stocks Indeed, in 1991, when we were just coming out of a recession, real estate prices only moved about 1.85% all year. Trying to time the real estate market — and developing an anxious ulcer about it — leads us to our fourth mistake:

Mistake #4 — Trying to catch a falling knife

I include in this all of those anxious decisions about buying impetuously, and not taking the time to carefully examine the market to see how things play out.

No question about it, this recession is going to be terrible, and particularly so for home owners who are over-extended on their mortgages. The mortgage market TRIED to discipline itself after the last recession, taking care about making stupid loans (a category that included a lot of garbage back a decade or so ago). That said, there is still a lot of stuff out there that will land on the chopping block. I just read a piece this week about folks who bought homes specifically to rent via Air B-n-B. The lenders counted the anticipated Air B-n-B revenues as income for purposes of making the loans. A lot of these are going back to the bank this summer.

The 2009/10 recession was very different. It was, in no small part, caused by bad real estate lending. When loans began to default — as loans do from time to time — this caused a recession. House prices continued to fall during the recession, but then there was an echo effect after the recession was over. House prices stabilized, and then dropped even more after the recession was finished.

This recession is clearly caused by other factors, and so housing and real estate failures in general will be effects of this recession, and not causes. Worst case scenario, people who lost their jobs in March (and a lot of folks did) didn’t make their March house payment. It takes about three of those missed payments to get in really serious trouble, and then several months afterwards before a property gets back into the bank’s “REO” portfolio. Banks then have statutory requirements, so the first wave of RE foreclosures won’t even get into the market for another year or so.

Now, here’s a bit of a secret. Many if not most of those “first wave” properties will go on the market at inflated prices. I’ve found that lots of investors rush into auctions and pick up anything laying around, having watched too many of those “flipping” TV shows. Those properties may not go on the market, at reasonable prices, for several years. I’m currently still looking at properties that went into initial foreclosure in 2009. I’m not kidding.

So, don’t try to catch a falling knife, have a strategy, stick too it, and be careful in your investments.

Share this:

Real estate and the pandemic

I’ve been reluctant to talk about this just yet — maybe it’s too early, and anyway, I’m a data driven guy, but here goes. Maybe if I talk about it, it won’t happen.

The recession of 2009/10 completely changed the face of the real estate finance market in America. The sub-prime meltdown was in no small part precipitated by the onset of the recession, with slow-rising unemployment causing a domino effect on loan distress, foreclosures, and the failure of mortgage backed securities. Now, the parallels cannot neatly be drawn — the last recession was in many ways caused by the fools gold of crappy lending practices. Further, as we now know, there was a huge “shadow banking system” (to use the terminology of Tim Geitner) and the underpinnings of the financial market were week and shallow.

However, it’s interesting to note that unemployment only reached about 9.6% last time. Last week, Goldman Sachs forecasted 15% – 20% this time, and that was BEFORE this morning’s new jobless claim pronouncement. We know this afternoon that the Treasury system to distribute loans and grants to small businesses is badly broken. The President’s dream of a “V” shaped recession, with a sharp recovery before summer, is now a distant and dissolving cloud. We are in this for the long slog, folks.

Which leads us to real estate. A few cautionary notes — I hesitate to call these predictions, but these are certainly things I’d look out for:

- New home construction will basically stop, with all of the economic nastiness that comes with that. We know from reports this morning that new home starts are already down 23%.

- Despite the end of “subprime” lending, there are a LOT of 100% loan to value loans out there. It’s not unreasonable to think of distress and foreclosure rates topping 10%. (Some sub-prime pools saw distress and foreclosure rates topping 50% in the last recession.)

- A lot of investors bought rental properties in the past few years. If you own those free-and-clear, expect some retrenchment in rent collections, perhaps 20% or more. If you leveraged your investments, as so many “flippers” and speculators did, well, I’m sorry.

- People turning 65 with good jobs, and 401-K’s that just tanked, will not be retiring any time soon. That stagnates the hell out of the labor pool, and makes it tough on younger folks to start households. In 2010, household formation actually turned negative.

- And that’s just residential real estate. Consider retail. Huh… Yeah…

- A LOT of farms in America are geared to grow crops for food service, restaurants, etc. That market will be very slow coming around, which will exacerbate the farming crisis.

Now for the other side of the coin. We REALLY need to re-think elder care in America, and the structure and management of elder are facilities. There is a huge and growing real estate story to be told there. We will also most likely see a LOT of people working from home. There is a real sadness there — people LIKE to work in groups, and get vitality and intellectual stimulation from working in groups. That said, a lot of businesses will be looking for ways to cut back on the office overhead.

I’m just thinking out loud here. I’d appreciate a dialog with any of you on these and other topics. Best wishes,

Share this:

ACCRE LLC

In the past I’ve maintained two separate “blogs” — this one and one for my private REIT Fund of Funds, ACCRE LLC. This latter blog has become a problem on a technical level, and frankly a pain in the neck to separately maintain. For that reason, I’m merging the two effective this month. From now on, my twice-monthly ACCRE LLC updates will appear here, rather than there.

For the uninitiated, ACCRE is a traditional long-short hedged fund invested in publicly traded Real Estate Investment Trusts, or REITs for short. Over the past three years, it has outperformed the S&P by about 3.5 to 1, and also significantly outperformed the S&P Global Property Index. It also has less than a 50% correlation with the S&P, and so provides a great diversification benefit for a portfolio. I publish the end-of-month results as near as I can after the month-end, and then about the middle of the month produce some updated diversification metrics (Sharpe’s Ratio, correlations, etc.)

So, with that in mind, those same technical difficulties prevented me from doing my regular end-of-month update for March. Here tis’, folks…

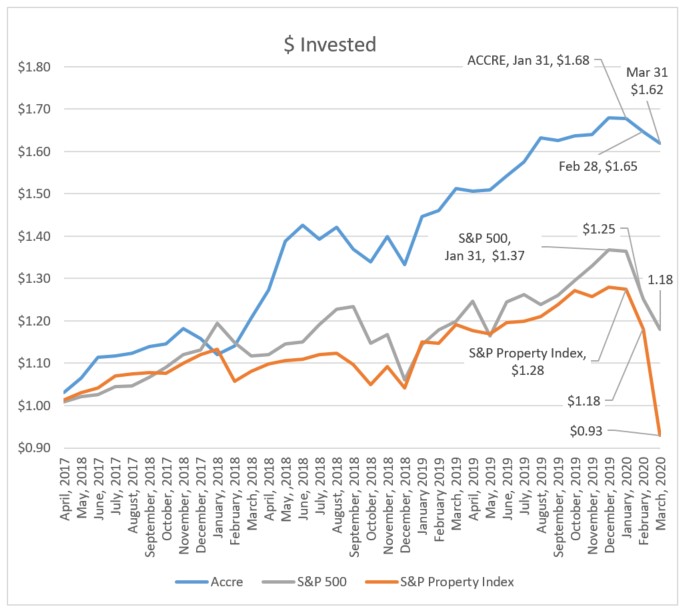

ACCRE and the broader market for that matter had a terrible February and March. That said, ACCRE seemed to level off a bit in March, relative to other investments, while the S&P continued to tank. (I’ll give you a peak into the future — as of mid-April, ACCRE is almost back to break-even.)

Again, for the uninitiated, the chart normalizes everything to a dollar invested. Hence, a dollar invested in ACCRE at the inception, 3 years ago, is worth $1.62 today, for an annualized rate of return of about 17%, compounded. That same dollar invested in the S&P 500 would be worth $1.18 today (about 5.7% annually), and if invested in the S&P Global Property Index would be worth only $0.93.

By the way, there is a second, private “newsletter” that goes out to subscribers announcing any trades I make as well as the percentage makeup of stocks in the portfolio. If you are interested in that, please let me know.

Share this:

No two recessions are alike… but…

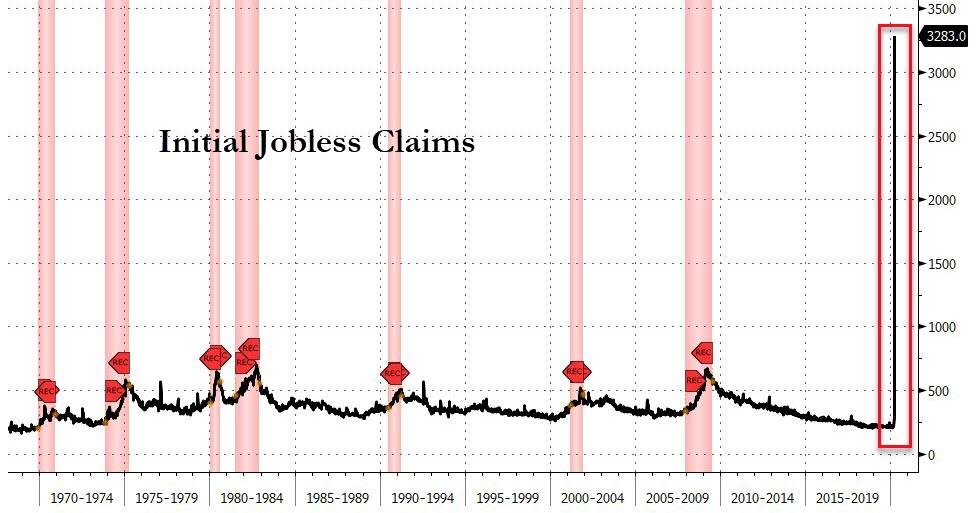

OK, folks, we are most decidedly in a recession. The initial jobless claims are like nothing we’ve ever seen before:

Goldman Sachs is predicting a total GDP pull-back of 24% in the third quarter, which is unprecedented. They further expect this to really tank in April, but the red ink should slowly abate after that. Net for 2020 will be a negative 3.8% GDP. The service industry will be hit the hardest, but there will also be a housing / construction slow-down, and of course manufacturing will be hit as well. Since Europe and the US buy lots of stuff, expect the rest of the world to follow suit.

With this, you would expect the markets and real estate to tank, but just the opposite seems to be happening. The broader indices, and my ACCRE real estate fund, are off their previous lows and trending nicely upward. It would appear that markets discounted the worst, and are now favorably impressed with the Federal government’s ability to step up to the plate with both fiscal and monetary stimuli. (Note that most other countries do not have this luxury — China has to sell U.S. bonds, of which they have about $1 Trillion, but can’t really issued bonds of their own to stimulate their economy.)

If Goldman Sachs is right, this will be nasty-bad for a few months, and then should abate by the end of the year. The 1958 recession is worth studying — particularly as it impacted U.S. social programs, the economy, and the shift in the power structure.