Archive for March 2020

No two recessions are alike… but…

OK, folks, we are most decidedly in a recession. The initial jobless claims are like nothing we’ve ever seen before:

Goldman Sachs is predicting a total GDP pull-back of 24% in the third quarter, which is unprecedented. They further expect this to really tank in April, but the red ink should slowly abate after that. Net for 2020 will be a negative 3.8% GDP. The service industry will be hit the hardest, but there will also be a housing / construction slow-down, and of course manufacturing will be hit as well. Since Europe and the US buy lots of stuff, expect the rest of the world to follow suit.

With this, you would expect the markets and real estate to tank, but just the opposite seems to be happening. The broader indices, and my ACCRE real estate fund, are off their previous lows and trending nicely upward. It would appear that markets discounted the worst, and are now favorably impressed with the Federal government’s ability to step up to the plate with both fiscal and monetary stimuli. (Note that most other countries do not have this luxury — China has to sell U.S. bonds, of which they have about $1 Trillion, but can’t really issued bonds of their own to stimulate their economy.)

If Goldman Sachs is right, this will be nasty-bad for a few months, and then should abate by the end of the year. The 1958 recession is worth studying — particularly as it impacted U.S. social programs, the economy, and the shift in the power structure.

Share this:

Real Estate and the Pandemic, part 2

Week before last, I wrote about the performance of our REIT portfolio versus the S&P during this market crash. I wanted to bring you up to date on that today, and I’ll continue to update you in the future.

First, as a reminder, I own and manage ACCRE, a private REIT fund made up entirely of real estate shares. Over the past three years, we’ve out-performed the S&P about 2.5 times. Further, because we’re only partially correlated with the S&P (about 45%), we get a high degree of diversification in volatile markets. Real estate is generally considered to be a “safe harbor” in troubled times. This is no exception.

I’ve tracked the S&P since the peak on February 19, and normalized both the S&P and ACCRE so they’ll fit on the same graph:

As you can see, from the peak, the S&P was down about 29.18% at the close yesterday. (It is up 0.70% on the day as I write this). ACCRE has tracked the S&P in parallel, but with a significantly lower down-trend. Hence, we’re only down 13.47% since February 19.

Naturally, hindsight is 20-20, and the perfect spot would have been in cash on February 18. That said, I’ve weathered more than a few bear markets in my several decades (see my post on March 11), and we seem to have come through all of them nicely.

Share this:

Welcome to the bear market, folks

Please watch your step. This will be a lot messier than you’ve seen for the past decade or so. You’ll want to wear rugged clothes and comfortable work boots. I’d wear a hard hat and goggles, too.

So apparently we’re in one. The term can be confusing — an individual stock can be in a bear market, but right now, we’re talking about the whole shooting match — NASDAQ, Dow Jones, and S&P-500. We call it a “bear market” when it drops 20% from its 52-week high. Many of you have never seen one. I’ve seen more than a few.

The average recorded bear market lasts 367 days, but some pundits unofficially say more like 18 months or so. That’s from the beginning of the bear until the market returns to 20% above the eventual bear trough. Between 1900 and 2008, we’ve had 32 recorded bear markets. We were clearly overdue for one. Bear markets are usually accompanied by recessions. Hence, the hoarding of toilet paper. There are generally two kinds of bear markets — cyclical and secular. Secular bears last much longer. Indeed, one could argue that the entirety of the 1970’s was one long secular bear market. Cyclical bears tend to be deeper but shorter. Hopefully, that’s what we’re in right now.

Prices can cycle up and down during a bear, but until we get 20% above a bottom, we’re still considered to be in a bear trough. Here’s the good news — historically, once the market finds a bottom (and that may take time), the bull run can last quite a bit of time. Consider the most recent cyclical bear, that happened in 2008. The Dow closed at 6,544.44 on March 6, 2009, down 53.4% from its peak. Of course, since that bottom, the Dow has risen almost 500%.

The most severe, sharp bears seem to be related to a world event. In the prior example, which was the second worst on record, it was the real estate securities melt-down. The third worst on record was the 1973 bear, which is generally attributed to President Nixon’s mishandling of the gold standard. Of course, the worst bear in history was the 1929 crash, when the Dow fell 94%. More typical bears are those which simply follow a long bull run. For example, the 2000 bear began on January 14, 2000, and the Dow eventually fell 37.8%. (Notably, that bear INCLUDED the 9/11 terrorist attacks, but was not precipitated by it). The 1970 bear began at the end of 1968, and the Dow eventually fell 30%.

Just like everyone else, I’m watching my portfolio with more than a little trepidation. However, my own investments were pretty well thought out during the bull run, and should serve me well as insulation from any bears.

I’ll keep you posted.

Share this:

Health care, and health care finance

OK, I’ll admit right up front that my areas of expertise do not span health care. I’m an economist, with a focus on micro-analysis and real estate. That said, the Venn diagram of the Democratic primary and the pandemic crisis is giving voice to the “Medicare for all” crowd — perhaps a much larger voice than they otherwise deserve.

With that, I’ll talk about car buying for a minute. Lots of people buy cars — I own several. At the top of the economic food chain, buyers just write a check. Some have pre-arranged financing thru their bank. Others get a loan at the dealership itself. There is even a “buy here pay here” option in many places for car buyers with truly awful credit. (The imputed interest on those loans is usurious, but that’s for another day.). If you absolutely CANNOT afford a car, or don’t really want one or you’re too old to drive, there is mass transit, which may be subsidized by the local taxpayers, will usually cost a trifle to ride, and may be underwritten by employers for their staff (we do that at Greenfield as an employee benefit).

How about acquiring a place to live? For about 60% of American households, that means an owner-occupied residence (mostly single family, but some co-ops and condos). Mostly those are financed with mortgages. The rest of us live in apartments or rental houses, and those residents are usually utterly clueless about how the building is financed. Admittedly, there is a bottom rung of the ladder, and we struggle at the local level to provide shelter for all. However, there is little evidence that public sector intervention solves that problem successfully without private sector partnership.

The point being, complex assets and services are generally provided in a manner agnostic to the financing of those assets and services. I’ve heard all of the stories of how Canada and other countries have somewhat successfully implemented single-payer systems, but I’m still skeptical that a heterogenous nation like the U.S. could do that successfully.

That said, this pandemic has illustrated the problems of health care delivery versus health care finance. The Feds are already stepping in with billions of dollars to ensure (not “insure”) appropriate epidemic control and emergency health care delivery to all who need it. We can — and economically SHOULD — find a way to ensure that every American has access to health care. However, the financing of said system can — and economically SHOULD — remain multi-tiered. Health care DELIVERY and health care FINANCE are two different and separately complex issues.

If you are a union member, or an employee of a company with health care benefits, and happy with your system, you should be able to keep it. If you can afford private health insurance, and prefer to go that route, so be it. However, “Medicare for all” sounds a lot like “mass transit for all”. I’m more than happy to see a portion of my tax dollars go to support a system whereby everyone has a ride to work, but I and my jeep will continue to enjoy the other lanes of the highway.

Share this:

Real Estate and the Pandemic

I’ve been asked several times in the past few days to comment on the economy, the market, and particularly real estate during this current crisis. By the way, as a general rule, real estate is a safe harbor during times of crisis, but that doesn’t give a very good answer to an immediate question. Let’s look at it another way.

First, it appears that the stock market really started realizing that this was a problem in late February. Indeed, the S&P 500 hit a peak of 3,386 on February 19. That was an increase of almost 4% in less than two months. Then the reality hit that this thing could have very real impacts on supply chains, spending and consumption behavior, corporate profits, and thus the economy as a whole. As of the close yesterday, the S&P was down an astonishing 12.2% in only 12 trading days.

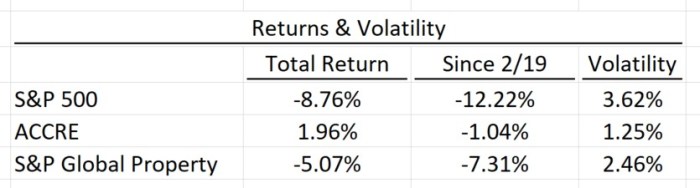

That’s a fairly short timeframe in which to measure real estate returns. However, I have a couple of good proxies for that. As you know, I manage a small, private REIT hedge fund called ACCRE. This is a carefully curated fund, and has out-performed the S&P by about 2.5X since I started it in 2017. (For more about ACCRE, please visit the web site, www.accre.com.) I also track the S&P Global Property Index, which is a daily traded index of securitized real estate. While neither of these is a perfect measure of how all real estate is doing in this crisis, these do give some measures of how well real estate can attenuate the volatility in a portfolio, and whether or not well-chosen real estate investments can really be safe harbors.

To make a comparison, I “normalized” all three indices to = 100 on January 2, 2020. That way, all three indices will fit on the same graph:

The Global Property Index, unfortunately, tracks the S&P 500 fairly well, although with a bit less volatility. It is a weighted index, but not a managed one. Hence, a broad random investment in real estate may have performed better the past few weeks, but not by much. ACCRE, on the other hand, is a carefully managed portfolio, and has actually performed quite well this year.

Volatility is simply the standard deviation of the indices since January 2. As you can see, the S&P has not faired well, but the Global Property Index has done a bit better, albeit with much lower volatility. The managed (I would use the word “curated”) real estate portfolio is actually still up on the year, and with the lowest volatility of the three.

I’m asked almost every day, “when is it a good time to buy real estate?” A surprising number of investors expect a recession, and want to wait until the depths of the recession to move money from stocks in to real estate. Clearly that’s counter productive. The time to buy carefully selected real estate was three weeks ago. However, it may not be too late.