Archive for July 2023

Travel Stats and Real Estate

It’s widely recognized that, in major American cities, the central business district (CBD) office market suffered greatly during and as a direct result of the pandemic. There have been spin-off impacts for CBD retail, as down-town workers are no longer there to shop on their lunch breaks or to dine in street-front cafes and restaurants. Worker-bees quickly adapted to work-from-home, with tools like Zoom and Teams and others proliferating, and a parallel expansion of broad-band facilitating all of that. Now that the pandemic has receded, few seem anxious to return to the commute-and-work grind.

Arguments abound over the efficiency and efficacy of “work from home” versus “work in a cube farm”. Most managers seem to agree that there may be room for a balance — say 3 days per week in the office? Two? It depends a lot on the nature of the work, but still there is widespread agreement that we have too much CBD “B” grade office space right now, and perhaps too much ancillary space (e.g. — street front cafes) as well.

It’s hard to get a handle on exact statistics about office utilization. Many big cube-farms are tied up in long-term leases, and while some building owners and managers use technological tools like elevator trips and key-car swipes, they are also loathe to disclose actual data. This isn’t a trivial problem, since most of these affected buildings are financed and/or have institutional ownership. Real estate finance, development, and long-term utilization trends are all in the balance.

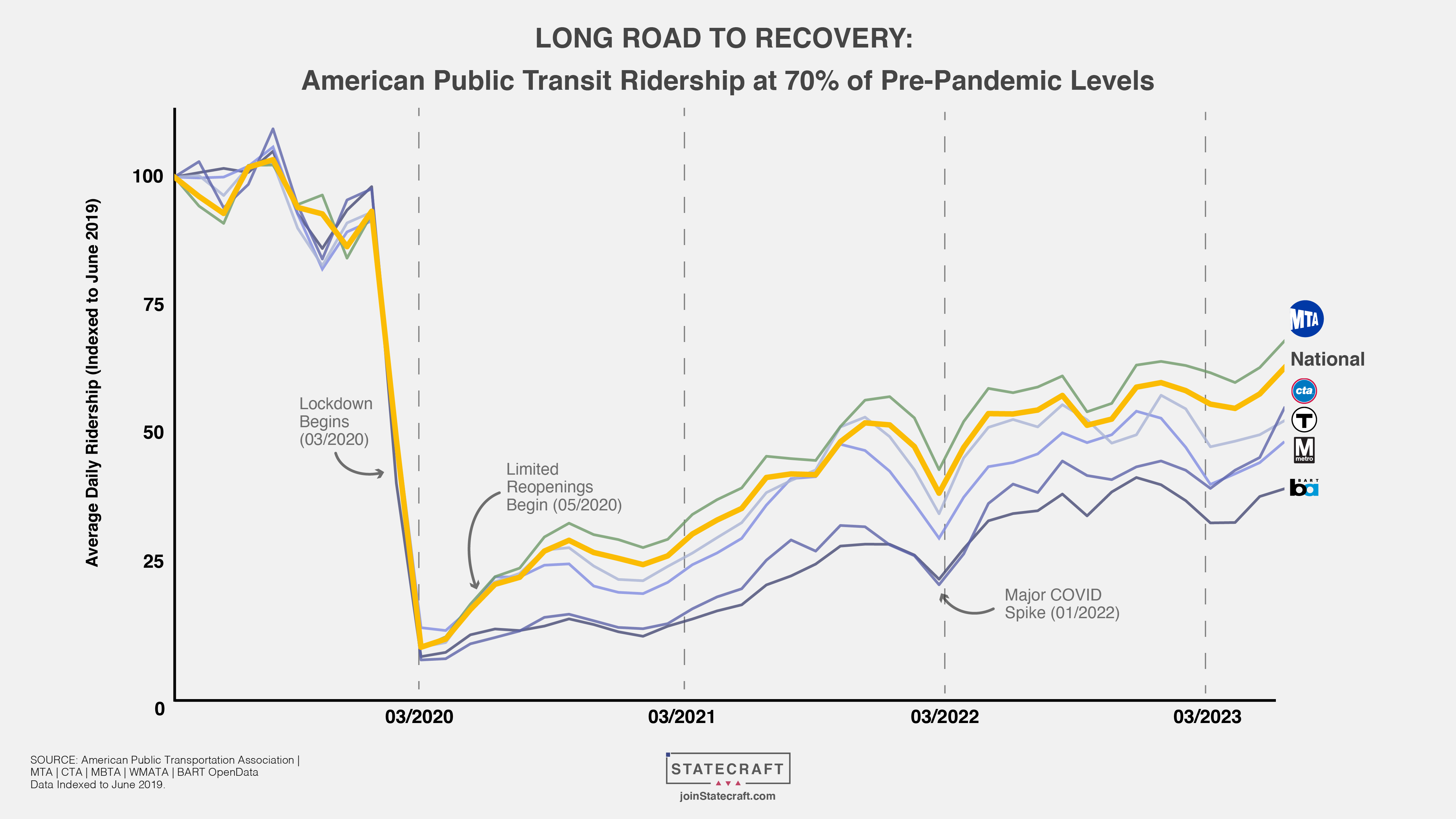

One bit of data that just came across my desk was a graphic I found from Statecraft.com (a California-based political software company), which tracks the utilization of mass transit across many of the nation’s top transit authorities as well as the national average. For comparison purposes, ridership is normalized to 100 as of the onset of the pandemic. The results are revealing.

Nationally, we’re at about 70% of pre-pandemic ridership NYC’s MTA leads the list with slightly under 75%, while San Francisco’s BART is turning in an anemic ridership less than 50% of former levels.

Naturally, this has enormous implications across numerous economic and public policy sectors. In my own home base of King County, Washington, for example, we’ve made enormous investments in public transit for riders who may not be back for a long time to come. However, from a purely real estate perspective, these riders used to occupy offices, stores, and shops in the downtowns of our major cities. thirty to fifty percent of them aren’t there now, and that means the space they used to occupy has only marginal productive value.

As usual, I enjoy hearing from you. If you have any questions or comments, please let me know.

John A. Kilpatrick, Ph.D., MAI