Archive for February 2021

Philadelphia FED Survey

One of my frequent economic touchstones is the quarterly survey of economic forecasters conducted by the Philadelphia FED. Obviously, they can’t pick “black swan” events (e.g. — COVID) but once the economy is in a steady state, they are usually very good at seeing intermediate term trends.

The improvement in sentiment from before the election is palpable. Their panel of forecasters project real GDP growth this quarter (that’s nominal growth minus inflation) at 3.2% annualized, with an overall growth at 4.7% in 2021 and 3.7% in 2022. These represent significant improvements over previous forecasts.

Unemployment will continue to nag us, but is on a downward trend. According to their forecasters, we should end this quarter with unemployment at 6.3%, trending down to 5.1% in early 2022. Non-farm job growth is projected at 223,400 per month this year. Inflation is expected to nudge up a bit, although that’s not entirely a bad thing coming out of a recession, as it indicates increased demand. The previous survey anticipated inflation at an annualized rate of 2.0% in early 2021, but now forecasters expect that at 2.5%. That said, the general projections for inflation for the coming decade, barring any flocks of black swans, is in the range of 2.2%. With that, 10-year treasuries are forecasted to average 2.8% over the coming decade, up from an early forecast of 2.7%.

Most interestingly, forecasters were also asked about the probability of another negative-GDP quarter this year (signaling a return to recession). Before the election, the average sentiment was a 20.4% chance of a quarterly GDP contraction this year. After the recession, this has nudged down to 19.1%. While that may not look like much of a change, it is a meaningful shift in forecasters’ sentiments. Survey respondents were also asked about economic output and productivity for the coming decade. A year ago, they projected the ten-year average annual productivity growth at 1.4%, while now they’ve raised the bar to 1.75%, a significant increase in their forecast of U.S. output and productivity.

Finally — and this is probably of most interest to our readers — the forecasters were asked about house prices this year and next. They looked at six different house price indices (see below), and forecasters projected median house price increases ranging from 4.7% to 7.9% this year, slowing somewhat to 3.5% to 5.3% next year.

| 2021 Median | 2022 Median | |

| S&P CoreLogic Case-Shiller: US National | 6.8% | 4.5% |

| S&P CoreLogic Case-Shiller: Composite 10 metros | 4.7% | 3.9% |

| S&P CoreLogic Case-Shiller: Composite 20 metros | 7.5% | 5.0% |

| FHFA: Purchase Only (US Total) | 5.6% | 3.5% |

| CoreLoic: National HPI including distressed | 5.6% | 5.3% |

| NAR Median: Total Existing | 7.9% | 5.1% |

As usual, if we can answer any questions about this, or if you have any comments, please don’t hesitate to reach out!

John A. Kilpatrick, Ph.D., MAI — john@greenfieldadvisors.com

Share this:

A New Twist on Rails to Trails Takings

In 2019, the Appraisal Institute, the Appraisal Institute of Canada, and the International Right of Way Association produced Corridor Valuation, an anthology on a complex subject which is surprisingly common in (pipelines, rail lines, power lines, etc.). I had the very real privilege of contributing two chapters, one on telecommunications corridors (fiber optic cable, etc.) and co-authoring the chapter on Rails to Trails corridors with my esteemed colleague, David Matthews.

Each year in America, on average, about 2200 miles of rail lines are abandoned, and often converted to public use, such as hiking/biking trails. However, the legal nuances are a bit more complex than meets the eye. Often, the railroads did not acquire “fee simple title” to the corridor, but rather acquired a perpetual easement with the proviso that if the rail corridor was ever abandoned, the land reverted to the adjacent property owner. “Abandoned” was usually a process over many years, and as these rail lines became effectively abandoned (although perhaps not legally so), the adjacent property owners made use of the land for residential developments. golf courses, and a host of other uses.

Without re-typing our entire book chapter, sufficient to say someone happened upon the idea that converting these “abandoned” rail lines to public use (e.g. — hiking/biking trails) was a good idea. However, there are costs involved. In a case that made its way to the US Supreme Court not too many years ago, it was decided that these adjacent property owners should be compensated not only for the loss of the land (that otherwise would revert to them) but also for “severance damages” which would be the loss of value to their adjacent property for now having a public use in their back yards.

So… I gave you all of that as a prologue to this. There is a really interesting rails-to-trails case coming out of Oregon right now. Many of the adjacent property owners around the US have argued about the loss of security from having hikers/bikers in their back yards. The project in Yamhill County, Oregon (southwest of Portland) spanned farmland. The argument posed by the farmers was that the new Yamhelas-Westsider recreational trail would inhibit the use of pesticides and endanger food safety (along with the common argument that the trail would invite trespassers). Oregon law requires a 100-150 foot exclusion zone depending on the pesticide being sprayed. If a bicyclist or pedestrian passes within that area, apparently the farmer is supposed to stop spraying.

This is a terrifically interesting argument, and I would have been very interested to see this litigated. However, the county’s board of commissioners voted last week to withdraw the land use application, even after spending in excess of $1 million on the project (and probably obligating to pay the state back another $1 million). The phrase “cut our losses” came out of the final commission meeting to end the project. Notably, Oregon’s Land Use Appeals board had blocked the project at least three times, finding that the county did not sufficiently study the impact on farming.

I doubt we’ve seen the end of this. A lot of money has been spent on both sides, and the proponents of the trail have are well organized. This will be a very interesting case if and as it moves forward.

Share this:

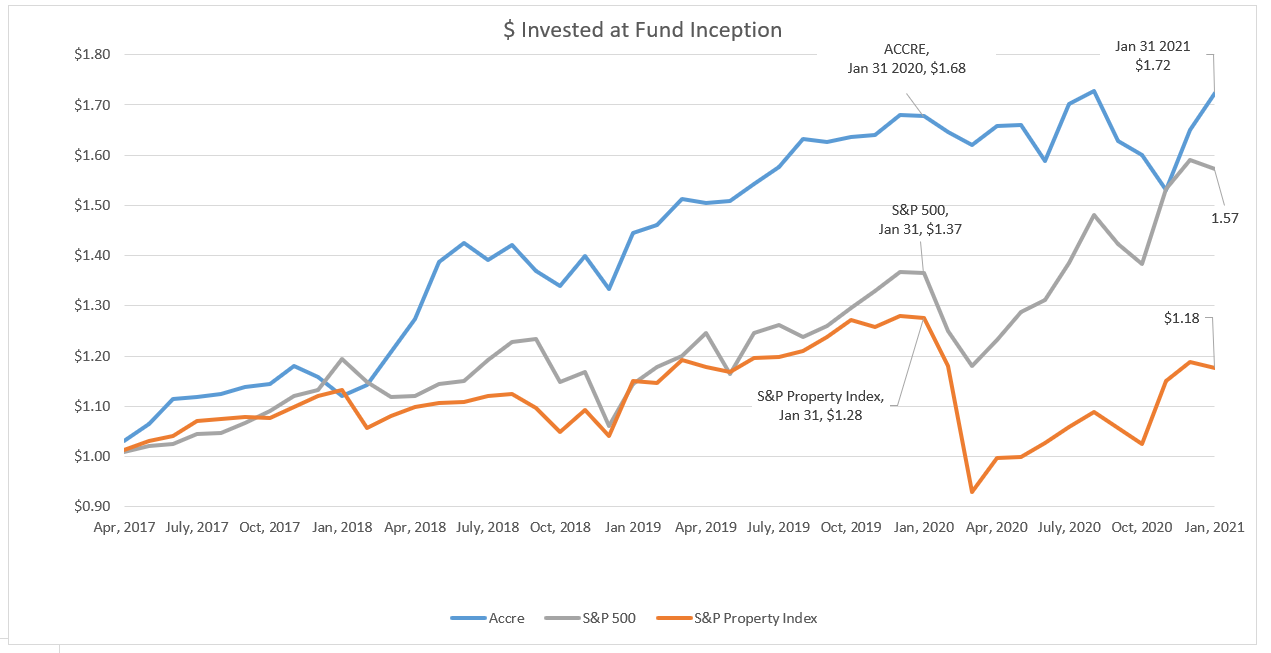

ACCRE LLC Report, January, 2021

Well, wasn’t THAT an interesting month! In times of market turmoil, investors often turn to real estate as a safe haven, and we certainly saw that happen in January. The overall S&P was down a bit but the volatility continues to be noteworthy. As such, ACCRE did quite well compared to both the overall market (S&P 500) and the global real estate in general (S&P Global Property Index). We’ve had two very nice months in ACCRE, and hope to see that trend continue in the new year.

Unquestionably, the S&P had a better 2020, but is off to a comparatively lackluster start in 2021. We hope for the best, of course, but it’s important to note that one reason for ACCRE is to provide diversification in an otherwise healthy portfolio. It continues to do that, and continues to provide above-average risk adjusted returns. The overall correlation between ACCRE and the S&P is a bit higher than last month, but continues to be much lower than the historical average.

| S&P 500 | |

| Average Daily Excess Return | 0.0405% |

| Standard Deviation | 1.3203% |

| Sharpes Ratio | 3.0710% |

| ACCRE Fund | |

| Average Daily Excess Return | 0.0485% |

| Standard Deviation | 1.1922% |

| Sharpes Ratio | 4.0651% |

| Overall Correlation (life of fund) | 51.9201% |

| Correlation (monthly) | 21.4110% |

Again, for the uninitiated, the Average Daily Excess Return is the daily return minus the return that would have been earned in a risk-free asset (here, the coupon-equivalent 13-week T-Bill, measured daily). The Sharpes Ratio is the ratio of those excess daily returns to the standard deviation of those returns (the measure of volatility) and serves as a proxy for risk-adjusted returns. ACCRE usually has higher excess returns and almost always has lower volatility, hence a higher risk-adjusted returns.

Best wishes to you all, and if I can answer any of your questions on REITs or real estate strategies, please drop me a line.