Archive for April 2021

Home Price Paradox

If there’s a recession, why are home prices still going up? That was the focus of an article last week by Anna Bahney form CNN Business titled “Home Prices Hit a New Record Because There Simply Aren’t Enough Houses for the Crush of Buyers.”

Two things she does not mention. First, this recession is nothing like the last one. Indeed, the last recession was deepened in no small part because because of the surplus of foreclosed homes. (Yes, there were a LOT of other reasons, and we can go into that later.) Second, our studies at Greenfield indicate that since WW-II, home prices generally do not fall during recessions (the last one being the exception). However, this recession is odd in that it is not being felt evenly throughout the economy. The bottom tier of workers — who are most likely to be renters — are suffering disproportionally. At the middle of the economy and above — the folks who are likely to be homebuyers — the recession hasn’t hurt quite as badly. Coupled with that, there is a very real material and labor cost problem.

Not surprisingly, according to Ms. Bahney’s article, the median price of a home in March in the U.S. hit $329,100, up 17.2% from a year ago. The inventory of homes for sale is down 28.2% from a year ago. Worse still, the inventory of homes for sale between $100,000 and $250,000 is down 36.6%.

According to Lawrence Yun, chief economist for the National Association of Realtors, this is resulting in a widening gap between haves and have nots. “You will have homeowners gaining wealth and renters missing out,” he said. He used San Francisco a few years ago as an example. If one middle income household purchase a home a few years ago, and the other did not, the first household are now millionaires. Yun calls this rapid price appreciation an “arbitrary outcome” for family wealth.

Anecdotal evidence suggest something of a flight from urban areas to the suburbs, somewhat as a reaction to COVID and a need for space to work from home and home-school. Since owner-occupied residences are more likely in the suburbs, this suggests an increasing demand, and no real end to the price crunch in sight.

Share this:

New York Office Space

Let’s start out by admitting that New York City real estate is unique. In very many ways, what happens in NYC has no bearing on “Anytown America”. However, COVID has put pause to many economic rules-of-thumb, this one included.

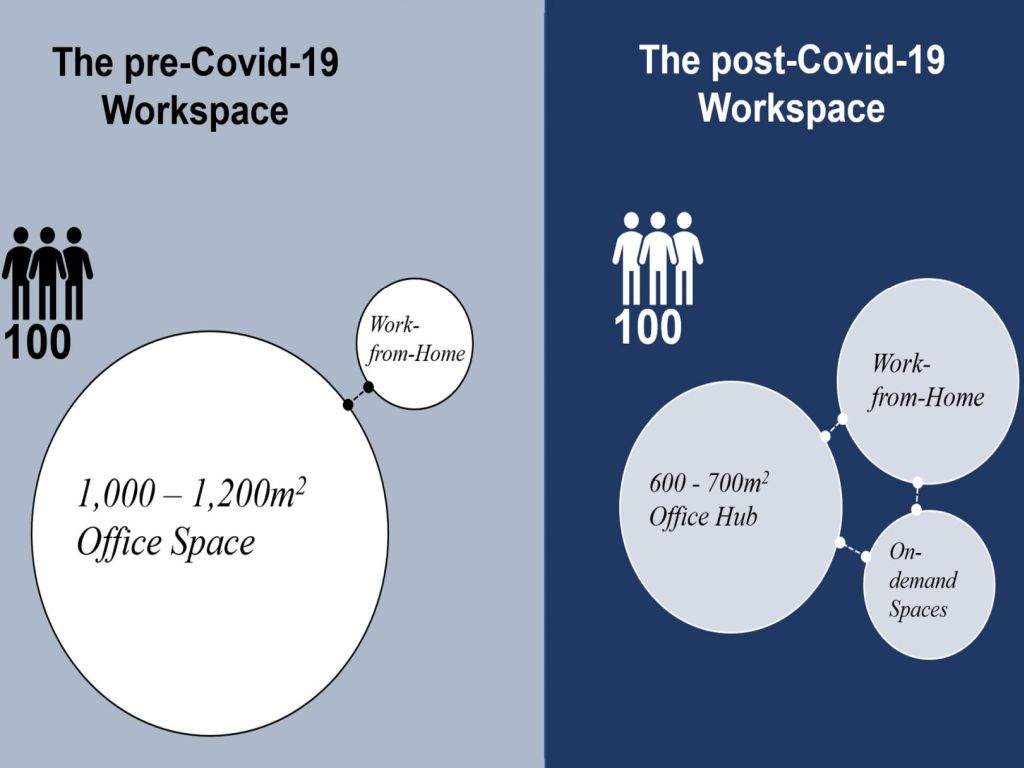

I was struck by a CNN.com Business article this morning by Allison Kosik titled “New York City Hasn’t Had This Much Empty Office Space in Three Decades.” According to a Cushman Wakefield report, cited in the article, office space vacancies in Manhattan alone reached 16.3% in the first quarter of this year, up from 11.3% last year. By some estimates, there is about 240 million square feet of office space on that island, so about 12 million square feet went vacant in 2020, directly attributable to the COVID-19 recession.

Now, as Ms. Kosik pointed out, this represents people who are no longer working in an office, but working from home. In my experience (and I “zoom” with folks in NYC a lot) these folks are still busy, but happily telecommuting. What’s more, these aren’t temporary shifts — these shifts are permanent enough to cause their employers to give up the space.

Is this a trend? Will other employers continue to facilitate work-from-home? I would note that even 10 years ago, technology would probably not have supported this on a wide-scale. “Zoom” (and all of the other services, like Team and Webex), ubiquitous high-speed connectivity, smart-phones, and secure cloud servers are all necessary for this to work. However, 100 years ago, the office of today could not have been supported without technology like computers, telephones, and even air conditioning. Has COVID really triggered a sustained shift in the American workplace landscape?

I would have to note that the thousands and thousands of office workers who now work from home previously supported a vast secondary and tertiary network of businesses. Working from home means you don’t grab lunch at the corner deli as often. You don’t buy “work clothes” as often — if at all. Parking garages, busses, and subways all see downturns in business. Demand for Yellow Cabs in New York City has collapsed, and I don’t doubt that is true nationwide.

Offices occupy about 18% of all commercial space in America, and use about 20% of the electricity. This is not a trivial footprint, nor one which shifts quickly. One model proposed by Regus, a provider of flexible workspaces, is a variant on the old “hotelling” model of a few years back. Businesses shrink the office footprint by enabling work-from-home, but then provide some necessary space for customer/client contact and some flex space options for shifting project demands. This is probably a great model for professional businesses (attorneys, CPAs, researchers) but may not be a one-size-fits-all for ever office occupant. Nonetheless, this may very well be an increasing solution, suggesting at least a “flat” demand for new office space for quite a few years to come.

We’ve actually made some of these shifts at Greenfield, with the attendant problems and benefits. As always, if you have any questions or comments about this, please feel free to reach out.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Share this:

ACCRE LLC Report, March, 2021

We’d LIKE for our fund to have positive returns every month, and to beat the benchmarks more often than not. March was certainly the exception to the rule.

We not only turned negative in the face of a strong, positive S&P, but also we underperformed global REITs. Part of the reason is that we’ve tried to stay defensive on the volatility front, and indeed we did that. However, that also means we may miss important market turns. I would note that this is the first month since we began keeping record that the S&P 500 cumulative SHARPE Index bested us, which is saying a lot for our defensiveness.

The first trades of April (not reflected above) are positive for us, but we’re going to have to go a long way to ameliorate the last two months of negative returns.

| S&P 500 | |

| Average Daily Excess Return | 0.0457% |

| Standard Deviation | 1.3073% |

| Sharpe’s Ratio | 3.4967% |

| ACCRE Fund | |

| Average Daily Excess Return | 0.0343% |

| Standard Deviation | 1.2058% |

| Sharpe’s Ratio | 2.8466% |

| Correlation (history of the fund) | 52.2405% |

| Correlation (monthly) | 69.4484% |

Undoubtedly, we’ll consider our positions in the next few days, and if any changes are warranted, our subscribers will receive trade alerts accordingly.

Best wishes for a great April, and as always, if I can answer any questions on this or related topics, please don’t hesitate to reach out.

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com